Mac Bank runs a quite useful monthly survey of Chinese steel mill conditions. August is out and shows a sharp rise in conditions:

The August results of our proprietary steel sector survey (in which we interview 40 steel mills, 40 steel traders and 30 iron ore traders) show further improvement on the strength of July with many indicators reaching the highest levels in the two year history of the data. Mills are reporting very strong orders and a strong improvement in profitability. The traders are also positive but with steel inventory starting to flat line after consistent falls, we suspect that the August results may represent a near-term peak in market conditions as steel supply could start to weigh on prices.

Sentiment at all mills was up and orders look very strong:

Advertisement

Derived largely from, you guessed it, construction. Inventory has stabilised and intentions to buy raw materials are very strong:

Though it must be noted that the survey does not seem proportional to actual activity given we’re now higher than during the monumental restock that occurred earlier this year but that is clearly not happening in the market.

Advertisement

So, looks like good activity coming through and quite unseasonal at that.

However, as UBS argued today that does not mean that the seasonal iron ore price dip won’t occur:

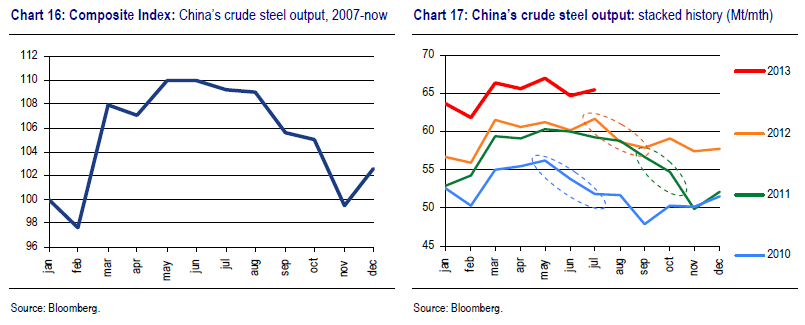

China’s steel industry is seasonal, the most active production occurring in May-Aug each year. Production rates tend to decline from Sep- Nov, reducing the need for iron ore feed.

Since the spot-price became the dominant value signal for the trade post Apr-2010, there have been 3 price corrections of >30%. These events occurred as China’s crude steel production rates roll over.

— in 2010, steel production peaked in May; production rates fell Jun-Aug; ore prices corrected 35% 27-Apr to 13-Jul. — 2011 steel production rates followed seasonal trend; production lifted May-Aug; fell Sep-Oct; ore prices corrected 48% 14-Sep to 28-Oct. — 2012 saw steel production rates peak Jul; prices corrected 41%, 11-Jul to 6-Sep.

Where do we sit in 2013? steel production rates are up 9%yoy to 780Mtpa annualised; peak is May; output remained elevated through to Aug, at >750Mtpa annualised. We continue to expect seasonal output cuts in Sep-Oct; likely to undermine ore spot prices & exposed equities – exaggerated by an Australian-led ore supply surge.

Advertisement

I reckon the dip is still likely to happen though not as severe as last year but I expect a much more muted rebound in Q4 as this surge in construction activity passes (sales have been falling for some months now), new iron ore supply begins to build and mills retain a preference for real time delivered ore over stockpiling.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.