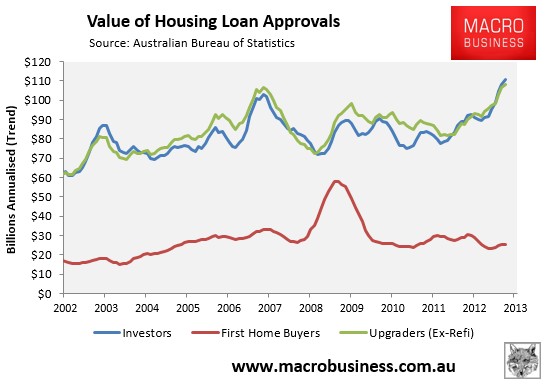

Today’s strong housing finance data, summarised earlier, reported a further weakening of first home buyer (FHB) demand, suggesting this housing cycle continues to be driven by investors and upgraders (see next chart).

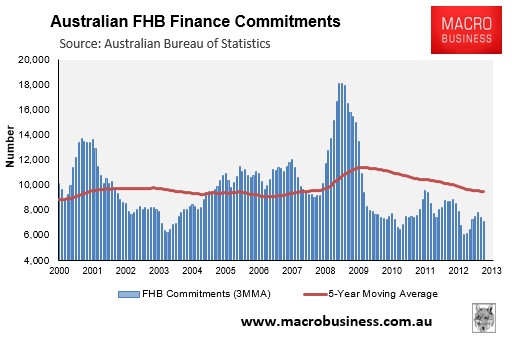

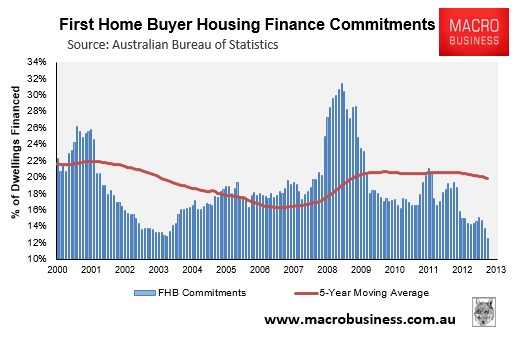

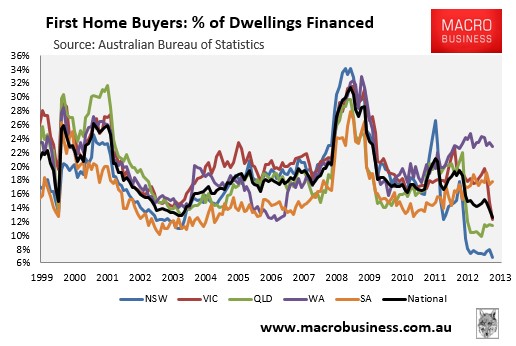

As noted in my earlier post, FHB commitments nationally slumped by 9% (non-seasonally adjusted) in September and were down 24% over the year. They also represented just 12.5% of total owner-occupied commitments – the lowest level in the series’ 22-year history (see below charts).

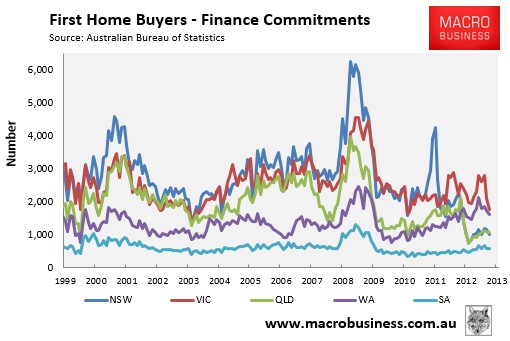

Looking at the state-by-state break-down, you can see that the FHB retreat has been driven by the eastern mainland states, where grants on pre-existing dwellings were cancelled in October 2012 in New South Wales and Queensland, and in July 2013 in Victoria (see below charts).

Whereas the FHB share fell to a record low of 12.5% nationally in September, well below the 5-year moving average (5yMA) of 19.8%, the shares in New South Wales and Victoria were just 6.8% and 12.2% respectively – both record lows and down from 5YMAs of 19.1% and 21.0%. Queensland’s FHB share also fell to 11.3%, down from a 5YMA of 18.2%.

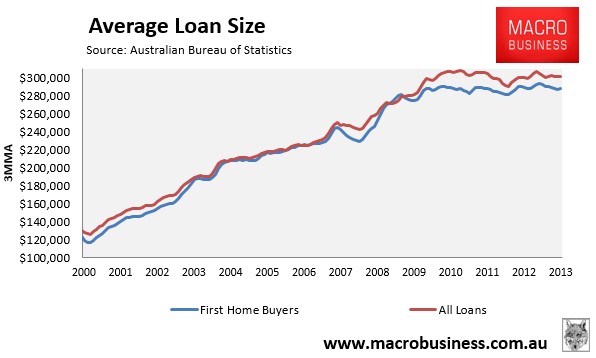

Another interesting observation is that the average loan size for FHBs has shown minimal growth over the past 4.5 years. Since March 2009, the average FHB mortgage has risen by only 2.6%, whereas the average mortgage for the market as a whole grew by 10.0% (see next chart).

While the slump in FHB demand is concerning, there is some ambiguity over whether a significant amount of commitments are being unreported. As noted last month, there have been anecdotal reports of lenders being unable to record FHB mortgages into their application systems. There could also be an increased reluctance of borrowers to record themselves as FHBs in the absence of any grant or stamp duty concession being made available.

Whether these factors are weighing heavily on the FHB data is impossible to know. Either way, like the woeful tracking of foreign buyers, the situation needs to be resolved since accurate data collection is vital in order for analysts, commentators, and policy makers to make informed judgements.