From the AFR:

Any hopes that the new consensus on the urgency of New South Wales’ natural gas problem would lead to softer rules for coal seam gas have been dashed. Much to the frustration of CSG companies, in particular AGL Energy, the NSW government has cemented the 2-kilometre buffer zone around residential areas. Indeed, the number of areas affected will increase as new growth housing regions are included. Hundreds of vineyards and horse stud properties will also be off limits to CSG. Arguments from AGL that the rule exempts hugely more land from CSG than warranted have been ignored.

Meanwhile, from the The Australian:

Australian Industry Group chief executive Innes Willox warned there was a “real risk” of industrial closures sparked by steeply rising gas prices within a couple of years as he criticised the NSW government for proceeding with “the most restrictive elements of its revamp of coal-seam gas regulation, regardless of the looming and intense gas-supply issues facing NSW”.

Let’s get a few points straight. Coal seam gas is causing the price spikes not fixing them. By opening the eastern seaboard gas market to North Asian prices via the Gladstone LNG hub, the local $4-5 mmbtu price can’t compete with $15mmbtu available in North Asia. Gasification and shipping costs are equivalent to $5 so the net back gas price is around $10 local:

Will mining more CSG in NSW solve the problem? First you would need absolute gas reservation policies to prevent more LNG plants immediately being built to ship it out. And to prevent a pipeline being built from Newcastle into the Surat Basin and thence onto Gladstone, for shipping out.

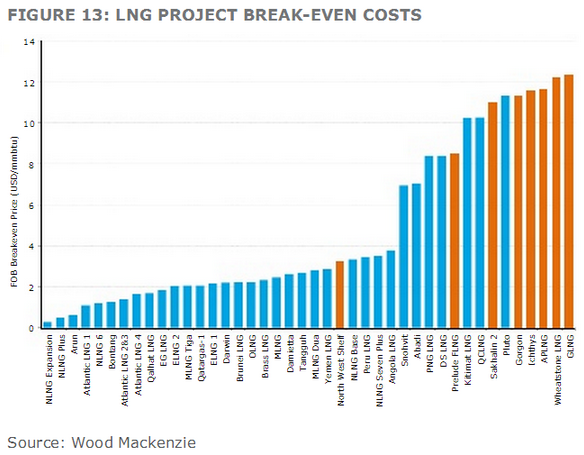

But even if you go this way, you still need to make the CSG profitable here. And it’s not cheap. Santos reckons break even is somewhere around $6mmbtu. Add some profit and you’re at $7-8. This is demonstrable in the break even costs associated with the Gladstone LNG projects, which are all around $12mmbtu:

So, your best case scenario with expanded NSW CSG production is a gas price of $7-8 versus $10 at current North Asian prices.

But, in my view, North Asian prices are going to fall. The steady breaking of the Pacific oil-price price link for LNG by Japan and the US is going bring prices down. I reckon into the $12-$13mmbtu range for spot. That brings the Australian net back price down to $7-$8, the same as if you start mining CSG hand over fist locally.

And there is another risk. One of the reasons the gas extraction costs are so high is mining boom inflation. Adding a new wave of NSW CSG projects is potentially going to feed this even more meaning both our LNG exports an manufacturing are under simultaneous competitive pressure. We should really be looking at how we accelerate cost-out deflation in these projects to ensure we can compete with North American LNG.

Nobody could accuse me of not supporting Australian manufacturing but the numbers behind the NSW GSG panic don’t add up. Correct me if I’m wrong!