At the AFR Peter Reith reckons:

The public at large has not yet woken up to a looming gas price shock in the eastern states, the chairman of Victoria’s coal seam gas review says.

…the former federal minister chairing the Victorian review, told The Australian Financial Review he wanted a “fair deal” for farmers to encourage gas production and restrain price hikes. He also indicated his review was being heavily influenced by the potential impact of the gas squeeze on Victoria’s manufacturers, and the need to ensure access to gas at competitive prices.

“There is no doubt that we are seeing gas prices rise. This is a matter of great significance to manufacturing in Victoria,” Mr Reith said. “No one should kid themselves this isn’t a big issue. For the public at large, it hasn’t hit them yet, but I can promise them it’s coming.

“There are a lot of jobs and investments which will be impacted on by the rising price of gas.”

Mr Reith urged against delay in acting to lift a moratorium on coal seam gas development in Victoria. “Delays are only going to push out the transition period and that’ll have an impact on manufacturing in Victoria,” Mr Reith said in his first public remarks on the review.

For once, in reply, Ross Gittins and I see eye to eye:

The gas industry is working a scam on the people of NSW, in collusion with other business lobby groups and federal and state politicians. It’s trying to frighten us into agreeing to remove restrictions on the exploitation of coal seam gas deposits. Failing that, the various parties want to be able to lay the blame for an inevitable jump in the price of natural gas on the greenies and farmers.

According to the gas lobby, the manufacturing lobby, the Business Council, federal Industry Minister Ian Macfarlane and former Labor minerals and energy minister Martin Ferguson, we have a looming gas supply crisis in NSW and must unlock our local coal seam gas resources if we’re to avoid shortages and the price hikes they bring.

…The problem, we’re told, is NSW produces only about 2 per cent of the natural gas its households and industrial users consume. And when facilities for liquefying and exporting gas start operating within a year or two, producers in Queensland and Victoria will switch to exporting their gas to gain the higher foreign prices.

…Because of pipelines between the states, how much gas a state produces has nothing to do with the prices its households and businesses pay. According to the gas lobby’s logic, the coming ability of producers to get much higher prices by exporting their gas should produce shortages of gas for local users in Queensland and Victoria, not just NSW.In truth, there will be no shortages of gas in any state, just a requirement to pay the higher, netback price. There’s no reason producers would prefer to sell to foreigners if locals are offering to pay the equivalent price.

With the advent of fracking and access to higher prices, it’s not surprising gas producers are desperate to extract as much coal seam gas as possible as soon as possible. But their argument that increased production in NSW could hold down NSW gas prices is economic nonsense.

Any new gas producers in NSW won’t be willing to sell to locals for anything less than the equivalent price they could get by selling to foreigners. That’s the scam.

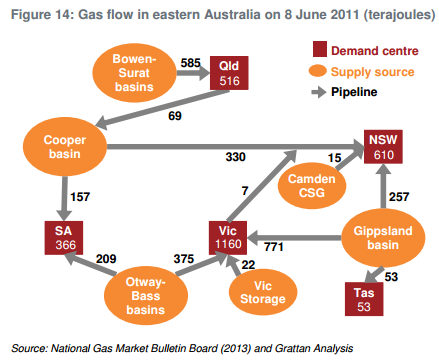

This is not entirely accurate. There is no current way to get NSW or Victorian gas to QLD. From the recent Grattan report:

Thus locally produced gas would be “captured” if it was accompanied by state reservation policies that prevented development of more LNG terminals or pipelines to Gladstone. But it’s still a scam. The problem is that CSG is not cheap. It costs around $6mmbtu to produce. Add a profit and you’re already at $7-8mmbtu.

The irony is that even though the Pacific Rim export market is causing the problem, it is also the solution. As North American gas drives down the price in North Asia to $12-$13 range from the current $15-16, the local netback price (that is minus gasification and shipping) will fall to the same $7-8 price range. In short, local prices are going to rise to export parity whatever you do.

It may be that more gas development is a good thing for jobs etc but let’s not kid ourselves about why, eh?