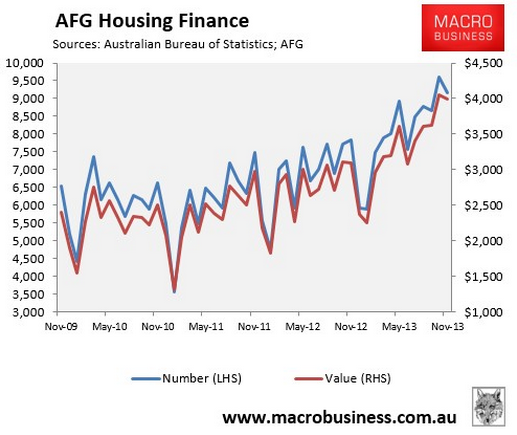

Australian Finance Group (AFG) has released its housing finance data for the month of November, which registered a 4.5% fall in mortgage applications over the month, but more importantly (since the series isn’t seasonally-adjusted) a 17% increase the number of applications over the year:

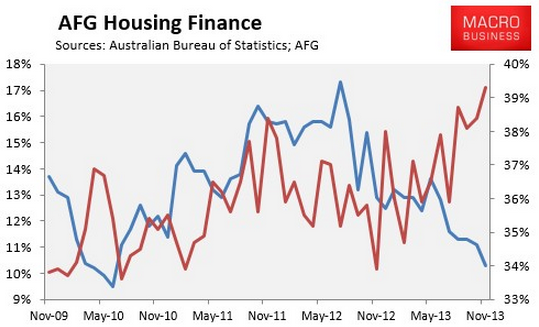

Investors are now screaming ahead, with their share of mortgages rising to 39.3% in August, according to AFG (see next chart).

Much of this investor demand is being driven by New South Wales, where investors accounted for nearly half of all mortgages in November. FHBs fell to an astonishing 2.8% share of new mortgages. Think about it. Only three in every hundred mortgages in NSW are now first home buyers. This is either a data problem or it is a howling bubble in action.

Other states are also bad and getting worse:

Participation by first home buyers varies dramatically by state, with AFG recording its worst ever figure for NSW, where only 2.8% of new mortgages were for first home buyers – compared with 48.5% for investors. Elsewhere, first home buyers comprised 6.2% in QLD, 11.4% in VIC, 16% in SA and 20.2% in WA. While WA has led the nation for first home buying activity over the past year, this 20% figure is still much lower than the 24.4% figure recorded six months ago in May 2013.

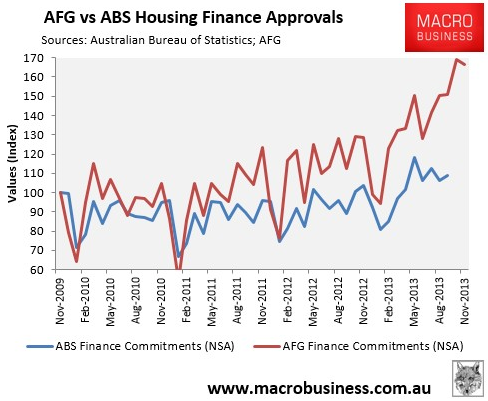

As noted previously, some caution should be exercised in interpreting AFG’s figures and extrapolating its results to the overall mortgage market, as measured by the Australian Bureau of Statistics (ABS).

AFG’s data measures mortgage applications, whereas the ABS measures actual mortgage commitments. According to AFG’s General Manager of Sales & Operations, Mark Hewitt, just over three quarters of applications on average become mortgage commitments, although this figure can obviously fluctuate month-to-month. AFG’s market share has also been rising in recent years.

Therefore, while AFG is a useful guide as to the strength of mortgage demand, its results do not necessarily translate to the overall mortgage market as captured later by the ABS.

To illustrate, consider the below chart showing how the growth of AFG mortgage applications has diverged significantly from ABS mortgage commitments since November 2009:

Nonetheless, the AFG data is painting a picture of a deeply unhealthy housing market with clear bubble tendencies as speculators party and fundamental demand collapses. Of course AFG spins that around as an appeal for another bailout:

Mark Hewitt, General Manager of Sales and Operations says: ‘Overall, the mortgage market is in robust, good health, and it’s encouraging to see more people willing to upgrade their homes and buy investment properties. But urgent action is needed to address the absence of first home buyers from markets in NSW and QLD. We need to see a lot more people get on the property ladder to underpin the long term sustainability of those markets.’