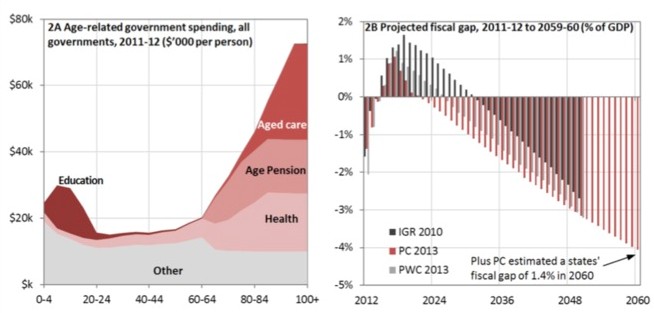

Yesterday, I questioned whether anyone in today’s crop of politicians would have the cojones stare down vested interests and clearly articulate the need for reform and ‘shared-sacrifice’ as the once-in-a-century mining boom fades and Australia’s population ages, which will place huge pressure on the Federal Budget (see below chart).

Today, the Labor Party’s shadow Assistant Treasurer, Andrew Leigh, seems to have ruled-out fundamental reform of Australia’s busted retirement system, arguing against lifting the pension age to 70, as advocated by the Productivity Commission. From The AFR:

Few social policies are as tightly targeted as the pension. The decisions to means-test it in the 1930s, and asset-test it in the 1980s, were vigorously contested. But they have ensured that this vital part of the social safety net goes where it is most needed.

Over the past week, there have been calls to increase the pension eligibility age from 67 to 70. Yet those advocating this change seem to have forgotten that low-income workers are more likely to do jobs – like childcare, construction and hairdressing – that involve tough manual labour.

It’s quite a different thing to expect an accountant to carry on their desk job until age 70 than to demand a bricklayer do the same… [N]ot everyone in a physical job will want to work until 70…

Given that Australians can access tax-free super payouts from age 60, is it really fair to make the poor wait until 70 to get the pension?

Leigh’s argument that it is unfair to expect those working in manual labour to work till they are 70 is bunkum. Anyone that is unfit to work – be they young or old – can access a disability pension, so it is not really an issue. However, suppressing the pension age would encourage many able-bodied workers to exit the workforce prematurely. It is poor policy and would place unnecessary strain on the Federal Budget.

His argument about the differential treatment between accessing superannuation and the pension is also questionable, as is his assertion that the assets test has ensured that “the social safety net goes where it is most needed”.

If he is so concerned about the lower access age for superannuation, then why not lobby to increase it so that it more closely resembles the pension? Further, how can he claim that the assets test is doing its job when the biggest asset most people own – the family home – is excluded from their capacity to fund their own retirement?

Indeed, the exclusion of the family home from the assets test for the aged pension, combined with the ability to withdraw one’s super as a lump-sum (instead of an annuity), has created an incentive for households to borrow to purchase an expensive home in the lead-up to retirement, retire at 60, withdraw their super tax-free as a lump sum, use the money to pay-off their mortgage or to fund consumption, and then go on the aged pension from 65 years of age.

In such instances, the taxpayer is left wearing the cost of superannuation concessions throughout the individual’s working life, and then again once that same individual goes on the aged pension. And while such a strategy makes sense for the individuals concerned, it compromises the integrity, fairness and sustainability of the retirement system which, after all, was supposed to relieve pressure on the Budget, not exacerbate it.

More broadly, Leigh’s arguments on why the pension age should not be raised focus a lot on fairness. But does Leigh honestly believe that it is fair to expect a shrinking band of younger workers, many of whom are already struggling under the weight of expensive housing and high mortgage debts (fostered onto them by their parents’ generation), to pay ever increasing amounts of taxes to subsidise the growing army of retirees – many of whom are in a relatively stronger financial position?

Something’s gotta give.