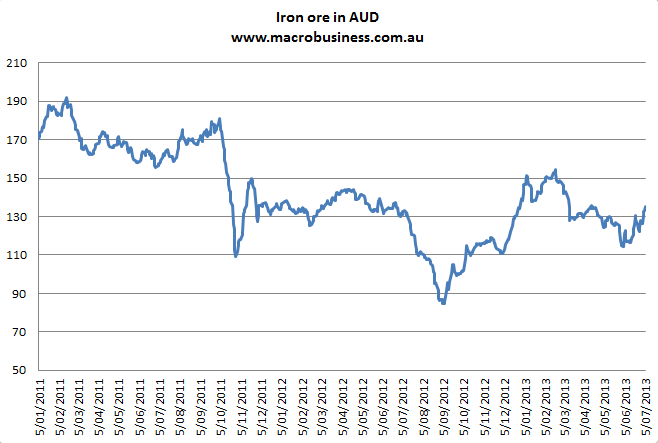

Some readers have been asking for the below chart, iron ore in AUD since its peak in 2011:

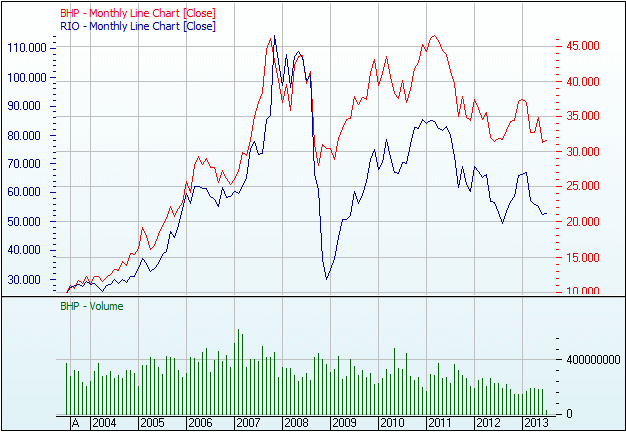

A nice little bounce there, not that it’s helping the big miners:

Advertisement

Both Rio and FMG are trading at heavy discounts to their 2011 prices when iron ore was effectively the same price and volumes are much higher now than they were then.