The iron ore miners have been having a bumper month so far, with some stocks soaring close to their year-highs since a steady rally from June and July.

So what’s behind the rally, especially given it’s happening when the iron ore supply is increasing dramatically?

“During the September quarter, Brazil’s Vale bought 40Mtpa (million tonnes per annum) of capacity on line, FMG’s 20Mtpa Firetail hit full production. Rio Tinto added 50Mtpa and BHP entered he quarter at 220Mtpa up 40Mtpa,” says BBY analyst Mike Harrowell.

“The market had expected this supply to drag the iron ore price down, and signal the expected iron ore price bear market, but this has not happened.

“One of the reasons is the surge in steel production, and demand for steel.”

Harrowell says there has been an increased demand for steel has been revised up to 31Mt, while the rest of the world has imported 18 per cent more steel.

“So Australian supplied Chinese steel mills will supply some 40Mt more steel to the world than was expected in April 2013. This additional 40Mt of steel means 65Mt of extra demand for imported iron ore, which absorbing all the new capacity.

“This year’s iron ore supply surge was supposed to kill the iron ore price. The fact that it has not happened is a major positive for the sector.”

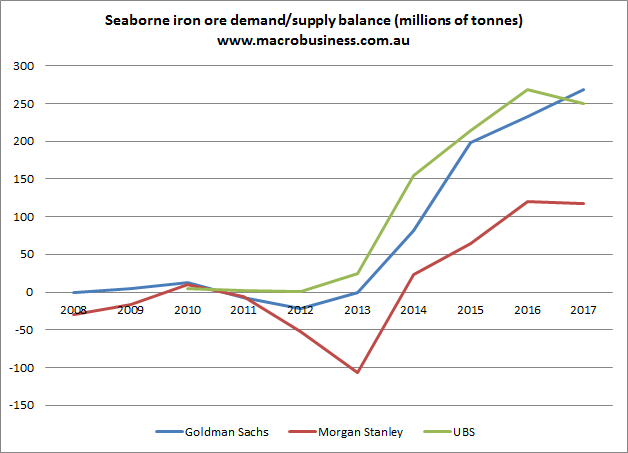

Yes it is, though it must be remembered that this is only the beginning of the supply surge and much of the Australian capacity is not fully ramped up yet. I would also like to know where the Vale figure comes from. Brazilian output rebounded in the quarter but mostly from problems not new mines. Anyway, here is the supply balance chart now:

Advertisement

The chart includes UBS’s recently updated data in which they argued:

Our view is that global demand will lift 2%pa from 2013-17E to 2,157Mt and we expect seaborne demand to lift 5%pa to 1,463Mt by 2017E. Our thesis is that China demand growth will abate as its economy matures from an infrastructure to a consumption-based economy (4% CAGR to 2017E).

On the supply side, we see seaborne supply to grow 7% in 2013E; accelerating +13% in 2014E to 1,374Mt. The biggest supply growth drivers are Rio Tinto and FMG in our view. Rio’s next 50Mtpa was commissioned in Sep-13.

Accordingly, a rapid ramp-up is expected which we think will be aided by 20Mt of inventory. FMG’s Kings mine is slated for 2013Q4, with FMG guiding to system-wide production of 155Mtpa post the 2014 wet season. Medium-term iron ore demand growth rates abate, but remain positive.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.