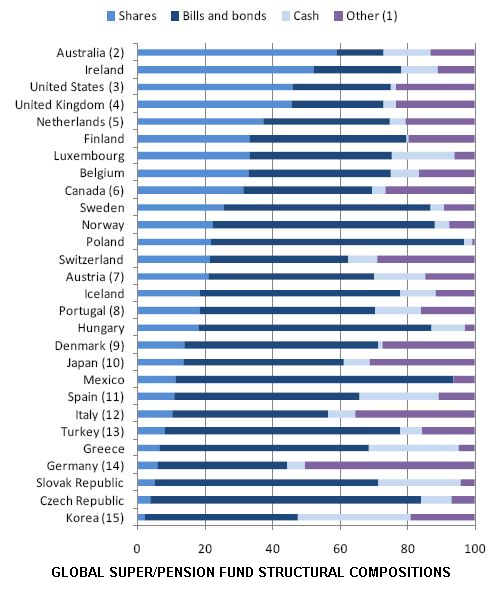

Australians (particularly their fund managers) have traditionally had a love affair with equities – in fact we have the largest portion of our superannuation wealth invested in them than any other comparable country, as shown in this graph (h/t to The Prince).

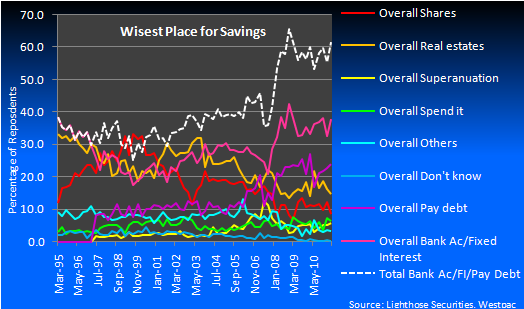

However the GFC ,combined with the last 6 months of Euro-trashed share prices, has seriously strained the relationship. We are now far more wary of shares and their volatility, with less than 10% of Aussies believing shares are a good place to put their money. This compares with almost 20% prior to the GFC:

As a result, there has been a renewed interest in fixed-income investments for retail investors and self-manager super funds. This interest should only grow into the future, as the baby boomers start to retire and op for the certainty of fixed-income assets over the cardiac-inducing volatility of shares.

So, let’s take a look at the basic fixed-income options available to Australian retail investors.

Cash Deposits

Anyone can rock into a bank today, open up a fixed-interest account and start earning interest on their money. The last decade has seen a large increase in the options available for cash accounts, with high-interest, at-call online accounts becoming very popular. That said, term deposits are still a cash staple and usually pay the highest rate of interest. The at-call accounts are typically variable rate and will rise and fall with the cash rate set by the RBA or, less frequently, when banks decide to change their rates outside of an RBA cycle.

At the moment, ANZ offers a flat 6% on their at-call “Progress Saver” account whilst RaboDirect offers 6.4% for a 5-year deposit.

A good resource for comparing the interest rates available on different bank products can be found at Info Choice.

Corporate Bonds

Companies issue bonds as a form of debt financing. It allows them to directly tap the market for a loan rather than approaching a bank or formal lending institution. The company will take an investor’s money (i.e. you buy the bond) during the bond’s initial public offering and in return the company will pay you either:

- A fixed income – these are called “Vanilla Style” bonds, or

- A variable income – typically referenced to a short-term benchmark rate such as the 90-day bank bill swap rate plus a certain percentage. These are called Floating Rate Notes, with Woolworths Notes II being a recent example I covered in MB

The sale price at offering is called the face value. The payment on this face value is called the coupon. The coupon divided by the face value gives the bond’s coupon rate. So a $100 bond with an $8 coupon will give a coupon rate of 8% ($8 divided by $100). Coupon rates are always quoted as a % of the original face value of the bond (which may differ to the price at which the bond trades – see below). So the coupon rate does not change for vanilla style bonds.

Typically, a bond will have a maturity date when the original face value is paid back to the holder of the bond. However, some bonds can have indefinite lives and many companies allow themselves the right to purchase the bond back before the maturity date.

Bonds that are listed on the ASX can then be on-sold/traded by their owners at whatever price the market sets in the secondary market (the primary market is made up of the IPOs). This can create opportunities for the patient investor, as bonds may sell below the $100 face value, which means their running yield – the coupon divided by the market price – increases.

For example, if a bond with an 8% coupon trades at $80 after the IPO, then the yield jumps from an 8% coupon rate ($8/$100) to a %10 running yield ($8/$80). The bond may trade below its face value because the market believes the risk of the company defaulting has increased. Reasons for this may include a change in the company’s fundamentals or even macro-economic changes that may adversely impact future company earnings. When bond yields become very high, they are called “junk bonds” due to the elevated risk of the company defaulting. However, junk bond status doesn’t guarantee a company will default, so junk bonds can prove to be quite lucrative investments.

Now, if you’re mouth has been watering at the prospect of a guaranteed income stream for your portfolio, then I’ve got some bad news – the Australian secondary bond market is tiny. In fact, I can only find 5 vanilla bonds and 14 floating rate notes. That’s woeful. The US corporate bond market is far larger and contains bonds from low-yield blue chips all the way to risky, high-yield junk bonds. People have been calling for the development of the Aussie bond market, but right now the fixed income investor has very slim pickings on the local scene.

Government Bonds

When they aren’t running surpluses by taxing us to death, governments typically finance themselves by selling government bonds. Much like their corporate bond cousins, government bonds pay a fixed or floating coupon on the face value of the bond (typically $100). Governments also issue Capital-Indexed bonds which adjust the face value in line with inflation. This means both the face value at redemption/maturity increases, as well as the absolute value of the coupon (because it is based on the inflation-adjusted face value).

Once again, local bond investors will be miffed to hear that Australia has a very small government bond market too due to our relatively small level of government debt. In addition, government bonds are not quoted on an exchange. This means retails investors have to buy bonds in person at RBA offices (Sydney or Canberra) or by sending in an application form along with a cheque. This antiquated set up also applies for selling bonds – the investor sends in their forms and the RBA will buy them back at the prevailing market rate. I imagine that’s what investing was like in the 50s – although they at least had brokers with telephones back then. Personally I can’t believe this is the way we buy and sell government bonds in a modern, first world economy. But there you have it.

As a retail investor you can purchase as little as $1,000 in government bonds, up to a maximum of $250,000 (I presume after that you’ve become an institutional investor). For more information, check out this website.

Hybrids

The term hybrid is given to a class of securities that have the characteristics of both an interest-bearing security and equity i.e. both bonds and shares. Hybrid securities typically pay a fixed or floating coupon or dividend – in which case it may also have franking credits attached to the dividend. At a set date, hybrids will convert into equity (shares) or may be rolled over into a renewed hybrid security. These are often referred to as “Convertibles” and “Convertible Notes”, with a recent example being AFIC’s $300 million convertible note, offering 6.25% for 5 years.

“Preference Shares” also fall under the hybrid category. These are actually equity instruments (shares) that typically pay a fixed dividend, so they also have franking credits attached. They are called preference shares because they rank ahead of ordinary shares in terms of debtors obligations – so if the company goes bust, you are 2nd last in line to get your moolah back. All other debt holders get first dibs, with only the ordinary shareholders ranking lower. Think of preference shares as equity with a known dividend – great for security, but you won’t share in future dividend increases that are paid to ordinary shareholders.

Once again, I can only spot 48 hybrid securities on the ASX website, so secondary market retail investors don’t have a big spread to pick from.

Summary

So there you have it – a brief intro on the (Australian) fixed-interest options available to retail investors. In the future we’ll be reviewing individual fixed interest securities on a more regular basis, examining their details and what sort of return they can offer for the typical retail investor. If there’s any particular fixed-income security the MB community would like covered, shout them out.

Post-Script: the ASX interest rate securities lists can be found here on the ASX wensite.

Disclosure: The author is a Director of a private investment company (Empire Investing Pty Ltd), which has currently has an interest in one of the businesses mentioned in this article. The author also has a personal interest in the business mentioned in this article. The article is not to be taken as investment advice and the views expressed are opinions only. Readers should seek advice from someone who claims to be qualified before considering allocating capital in any investment.