Credit Suisse has a fascinating report out today on the global iron ore cost curve, where the price is likely to land in the next few years and where production is going to take a hit.

The key is its assessment of Chinese domestic production and how price flexible it is:

If the supply side behaves rationally, then the Credit Suisse price deck is probably too bearish. The Credit Suisse price deck implies deep cuts into the top end of the cost curve, that provide a more dramatic signal for excess supply to shut down.

…In our view, the most important question iron ore investors should be asking is whether or not China’s domestic volume will be price elastic. This will have more impact on your LT view of pricing than mulling over ‘Big 3’ ramp up profiles.

If the answer is ‘yes, entirely’, then

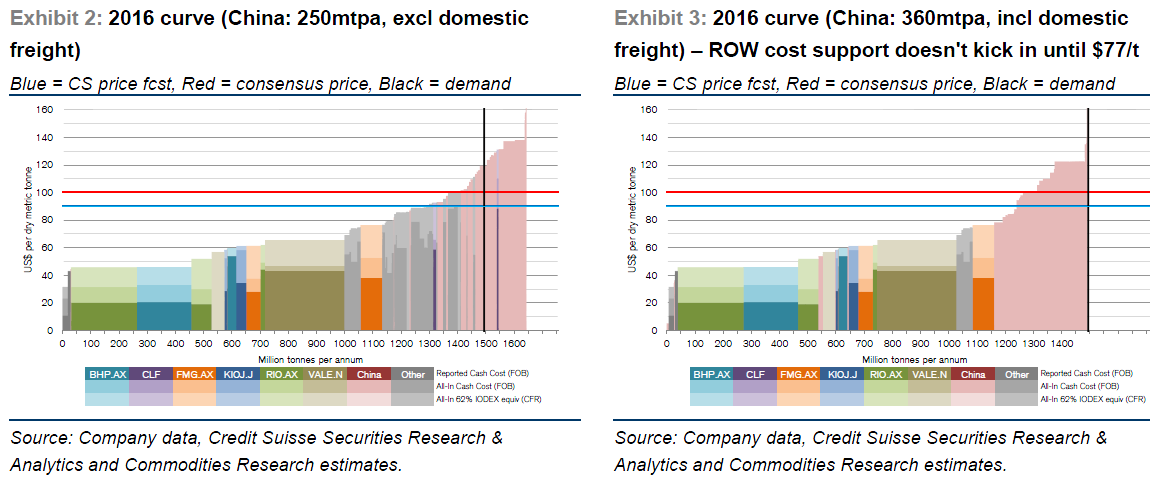

Chinese domestic supply falls to 120-126mtpa (from CSe 360mtpa in 2013, 62% equiv)

There’s only 10-20mtpa of excess ROW supply in our model, and

The 2016 cost curve support sits at $101-119/t, depending on your view of Chinese costs

But if the answer is ‘no’, then:

Perhaps Chinese domestic supply stays flat at current ~360mtpa

There’s around 260mtpa of excess ROW seaborne supply by 2016, and

The 2016 cost curve support sits at around $77/t, for the highest cost non-China supplier

The correct answer lies somewhere in between.

Chinese curve support remains at $119/t, as above

However if China is price inelastic ROW cost curve support is more relevant, and this doesn’t kick in until $77/t

Chinese production remains at 2013 levels of ~360mtpa (62% equiv)

ROW excess supply of roughly 260mtpa

Do you believe that China’s domestic supply is price elastic?

Although there is no end to the desk top analysis we can do on this subject and the range scenarions we can create, thofere is really only one conclusion we can have absolute conviction on…

The supply side will not behave rationally

Although our excel model might forecast the ‘perfect world’, game theory suggests that many sub-economic producers will continue to use shareholder capital to oversupply the market.

This will depress pricing for the entire market, and we would not be shocked to see short term price fluctuations down to as low as $50/t at some point in the next 2-3 years.

Unprofitable supply will continue to operate for much longer than it should. Labor commitments, infrastructure commitments, and supply contracts all complicate the game theory decision making process.

Correct. As the example of coal is currently illustrating, supply will not react rationally. It will be a drawn out process with, fought tooth and nail all the way down. CS sites three reasons for thinking Chinese production can linger:

Advertisement

The freight barrier. Although most iron ore investors are accustomed to thinking about mine to port rail costs and seaborne freight, we are surprised that Chinese domestic freight doesn’t get as much attention. The cost of freight in China does however ‘shelter’ a large portion of the domestic industry (~160mtpa of 62% equivalent supply comes from inland provinces), effectively creating a barrier to entry for import competition.

The Grade Debate. Statistical evidence to support a price / production relationship is weak, and we hypothesize whether China’s observable grade depletion trend could in fact be a reversable trend. If so, mining at higher grades will structurally change the shape of the cost curve as we know it today.

China’s cost base is price elastic. Although we think the price elasticity of Chinese volumes is low, a look at regional cost structures shows that the price elasticity of China’s cost base is probably one of the highest in the world. 40% of the China cost base is a function of the iron ore price. As prices move lower, these price-linked costs will decrease.

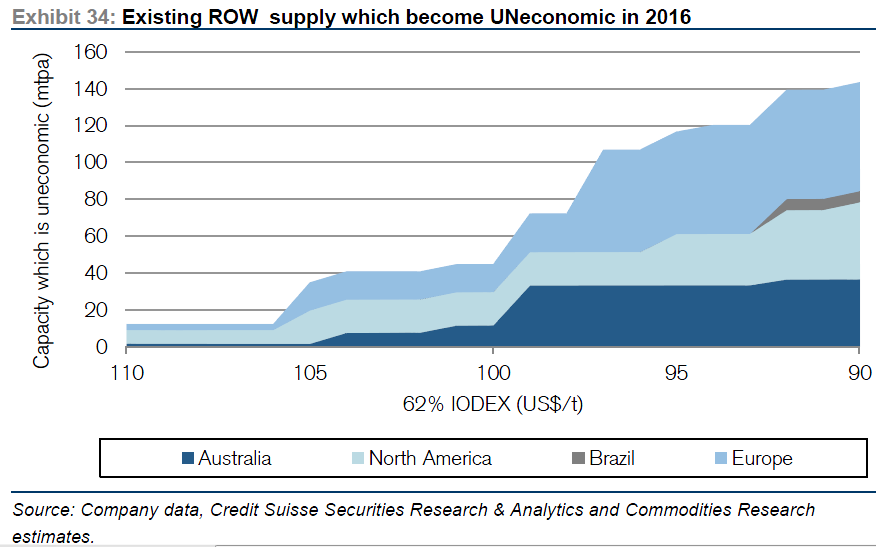

The news is not all bad, however. CS also looks at seaborne iron ore producers and concludes that much existing Australian production will remain profitable at $90:

Advertisement

Though this says nothing about individual firms and who it is that ends up owning the production! At $70 much new production plans start to get wound back as well.

In sum, this study bears out my thesis completely. Iron ore is likely to head for a long term price in the $80-90 range. But not before it goes substantially lower for longer to knock out what will be much stickier Chinese marginal supply than all assume.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.