The Macquarie commodities team have produced a neat short history of iron ore markets that is well worth a read if you’re an iron ore nerd (which includes all Australians).

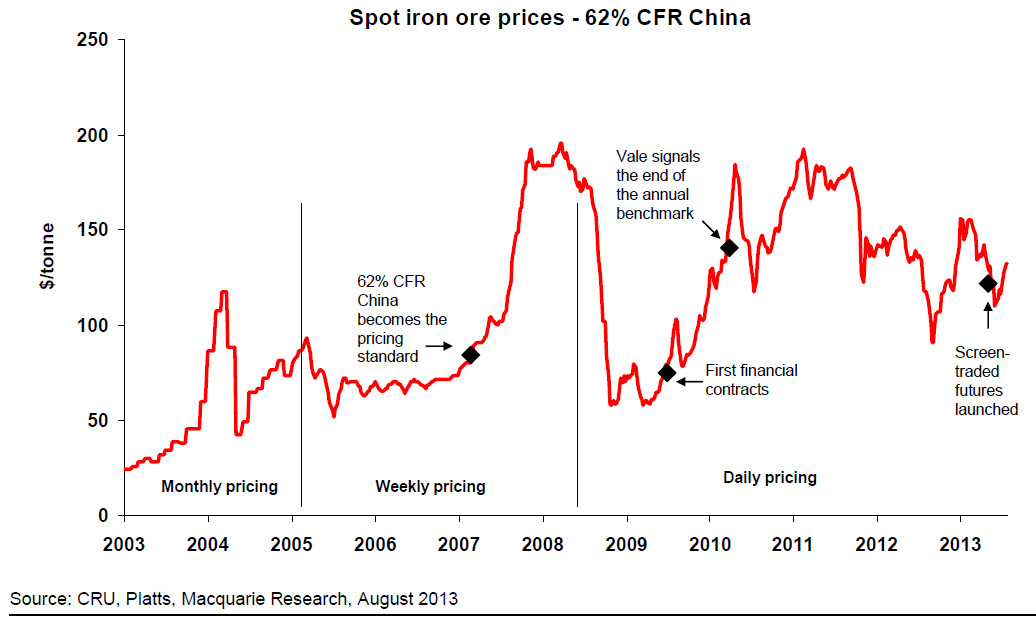

It has now been 10 years since a widely recognised iron ore spot market emerged, as Chinese steel output surged and Indian supply suddenly entered the market outside annual benchmarks. Like many youngsters, its first steps were hesitant and needed a lot of support. However, it proved to be a rapid developer, much more so that its peers, and coming into its own post the financial crisis and becoming predominant in the market. We believe the development of iron ore offers decent precedents for what may lay ahead for the potash market in the coming years. Meanwhile, iron ore’s huge potential means, should a suitable futures contract become the market benchmark, within five years its journey could lead to a place in the global commodity indices. In our view, a large part of iron ore‟s success in market transition has been down to the fact that it behaves as an extremely efficient commodity market. The feedback between demand moving, price moving and supply reacting is extremely short compared with peers. In this way, iron ore remains the purest play on actual (rather than anticipated) Chinese growth – something which is attracting more and more financial players as market liquidity increases.

The most recent development in iron ore has been rapid growth in financial contracts, with liquidity in SGX swaps roughly tripling in the past year. This has been in distinct contrast to ferrous peers such as met coal, where the physical spot market itself remains limited. Meanwhile, steel and scrap both have reasonably liquid physical spot markets, but development on the financial side has been slow going.

In its relatively short existence, there have been certain key stages of iron ore spot market development, each of which has played a part in where it sits today:

Traditional supply couldn’t keep up – The iron ore spot market started to emerge in 2003 as Chinese buyers desperately sought new sources of iron units following strong steel production growth, which had averaged 23% over 2000-2003. Traditional buyers such as Japan and Korea dominated the contracted market, and Chinese players were left chasing marginal tonnes at the sidelines of traditional supply.

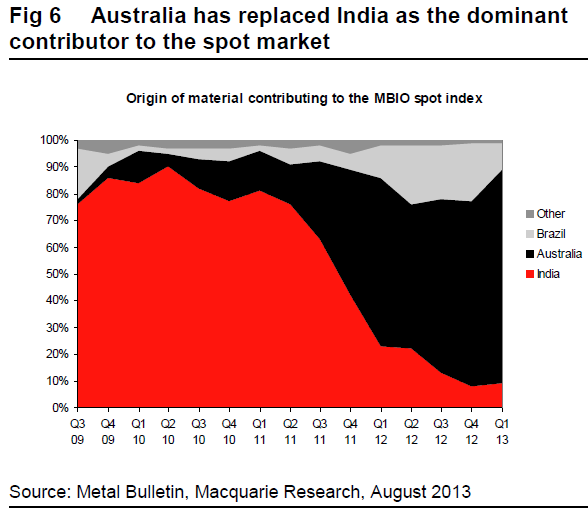

New suppliers with a different business model emerged – The other major factor in the inception of the iron ore spat market was the emergence of Indian swing supply, with the ability to react quickly to market needs without significant lead times on new supply. These Indian tonnes from Goa and Karnataka formed the backbone of the early spot market, with supply growing from 42m tonnes in 2003 to a peak of 119mt in 2009. Without this growth, the iron ore spot market might still be more akin to metallurgical coal.

Price discovery started making its way into market monitors – With iron ore spot becoming an increasingly referenced price, market analysis firms increasingly started reporting it on a semiregular basis. CRU reported 63.5% Fe monthly spot prices from 2003 (the time period reflecting the relative illiquidity of the market still) and increasingly when annual benchmark negotiations came round these were used as a reference point for negotiations, making the iron ore spot market more widely followed among all interested market sectors.

Prices based on port of delivery rather than port of origin – One interesting development in price discovery related to how the price benchmarks were constructed and reported. Given that true “spot” material is generally sold as close to the end customer as possible to minimise lead time (and risk), it was thus natural that prices started being reported on a CFR China basis rather than the FOB export port assessment used for annual contracts. The greatest significance of this was on how freight played into the price – this then effectively became a cost to the miners rather than a cost to the buyers.

Price discovery became more frequent… – With market liquidity growing, market assessments naturally became more frequent. 2005 saw weekly prices published, then in June 2008 Platts started to publish daily assessments, with Metal Bulletin and The Steel Index following suit. Also, the standard assessment for iron ore had become 62%Fe, reflecting the prevalent grade in the spot market.

…supporting the first financial contracts – With price assessments on a daily basis, credit departments started to feel a little more comfortable regarding iron ore market risk, and financial markets started to emerge. SGX listed their 62% Fe swaps in April 2009, which swiftly became the dominant cleared contract in the market.

Benchmarks lose relevance in the physical market… – The global financial crisis proved a defining moment for iron ore development. With credit tight and the spot price well below benchmark, some (though certainly not all) steelmakers defaulted on benchmark tonnages and chose to purchase on the spot market. As such, the benchmark system for iron ore did not withstand the physical market stress test, becoming effectively a one-way option call for buyers.

…and are no longer supported by producers – With BHP already showing support for market clearing prices in lieu of the benchmark, the final nail in the coffin of the annual benchmark came in February 2010, when Vale altered their stance. This was iron ore‟s „potash moment‟, with the potential impacts noted in the Commodities Comment of that day.

Physical contracts become increasingly spot-market linked… – Over the course on 2010-11, the vast majority of physical contracts became spot linked with a variety of quotational periods used; quarterly lagged pricing, monthly lagged or marked to market based on the daily index price. As a result, customs values have move ever closer to spot price values as the price lag has reduced.

…while the price discovery players battle for supremacy – With this development, the competing indices fought to convince producers theirs was to most robust. In many commodities, a single index or combination of indices has become predominant. This is not yet the case in iron ore, though with the correlation between index values so high this problem is not critical.

Meanwhile, financial contracts have grown… – In April 2011, we noted that ferrous market contracts, led by iron ore, were slowly gaining traction in terms of interest. Participation continued to grow, with over 5m tonnes of cleared and OTC trading in March 2011 and open interest up 207% YoY.

…and grown – However, the last 12 months has really seen iron ore volumes have taken off. This has been most notable on the SGX, where volumes and open interest have consistently hit new monthly highs over the past year, but also on the CME contract. Liquidity tends to bring liquidity, and we have certainly noticed a pick-up in the number and depth of iron ore financial market participants, with critical mass now having been achieved.

The physical market has coped with removal of a key support function – It is also worth noting that the physical iron ore spot market today looks very different from that 4-5 years ago. Indian exports have dwindled due to rising costs and prohibitive restrictions, but despite the removal of this „backbone‟ iron ore trade has continued to increase. With the vast majority of new supply tonnes coming out of Australia and indeed Brazil sold on a tender basis, Indian supply has not been missed in terms of market depth.

Certainly, the market transition is unlikely to stop here, and we see a number of developments continuing to shape iron ore in future years.

The CME recently launched the first screen-traded futures contract for iron ore, with SGX also launching a futures contract. While physical screen trading has become more commonplace, an active futures contract is the next natural step for iron ore. The lack of interested buyers (particularly ex-China steel mills) is a headwind to this; however, we would expect to see further traction in the coming 2-3 years.

As futures markets grow, we would expect to see increased levels of producer hedging. This will still be small scale at first, and less likely to involve the larger players, but junior operations are increasingly likely to take advantage of the upward swings that iron ore offers to manage the risk for marginal operations. There may also be some consumer hedging as well, but as mentioned above, despite the glaring need to manage raw material price risk in what is increasingly a conversion margin business, most steelmakers remain disinterested in utilising financial tools to do so.

Taking a longer term view, with an active futures contract in place iron ore could well find its way into the global commodity indices. Compared to other industrial metals, iron ore‟s market value is significantly larger, while its end use is well understood. It could also serve to make these indices less US-centric than is currently the case, and thus open up a wider investor base. Certainly, there are significant market changes to take place before this becomes the norm; however, given the current pace of development there remains potential for this shift in the next 5-10 years, bringing increased liquidity into the iron ore market.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.