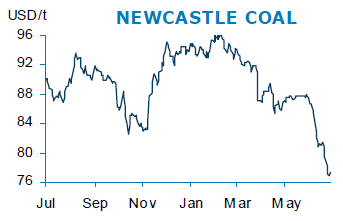

Bulk commodity prices improved on Friday, but ended the week softer. Iron ore prices have settled around the USD116/t level in line with a pick-up in Chinese steel prices and Baltic capesize rates, which were up another 18.8% last week. However, the mood is still cautious in China as rumours of ongoing tight credit conditions and potential defaults in the thermal coal market weighed on already bearish sentiment. Most thermal coal players are still reportedly reluctant to book cargoes, with prices still declining. That said, Japanese utilities are taking advantage of lower prices, with Hokkaido Electric last week buying 5 panamax’s (375,000t) of Australian coal to be delivered in Q3. Reports suggest Australian producers are surprised at the sharp drop in Newc prices over the past two weeks, but suggest a declining AUD is helping to buffer the downside and point to a bottom in the low USD70s.

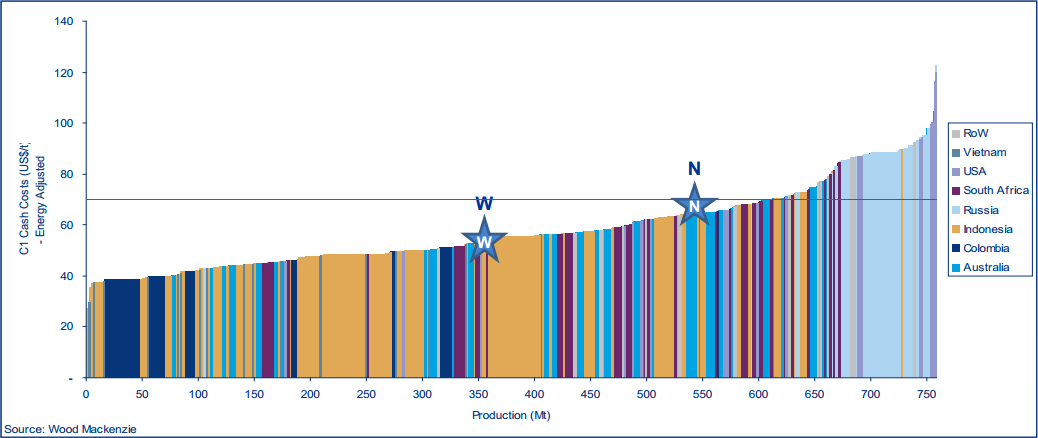

That’s possible. Note in the below cost curve that at $70, 20% of global coal is in the red:

Even some Australian mines get shaky. But don’t forget that most thermal coal is priced in quarterly and longer contracts which are much higher. So there is a chance that thermal coal will have to sit at $70 for quite some time to take out North American production.

Advertisement

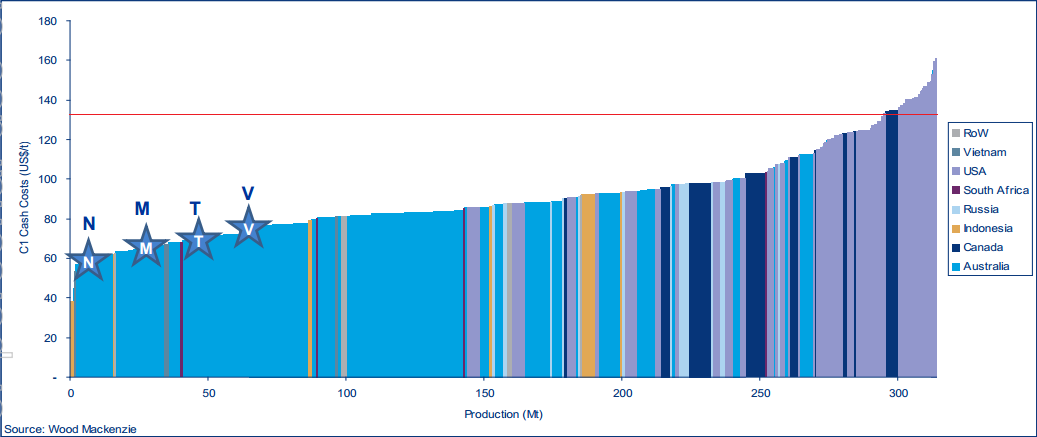

Coking coal is also sitting at its low of $134. It’s cost curve shows that more pain is ahead:

Note that about 10% of global production is in the red at current prices. I’m targeting sub $120 to really put the squeeze on. The same contract dynamics apply.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.