Ominously, analysts noted that the gold price has only suffered two sharp declines in the past five years, and both were at times of deep global instability. In July 2008, the gold price fell by 21 per cent, in what turned out to be a precursor to the global financial crisis. In September 2011, the gold price again collapsed by 20 per cent at the worst point of the euro zone debt crisis.

However, some argue the gold market is oversold, and that the extremely negative sentiment towards the precious metal could see the price move higher. They argue that since the beginning of the year, global central banks have ramped up their money-printing, while the recent Cyprus bailout shows the risk of keeping money in banks.

Certainly, many leading investors, including John Paulson, the US hedge fund manager who made billions by shorting the US housing market ahead of the financial crisis and who has made a huge investment in gold, continue to keep the faith. According to the Financial Times, John Reade, one of the partners of Paulson & Co said the hedge fund remained confident in gold’s outlook. “Federal governments have been printing money at an unprecedented rate creating demand for gold as an alternative currency. It is this expectation of global paper currency debasement which makes gold an attractive long-term investment”, he said.

Advertisement

I’m inclined to agree with the view on gold. But the reason why is not because we’re tumbling into some unforeseen, terrible and imminent recession. It’s because we’re going through the mid year slowdown that we have repeated every year since the GFC. If it gets bad enough we’ll see more QE. There is no mystery here. As I’ve written all year and repeated last week:

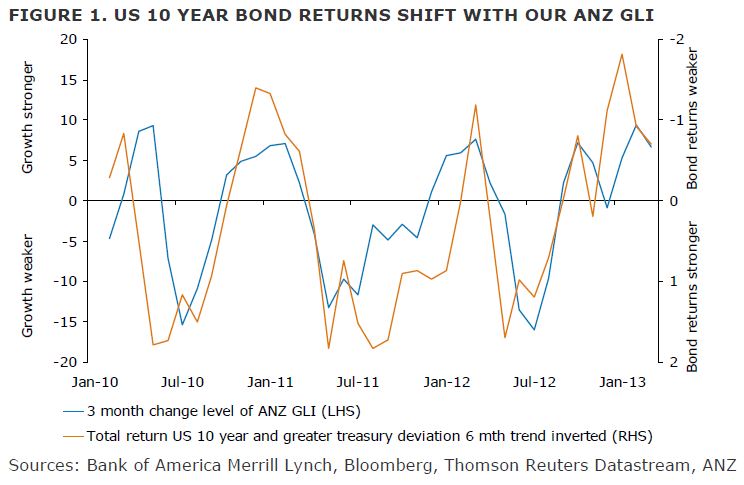

The clearest representation of this is in the ANZ’s Global Leading Indicator for manufacturing (charted against US 10 year bond) which is oscillating with the regularity of a metronome:

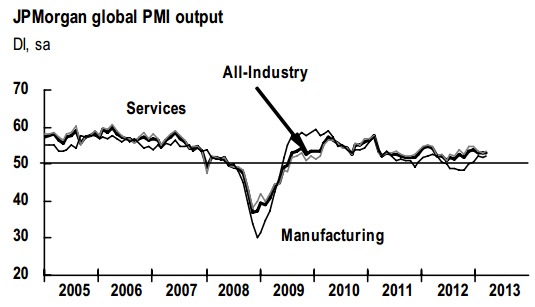

Another way to look at it is through the JP Morgan global PMI, which is also bouncing and rolling over like clockwork:

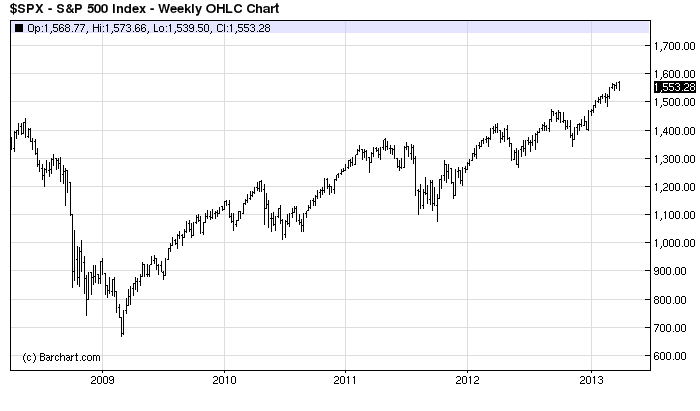

I expect we’ll see fading data for the next six months. As such, stock markets will struggle to go higher from here. Indeed, the mid year slump has also been a feature of the S&P500:

The pattern appears to be driven by the US economy (although there’s a big chicken and egg problem here). The manufacturing ISM shows the same pattern:

This is a simple inventory cycle. US consumers can’t spend like they used to when their asset markets only went up and made them feel rich. Instead, they go through mid year spasms of saving then loosen up again at Christmas. The economic effects of this pattern have led the US Fed to boost the cycle in Aug/Sep with more QE. Barring something unforeseen like a leveraged ETF meltdown feeding back into global banks, the same pattern could and will repeat itself if necessary.

Advertisement

But according to the Kouk, we are all just corks tossed in the heavy seas of the unknown. No wonder. Just a fortnight ago he saw rate hikes all over. Now we need cuts apparently:

International investors are still upbeat on Australia, its economy and its macroeconomic policy settings, which are underpinning the dollar at a time when it should be falling sharply.

The Reserve Bank said it is powerless to do much about it, other than set monetary policy to an easy setting to mitigate the effects on the real economy from the Australian dollar being so over-valued. The government can’t do anything about it either as it remains unquestionably committed to a floating exchange rate, as it should of course.

The dynamics are suggesting that the Reserve Bank may well need to cut interest rates yet again and soon. The recent uptick in unemployment, the low inflation climate and soggy business conditions all point to some downside economic risks ahead. The Chinese data in addition to the sharp fall in commodity prices risks exacerbating these downside risks. While an interest rate cut wouldn’t do much other than take a few more ticks off the level of the Australian dollar, it might set up the domestic economy for a period of decent growth even if commodity prices remain weak or fall further.

For heaven’s sake, there are lot’s of things we could be doing:

Advertisement

RBA should print money for other central bank portfolios

government should be installing Tobin taxes

macroprudential policy should be debated

the capital gains on investment property should be cut

land use should be liberalised

export incentives should be introduced

The Kouk’s suggestion that we just cut rates again to boost his 10% per annum blowoff in property specufesting is absurdly limited.

Of course markets are now pricing almost two rate cuts in the year ahead, as they should be in terms of the economic outlook. They should never have done anything else:

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.