An interesting observation from UBS via the SMH:

Some analysts believe crude oil prices could jump more than 20 per cent if a US military strike on Damascus drags other countries into the Syrian conflict. “Our oil team think oil could go as far as $US150 if we get the all-out scenario,” says UBS global macro strategist Ramin Nakisa. “We have gone overweight energy, that is the obvious way to play it.”

In past periods of geopolitical uncertainty, highly liquid US or German sovereign bonds were the perfect investment bunker during crises from Kosovo to Iraq to Libya. Investors parked funds in Treasures and bunds to wait until the outcome became clearer, and markets rallied relatively quickly anyway.

This time the option of sitting it out is less attractive. The US Federal Reserve is planning at some stage to start winding down the huge purchases of bonds it has been making to stimulate the American economy, and growth also appears to be picking up at last in other major Western countries.

Here is more from the note:

Likelihood of Syrian intervention and production outages keep prices high

- Brent and WTI remain around $115 and $108/bbl respectively despite delays to what seems like an all-but-certain US-led military strike on Syria. Added to significant production outages in the region, we expect prices to remain supported as we head towards 4Q2013. As we said in a note last week, in the unlikely event of disruptions to oil production in Gulf producers, prices could spike sharply.

Libya really the swing factor

- The Syria debate has eclipsed the near-total shutdown of Libyan output which, added to other shortfalls, is keeping nearly 3 mb/d off the market. This may offset a possible start to QE3 tapering and refinery turnarounds. While our base case is a gradual price slide in 4Q13, we outline two other ways things could possibly go:

The bull case is Syria spillover, while Libyan production remains offline

- If the Syrian intervention somehow spills over to impact nearby Gulf production, we estimate prices could easily spike to $130-150/bbl, even if that only lasted until spare production capacity and emergency stocks were mobilised. However, if spillover is exacerbated by continued shut-ins in Libya and elsewhere, prices could stay supported and higher than our base case of $105/bbl for Brent in 4Q13.

The bear case is markets shrugging off Syria and production improving

- We think however a more likely scenario is that markets shrug off the strike after the event and that neither Syria nor its allies retaliate for fear of further escalation. In a ‘perfect storm’, Libyan issues could be resolved and production ramped up quickly, Sudanese and Nigerian oil could return too, just as refineries head into October maintenance. Unless Saudi Arabia acted quickly to cut output and balance markets, we think we could see prices come off quite quickly.

Hmmm, I agree that this is unlikely. In the past, Middle East conflicts have tended to jack oil prices on the rumour but have sold on the fact of war.

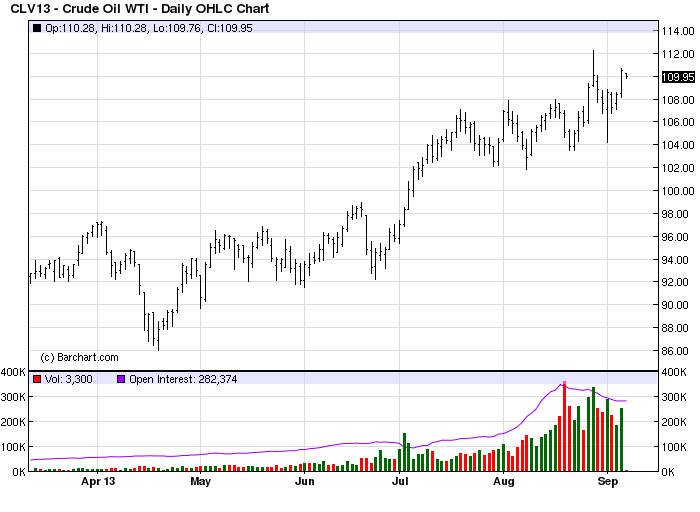

Still, technically the oil chart looks pretty strong:

And in such an outcome of an oil spike, I think it likely the Australian dollar would also fall, meaning the local hit would be $2 plus petrol prices and an oil-shock greeting Tony. At this stage, I’d consider this a tail risk.