The reported slump in first home buyer (FHB) mortgage commitments has been well documented since the New South Wales and Queensland state governments cancelled the First Home Owners Grant (FHOG) on pre-existing dwellings in October 2012, which has subsequently been replicated by many other state governments (see below chart).

Over the past year, the reported number of FHB finance commitments has fallen by 22% nationally, with the proportion of total finance commitments going to FHBs also slumping to 13.7% in August – well below the long-run average of 20%.

However, reports have emerged that all is not what it seems and FHB mortgage demand may not actually be as weak as reported by the Australian Bureau of Statistics (ABS). Specifically, it could be the case that FHB mortgage commitments are being significantly under-reported due to:

- An inability of lenders to record FHB mortgages into their mortgage systems; and

- A possible reluctance of borrowers to record themselves as FHBs in the absence of any grant or stamp duty concession being made available.

The first factor above seems most persuasive. According to the latest Accredited Broker eNewsletter, some lenders’ systems do not have a box to tick for FHBs – only boxes exist for the FHOG and the FHB stamp duty concessions:

Once upon a time it was easy for the Bureau of Statistics to analyse how many first home owners there were because the First Home Owners Grant (FHOG) applied to all homes. Now that it only applies to new build, it may be that there are still many first home owners – but they are buying pre-loved properties and the government has no way of quantifying them.

The banks are no help either; they are supposed to record the number of first home owners. But, their software only records first home owners when they are simultaneously applying for the FHOG. So, if you are a first home owner with a established property – NOT RECORDED. Similarly, if you are a first home owner, but will apply for the FHOG after settlement – NOT RECORDED.

The property industry is having a great debate about the first home owners market, but we would be better informed if we could get the facts first.

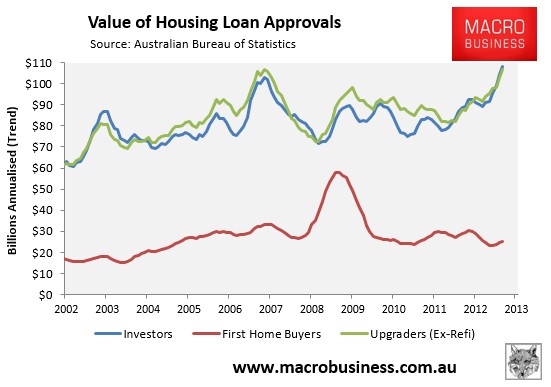

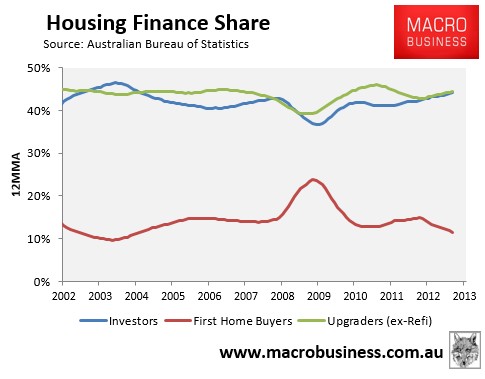

Looking at the overall housing finance data partly supports the above assertion. While, investor mortgage demand has rocketed, which has certainly helped to shut-out FHBers, upgrader demand has also risen significantly, suggesting that some FHBs might wrongly be getting captured as upgraders (see below charts).

However, it should also be noted that the FHOG had only been in force since the introduction of the GST in July 2000. Yet, the ABS seemed to accurately collect FHB mortgages prior to these grants, with the share of FHBs also much higher throughout the 1990s (circa 20%) than is the case currently (see first chart above). One wonders, then, how lenders and the ABS could accurately record FHB mortgages back in the 1990s (prior to the FHOG) and not now that the FHOG has been abolished on pre-existing dwellings across much of Australia?

Either way, like the woeful tracking of foreign buyers, the situation needs to be resolved since accurate data collection is vital in order for analysts, commentators, and policy makers to make informed judgements.