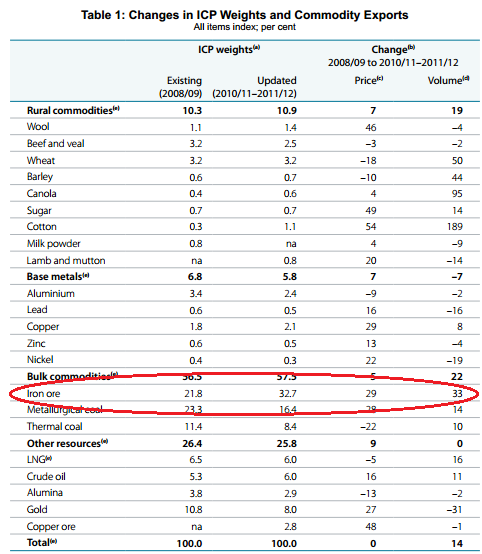

The RBA Bulletin released today had an interesting article about plans at the central bank to change its Index of Commodity prices to better reflect the new reality of dominance by steel input products. Here is the table with the previous and current weightings:

Between them iron ore and coking coal now constitute 49.1% of the index, up from 45.1%. The most comparable country with a minerals dependency this narrow is Chile and copper, which constitutes 49% of their exports (though there are others with oil dependency of course).

To manage the volatility of such a dependence, Chile employs the Economic and Social Stabilisation Fund which:

has macroeconomic stabilization objectives. It has the aim of accumulating excess copper revenues when the price of copper is high in order to channel revenues into the budget when the price of copper is low, thereby smoothing out government expenditure. As a Stabilization Fund, it has a lower risk profile in terms of its investments because it must take a short-term view due to liquidity concerns. The strategy is to be gradually implemented and external managers will be responsible for part of the fund. The fund primarily invests in currencies and foreign government agency bonds & financial institution bonds.

Nah.