The Bureau of Resource and Energy Economics (BREE) is out with its quarterly commodity forecasts and as I’ve noted before the tendency of the Bureau is towards optimism (making our pathologically positive PM proud). As a result it has had to slash its projections for the financial year just ending:

The net result of actual and projected falls in key commodity prices is that BREE’s forecast Australian resources and energy export value in nominal dollars for 2012–13 has been adjusted downwards from $186 million in the March release of the Resources and Energy Quarterly to $177 billion in this release.

But wait, there’s more! Next financial year we’ll boom again:

An assumed depreciation of the Australian-US dollar exchange rate for the financial year 2013–14 will provide additional support for Australian dollar value of resources and energy exports. For the next financial year, BREE forecasts resources and energy exports to increase relative to 2012–13 in nominal dollars by about 11 per cent, or some $20 billion, to total about $197 billion.

Advertisement

So, let’s look at the assumptions and see if BREE is following the PM’s instructions to drop a prozac. On iron ore the answer is, yes, BREE has been at the Mummy’s forbidden cupboard:

In 2012–13, Australia’s export volumes of iron ore are estimated to have increased by 13 per cent, relative to 2011–12, to total 533 million tonnes. Despite the substantial increase in export volumes, export values of iron ore in 2012–13 are estimated to have declined to $57.3 billion (see Figure 3). In 2013–14, a forecast increase of 15 per cent in export volumes and an assumed lower Australian dollar exchange rate are forecast to result in export values increasing by 17 per cent to $66.7 billion.

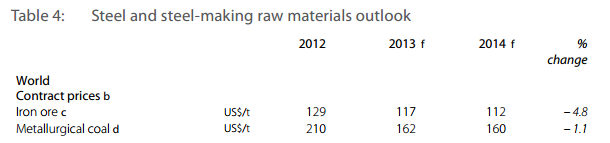

As I say every time this report comes out, you can’t have it both ways. Either volume growth is weak and prices strong or vice versa. Here are BREE’s price predictions for contracts:

Advertisement

And its volume predictions:

To state the obvious, a 15% rise in volumes is quite unlikely to result in a $5 fall in price. The first point to make is that Chinese imports will hardly grow next year. Second, Australian volumes received a huge boost from India dropping out this year. In short, there was a displacement effect yet the price still fell much further than BREE’s forecasts for next year. A 15% rise in iron ore volumes in the next year will mean a mad dash for market share and much heavier price falls.

Advertisement

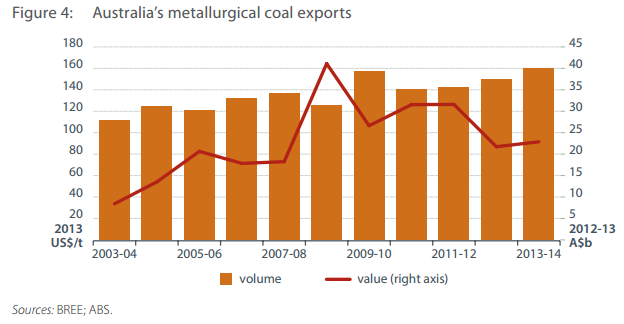

The coking coal forecasts are also pie-in-the-sky. The current spot price is almost down to $130. There is no sign of price stability as north Queensland volumes ramp up after the floods and industrial action and I expect that prices will continue to fall towards a bottom somewhere around $110 next year. That’ll be low enough to knock out all sorts of US competitors so I do expect a decent volume story for Australia but the price is going to be ugly while it all happens.

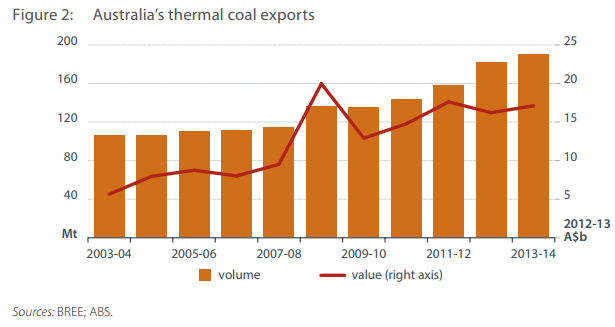

On thermal coal it’s a similar story if a bit less painful:

Advertisement

Australia’s exports of thermal coal in 2012–13 are estimated to have totalled 182 million tonnes, an increase of 15 per cent relative to 2011–12. This increase is estimated to have been more than offset by lower export prices to result in export values decreasing to $16.2 billion. Exports are forecast to total 190 million tonnes in 2013–14, an increase of 5 per cent. Export values are forecast to increase by 8 per cent, relative to 2012 13, to total $17.5 billion, as a result of higher export volumes and an assumed lower Australian dollar–US dollar exchange rate offsetting forecast lower prices in 2013–14.

I can see 10% downside in thermal coal prices but BREE is closer to the mark here.

On LNG, things are more settled for now:

Advertisement

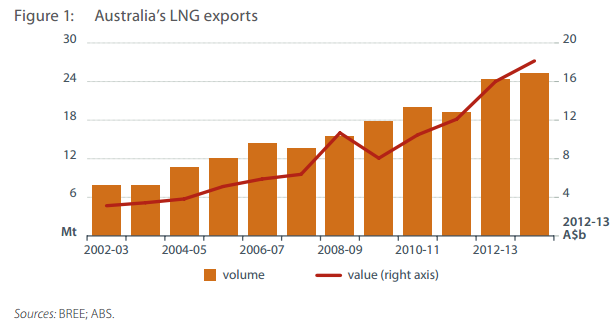

Australia’s LNG exports were 19 million tonnes in 2011–12. Australian exports of LNG are forecast to increase by 26 per cent in 2012–13 to total 24 million tonnes. In 2013–14, Australian exports are forecast to increase by a further 4 per cent to total 25 million tonnes as a result of increased production at the Pluto facility. The value of Australia’s LNG exports is forecast to increase to be about $15.2 billion and $18 billion in 2012–13 and 2013–14, respectively (see Figure 1). Forecast increases in export earnings are the result of expected increases in Australian export volumes and projected higher LNG prices over the outlook period from 2012–13 to 2013–14.

That’s fair enough given the price contracts in place.

In total, my guesstimate is that Australia’s mineral exports will fall in 2013/14 by about the same amount they did this year with a flat result in energy. The upside risk to that forecast is the Australian dollar, which could offset the dump if it gets low enough, fast enough. But of course, BREE ain’t arguing that.

All in all, BREE’s update reminds me of this, don’t know why.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.