Last week’s dour US data, with large falls in the ISM for manufacturing and services, as well as Friday’s big miss in employment is no surprise to me.

Regular readers will know that I’ve been arguing for many months that the current round of hope for global growth is no more than the same Christmas inventory cycle combined with a Santa Clause stock rally exaggerated by QE that we’ve seen every year since the GFC. That doesn’t mean underlying conditions aren’t improving, just not as fast as these year end spurts suggest.

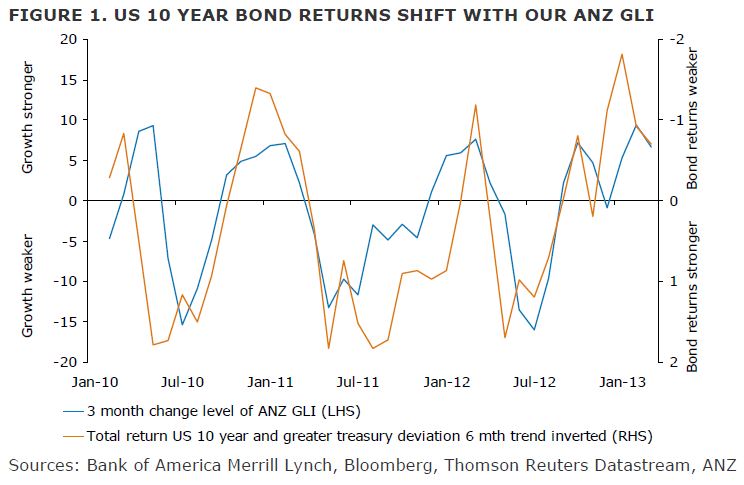

The clearest representation of this is in the ANZ’s Global Leading Indicator for manufacturing (charted against US 10 year bond) which is oscillating with the regularity of a metronome:

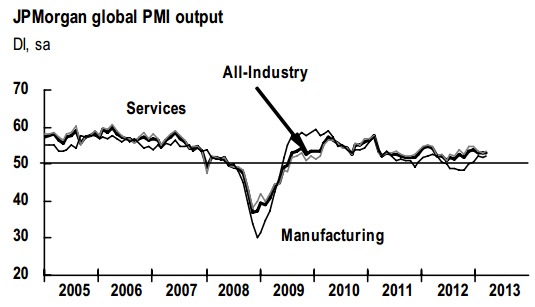

Another way to look at it is through the JP Morgan global PMI, which is also bouncing and rolling over like clockwork:

And is now easing:

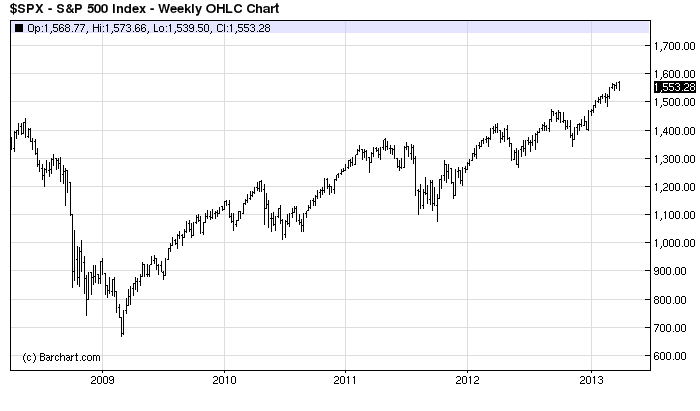

I expect we’ll see fading data for the next six months. As such, stock markets will struggle to go higher from here. Indeed, the mid year slump has also been a feature of the S&P500:

The pattern appears to be driven by the US economy (although there’s a big chicken and egg problem here). The manufacturing ISM shows the same pattern:

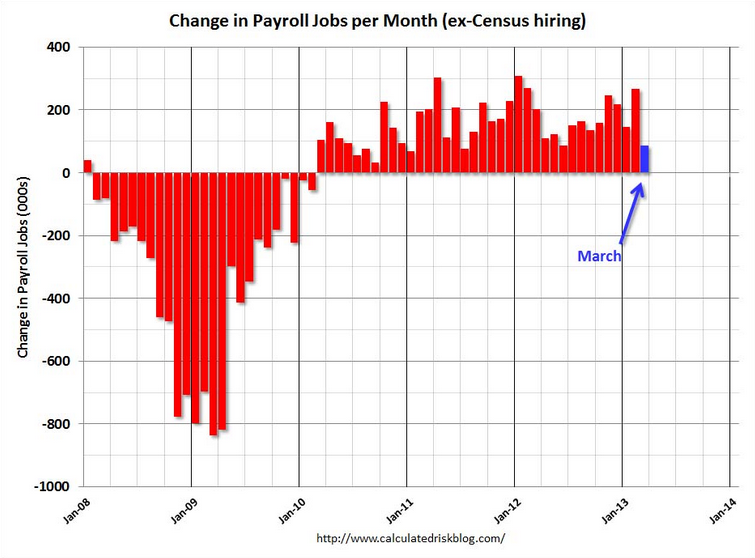

As does employment:

The hope is stronger this time around that a more consistent growth pattern will emerge with US housing leading the charge. But I don’t think so, which is actually good news (in the short term) in that the global growth slump will prevent US bond yields from blowing out and choking the recovery though higher mortgage yields (in the longer term of course that’ll present its own problem).

Commodity prices like copper are already signalling the slump. If it gets bad enough, as it has in each of the past three years, then you can expect another round of QE to step in the latter part of the year, just as we’ve seen with 2010’s QE2, 2011’s Operation Twist, and 2012’s Qe3/4.

For stock punters, it doesn’t look like bad time to take profits. Or, conversely, to prepare to buy the dip.