Mac Bank has a note out on coking coal that makes plenty of sense:

In a year that has seen global steel output surprise on the upside, metallurgical coal has been the poor cousin among steelmaking raw material peers. The expected recovery toward the $190–200/t range widely expected has not transpired, with the 3Q ane 4Q13 contracts the lowest since the system began in 2010. Certainly, ex-China weakness has taken its toll, but quite simply the market has more supply than required – a situation persistent since 2011. In previous cycles, the differentiating factor for met coal has been the lack of elasticity, with steel mills reluctant to change coke blends and suppliers unable to flex supply in and out of the market. This situation does, however, appear to be no more, with increased elasticity apparent on both the supply and demand side. Certainly, a lack of medium-term supply growth continues to set metallurgical coal apart; however, the odds on a $200/t price anyime in the coming years are significantly diminished.

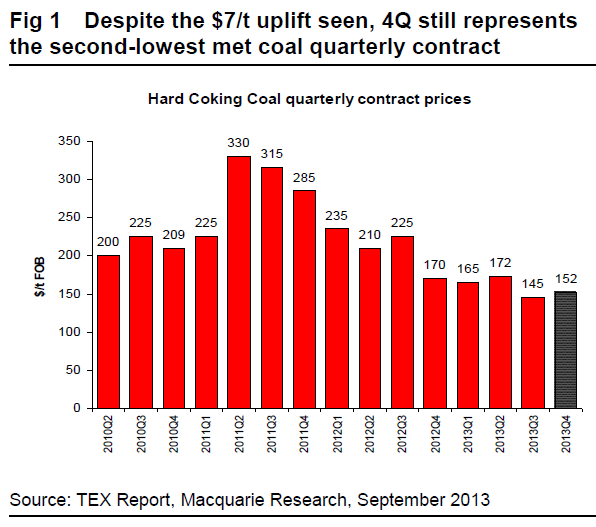

The recent 4Q settlement for hard coking coal at $152/t FOB Australia was certainly not as weak as it might have been. With spot prices languishing at ~$130/t FOB in mid-July, the market looked to be heading lower still, and in our 26 July Commodities Comment we noted that, in our opinion, 50mtpa of cuts were required to balance the market. However, with Chinese apparent production falling 70mtpa in that month alone, market balance was more than restored. Even so, the forthcoming period will still mark the second-lowest contract level since the quarterly system began in 2010, and one which is putting pressure on supply to exit the market rather than incentivising production growth.

As we’ve already seen in both coals, uneconomic production is no guarantee of shutdowns in the short term. My theory has been that we’ll see more downside (I was expecting a bottom in the $110-120 range) as BHP’s BMA adds another 15mt to production (roughly 9% of seaborne supply) next year, existing supply runs off only slowly and iron ore comes under pressure as well.

I’ll stick to that for now given the recent run up in prices has been around a Chinese restock but coking coal has shown itself capable of decoupling form iron ore and there is no doubt that of the three major bulk commodities it is best positioned long term.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.