Slowly but surely the better minds of Australian market economics are turning up the pitch of worry. NAB has completed a very useful analysis of the last week’s BREE major projects report and the results are no different to my own assessment: frightening. However, the detail is interesting.

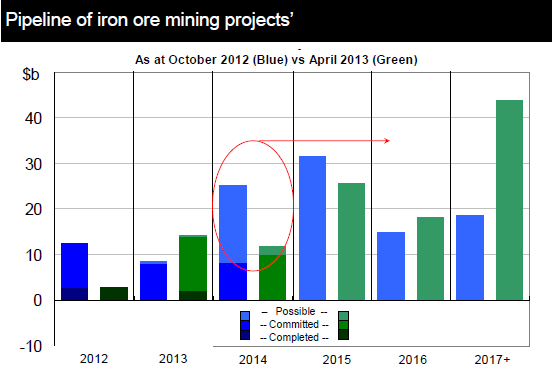

First is iron ore:

Overall, the value of committed iron ore projects has fallen by $4.2 billion relative to October 2012, representing the completion of five projects, to a total of $22 billion as at April 2013. There are currently 21 iron ore projects at the feasibility stage in the pipeline, with a combined value of $47 billion, up from $45 billion last October, and another $35-56 billion in less advanced projects (publicly announced), including two new projects: Fortescue’s Nyidinghu project (around $2 billion and 30 million tonne capacity), and Macarthur Minerals’ Moonshine project ($2.5 5 billion and 10 million tonnes capacity). However, delays have shifted the pipeline of uncommitted projects more heavily towards the out years of the outlook horizon – a reflection of the number of projects that have become ‘dead in the water’ as their viability is reconsidered. An example is the $7.4 billion West Pilbara project (expected to add 30 million tonnes to capacity) which is now unlikely to reach completion before 2018 (previously expected in 2014 and was downgraded from being at the feasibility stage to the publicly announced stage).

As I’ve argued many times, I see little prospect of more iron ore projects. We are already headed to $80 per tonnes on current committed expansions by next year. Perhaps out a few years there could be more, but Rio’s Pilbara 360 project is now a giant weight sitting on all prospective producers. It can produce 70 million tonnes in the $20 cost range, its infrastructure component will be ready in short order, so whenever the glut is sufficiently absorbed it will proceed swiftly to expand mine capacity (if not just go ahead). Nobody else can expand until it does and is absorbed. In the mean time, in my view, high cost production will need to rationalise.

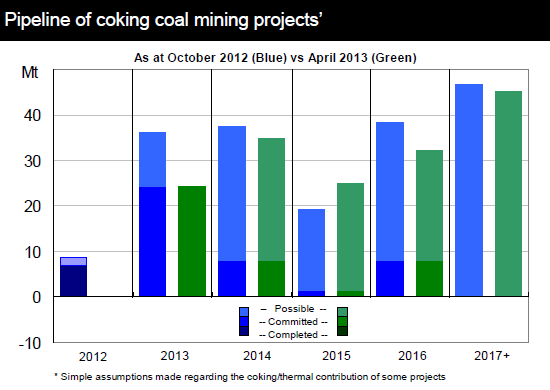

Next is coking coal:

Advertisement

With Australia accounting for around half of global seaborne coking coal supply, planned additions to Australian output are important to global coking coal markets as well as Australia’s investment pipeline. While the pipeline of new projects was relatively modest last year, committed projects are expected to bring an additional 30 million tonnes of capacity online over the next couple of years (representing around 20% of 2012 export volumes). The total pipeline of potential projects suggests a potential addition of 161 million tonnes to capacity, essentially doubling exports over the long run, although this is an unlikely scenario.

Despite decent ongoing demand, unlike iron ore the coking coal price never rebounded after last year’s plunge and has now fallen to post GFC lows near $140. In other words, the glut in coking coal capacity is already here and the lower prices needed to shakeout high cost production has begun. Most Australian production is sub $120 on the cost curve, with the US most vulnerable, but the shakeout period will still deter investment until prices reliably stabilise.

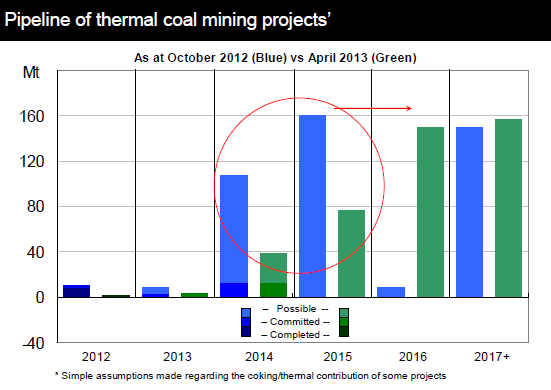

Then thermal coal:

Australia is the world’s second largest exporter of thermal coal (behind Indonesia) contributing almost 20% of global seaborne coal. While the pipeline of new projects is relatively modest this year, later years are punctuated by significant potential capacity expansions, although very little has been committed. Also, there have been a number of delays announced which have pushed a significant proportion of ‘possible’ projects (either at the feasibility or publicly announced stage) back to 2016 and beyond.

Similar story to coking coal in terms of market dynamics though the causes are different with gas displacement a factor and China’s shift away from high carbon energy. The prospects for thermal coal are worse than coking over the longer term with Australian production higher on the cost curve. Again the US is most at risk, and Russia. Also again, expect no new investment until prices reliably stabilise, which we may be closer to but only if the shift by China is not too great.

Advertisement

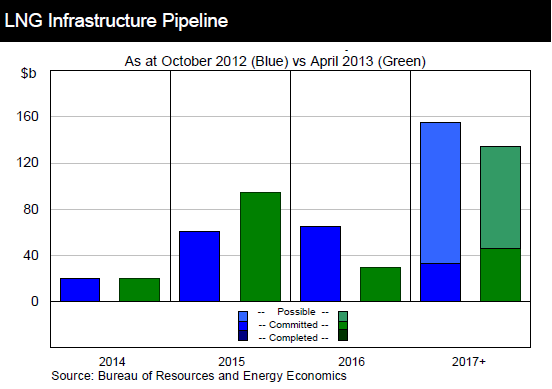

Finally, LNG:

While the number of LNG projects in April 2013 is unchanged from October 2012, the value of these projects has swelled by $10.5 billion, largely reflecting cost overruns at Gorgon LNG ($9 billion) and Australia Pacific LNG ($1.7 billion). BREE estimates that cost increases for LNG projects have been the largest of all commodities by value, at around $20 billion above FID estimates, or approximately 10% of committed LNG project values and a significant share of cost increases for all mining projects ($29 billion). The value of projects at the feasibility stage declined by $32 billion to $72 billion in the six months to April 2013, reflecting a number of projects – including the Browse LNG and Sunrise LNG projects – being pushed back to the publicly announced stage. Despite this shift, the value of LNG projects at the publicly announced stage was between $1.4 billion and $3.9 billion lower in April 2013, reflecting several projects progressing to the feasibility stage and the removal of the Pluto LNG Expansion (Trains 2 and 3) and Arrow LNG Expansion (Trains 3 and 4) projects from the list.

A major development in April 2013 was the announcement by Woodside Petroleum (on behalf of the Browse LNG project joint venture) to no longer develop the onshore LNG processing plant in north-west Western Australia based on unfavourable project economics. Instead, Woodside Petroleum plans to develop a floating LNG platform for the Browse Basin, enabling the processing of offshore gas. Floating LNG technology offers a less capital intensive and lower cost option that is completed entirely offshore. As a result of the decision to develop offshore, the Browse LNG project is likely to cost much less than the initial estimated cost of $36 billion.

Better news here, though mixed. The pipeline is less disturbed and will hold up for a few years. An echo boom in FLNG is possible though still speculative given the shift of US gas into North Asia. It is unlikely to feature before 2017 and when it does deliver the benefits will be far fewer because most of the investment phase benefits will go to Korea.

NAB’s conclusion:

Advertisement

BREE’s major project listings update combined with ABS data on capex and exploration expectations suggest that mining investment may be approaching a turning point. On the basis of past engineering construction commencements, there are reasons to believe that there is a risk of a decline in 2014 big enough to take 2 percentage points off GDP growth in that year unless another ‘mega’ project starts soon. Given NAB’s expectation for mineral and energy prices to fall further over the forecast horizon, the underlying trend in mining project commencements is likely to be negative.

There are a number of challenges facing the resources sector that are expected to reduce the value of committed projects as well as the amount of future capital expenditure undertaken in Australia. Investment at the committed stage remains dominated by ‘mega’ projects with a valuation greater than $5 billion, with these projects accounting for around 80% of committed projects. ‘Mega’ projects promote economies of scale in the production process and reduce average costs of production. However, no new ‘mega’ projects were added to the list of committed projects over the six months to April 2013, there has been an emerging trend for ‘mega’ and large projects at the feasibility stage to be either cancelled or to revert back to the publicly announced stage. Given our projection for minerals and energy commodity prices to continue on their downward trajectory, the outlook for the commencement of additional ‘mega’ projects looks grim. As previously commenced ‘mega’ projects reach completion, the stock of committed projects is expected to become dominated by a larger share of smaller more costly projects, which will limit the amount of mining capital expenditure able to be undertaken and the rate at which construction can occur. While the investment pipeline remains enormous, there is a real risk that the rate of decline in capital expenditure will be more pronounced than previously anticipated, having a more severe impact on the Australian economy than currently forecast.

I would paraphrase that as “uh oh”.

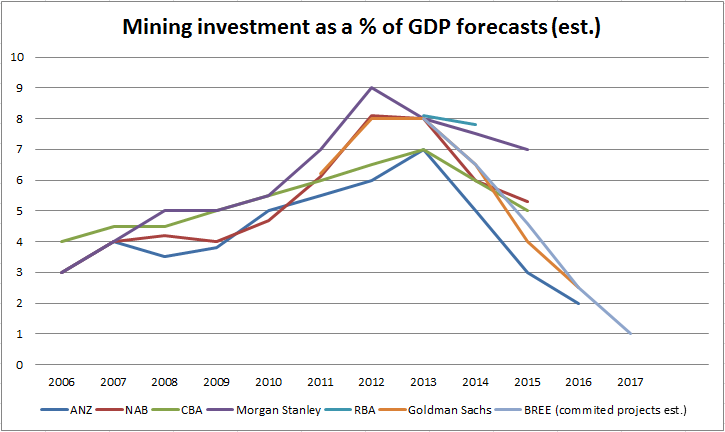

Here’s my updated guide to various mining cliff forecasts:

A substantial fall in the dollar and real exchange rate reduction could aid in reducing the slope of the cliff by improving the economics of projects and raising the prospect of taking market share from higher cost producers. But unless we actively seek it out it will likely be paced with ongoing declines in Chinese demand growth, rendering the effect moot.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.