It’s barely an exaggeration to say that in the years since the global financial crisis, Australia’s liquefied natural gas boom has saved the nation. As other developed economies have seen their business investment chase collapsing consumer wealth and demand down the drainpipe, Australia has enjoyed a once-in-a-century investment boom.

This, above all other factors, has so far helped Australia avoid the kind of growth-devouring deleveraging that has hobbled other developed markets.

But despite its timeliness, the boom has been so enormous – with seven concurrent LNG projects – that it has caused huge cost inflation, rewriting the breakeven points for projects, and shoving Australian LNG to the wrong end of the global cost curve. There are definitely bubble elements to the chase for Australian LNG.

Unluckily for Australian producers, this has transpired even as the unconventional gas revolution in the US has done precisely the opposite, cutting the price of gas to historic lows. The abundance of gas in North America has swiftly turned into an LNG export boom encompassing Canada as well. And this gas can now be landed more cheaply in Asia than can Australia’s.

Thus Australia faces some very uncomfortable questions about the sustainability of its gas megaprojects the profitability of the companies that own them.

The gas story

The LNG story will be familiar to most readers. It is an offshoot of the same commodity supercycle narrative we all know very well. As Asia urbanises, it powers a lift in demand that leaves inelastic supply scrambling to catch up.

This has been exacerbated by pressure for climate change action – with gas being seen as an easy transitional fuel option – and, more recently, by Japan’s Fukushima nuclear disaster, which has temporarily shut down nuclear as an alternative fuel in one of Asia’s largest energy consuming economies. These three factors have driven global LNG demand up 39% to 250 million tonnes per annum (mtpa) since the GFC, and it’s forecast to almost double by 2025.

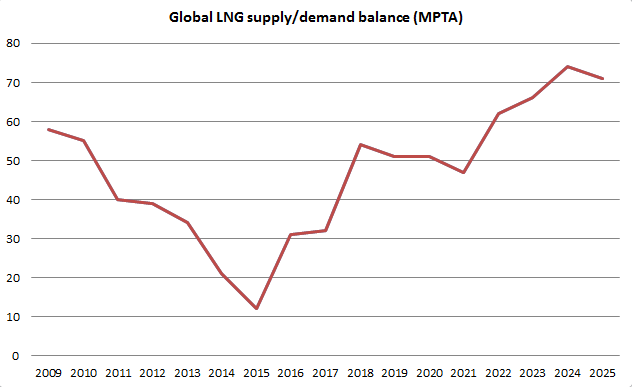

This has taken spot markets by surprise, especially since the Fukushima disaster, tipping the supply/demand balance in favour of suppliers, and it is expected to tilt further still for another two years (see Chart 1).

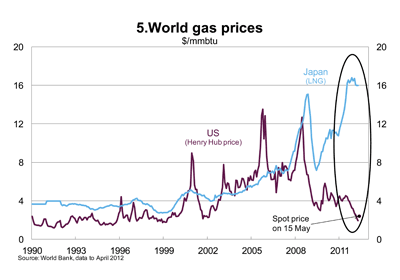

This, in turn, has driven prices sky high, as you can see from Chart 2.

Australia’s big seven projects will begin to turn this around from 2015, driving LNG supply back into surplus after several more years.

The magnificently expensive seven

The dynamics of a steepening gas supply curve have launched a staggering investment splurge in Australia. $180 billion has been hurled into seven monstrous LNG projects, the logistics of which are breathtaking.

In Western Australia, the Gorgon and Wheatstone projects account for $81 billion. In Darwin, Icthys is another $34 billion. In Queensland, three projects are in the process of transforming Curtis Island into a global energy hub, accounting for another $60 billion.

But the wisdom of undertaking these projects simultaneously is looking shaky. Indeed, they have launched LNG input costs into outer space. Gorgon’s current estimated cost has swelled to $52 billion, from $37 billion, but rumours are swirling that the ultimate cost will be $60 billion. Icthys is surrounded by similar uncertainty with rumours of a $10 billion blowout. And the risk of cost blowouts weight heavily on the owners of the Queensland three, including Origin Energy and Santos.

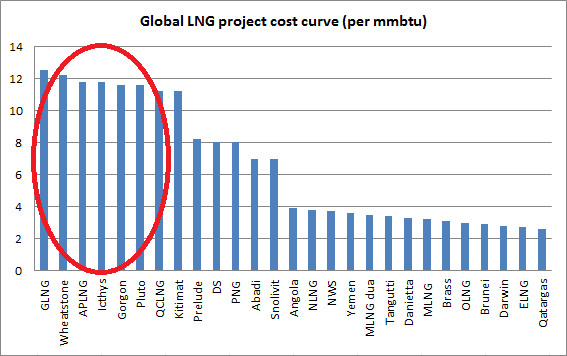

Australian now entirely occupies the wrong end of the cost curve, as you can see from Chart 3.

The $12 per million British thermal units (mmbtu) breakeven price might even be breached as costs continue to spiral. That may not have been a problem were it the end of the story.

The rise of competition

But there have been several unexpected chapters written into the tale. Unlike in some other commodities, such as iron ore, Australia does not have a natural monopoly in LNG. Gas is plentiful all over the earth but the US in particular has risen as an imminent and unexpected threat to Australia’s 95mpta in LNG projects.

Following its unconventional gas revolution, the US is enjoying gas prices around $3.60, roughly 20% of those paid in North Asia. Not surprisingly, there are very big plans to arbitrage this vast spread by exporting the surplus gas to Australia’s core markets in Japan and Korea. Already the US has approved four LNG projects (Sabine Pass, Lake Charles, Freeport project in Texas and Cove Point).

Another project, Cameron, has contracts in place and is expected to get approval in the near future.

These five projects represent 66mtpa of LNG.

Although US gas is cheap, the gasification and longer shipping times cost another $6 or so, meaning that it lands in Asia at around $10mmbtu. That in itself is going to pressure North Asian gas prices, but there’s more.

Another 28 projects (yes, 28) have lined up in North America for approval for a combined output of close to 300mpta! Canada has eight projects in planning and is very likely to get at least four of them going. The US has another 20 projects lined up but nothing like that many will get approval owing to several factors. For starters, the US would like to retain its cheap energy advantage for manufacturing, something Australia doesn’t want. Also, there is a lot of grass roots resistance to greenfield projects (existing approvals are for conversions of existing terminals). Nonetheless, if the US were to approve only the brownfield projects it would surpass Australian exports by 20mpta.

In that event, the International Energy Agency (IEA) projects that its local gas price will rise to $7 eventually, so more projects are a reasonable bet. The IEA also reckons that the widening of the Panama Canal plus increasing efficiencies in US gasification could push its production cost component down further, meaning higher volumes are possible without rising breakeven costs.

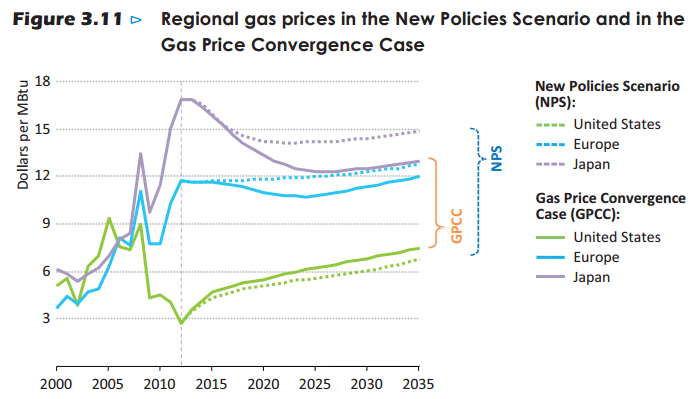

Thus, if the US pushes its export production towards 100mpta then the IEA sees the impact on North Asian prices shown in Chart 4. Follow the solid purple line. It falls right down to the $12 breakeven point for Australian projects sometime after 2020. That’s not necessarily a problem given Australian production is big enough that it can’t be taken out. But it does mean that whenever the supply demand balance slips towards buyers, it is Australian LNG that will be under pressure to limit output.

In short, Australia’s magnificently expensive seven represent the highest marginal cost production for LNG markets globally over the next two decades – and a constant threat to the profits of their owners.

Price protection

These market factors are best couched as risks rather than forecasts at this stage. But the likely outcome is still a falling North Asian LNG price over time. However, the magnificently expensive seven do have considerable price safeguards to ensure that production remains mostly strong.

The key defence is pre-sold gas. Most projects have 85% of their gas pre-committed to buyers (who are often equity partners) on long-term contracts that are linked to the oil price. Most are thought to have little room for renegotiation. It was these contacts that reassured debt markets enough to back so many projects at once. But you can expect growing contract risk, as iron ore miners have experienced when dealing with Chinese customers (which will be the source of new marginal demand).

Not all projects have pre-sold to these levels, either. Gorgon, for example, has only pre-sold 60%, and nobody is likely to sell any more gas on such contracts because customers have sensed the shift in competitive power and are campaigning for the abolition of the oil-link.

A final positive is that for those projects with high levels of pre-sold offtake, price pressures are five years away and the depth of price pressures ten years.

Conclusion

So what can we make of these top-down dynamics for the future of the Australian gas sector?

To start with, the near and medium terms look solid enough. And as projects successfully transition from construction to production, markets could de-risk share prices as they look forward to improving cash flows.

But there are reasons to think that share prices in gas firms and their support services could come under pressure.

First of all, there’s the risk of further capital expenditure blow-outs. This could push Australia’s magnificently expensive seven further out on the cost curve. As North American projects continue to gain momentum, there’s a danger that markets will discount the future income streams of Australian projects and their net present value.

Second, gas firms face a long and difficult process of reducing costs as their projects come on-stream and seek to remain price competitive as competition grows. Gas support services will face a lot of contract pricing pressure.

Finally, with these projects likely to impose a long period of project paralysis on disgruntled shareholders, as well as poor competitive metrics, future growth options are going to be limited.

————————————————————————————

Finally, here is the November traffic update for MB readers: