As the Great Moderation passes by and the Great Volatility takes its place, the investing world is glacially facing up to the fact that a return OF your money is just as important as a return ON your money. The past 30 years have allowed all and sundry to “fuggedaboutit” or “she’ll be right mate” when it comes to investing, as even the laziest stock pickers were rewarded, although many mistakenly viewed this as skilful, not luck. At MacroBusiness we focus on the risk as well as the reward, and are not blind sided by the historical anomaly that has now finished.

Today I want to talk about 3 key risks about the return OF your superannuation, outside of the tremendous underperformance or the return ON super.

Liquidity Mismatch

A recent news article highlighted one of the 3 major “return OF” risks with super: liquidity mismatch, driven by the demographic bulge that is the Baby Boomers who are nearing or in retirement phase. The report highlighted the risks, well known by the industry, that negative cashflows from pension drawdowns could have systemic risks within the funds themselves, some of whom are heavily invested in illiquid assets and have low cash allocations.

This could lead to, at best, delayed super payments, or at worst, runs on funds, causing immense stress on superannuants. The industry was quick to allay such fears by publishing and spreading a research note that countered these assertions.

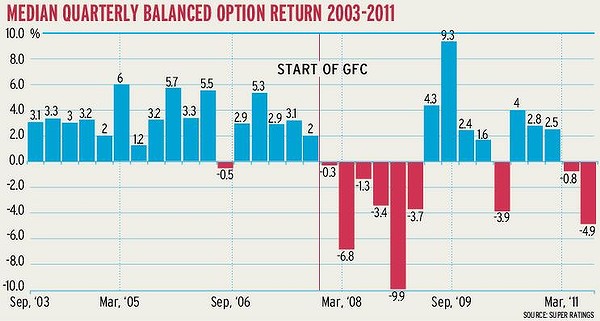

Notably, most pension drawdowns are monthly income streams, not lump sums, which should make this liquidity risk easier to manage. However, the systemic risk is by the industry focusing more on liquid asset allocation, instead of potentially more advantageous (both from an investor’s and macroeconomic point of view) illquid asset allocation, this could drive fund returns even lower, and/or increase volatility, which hasn’t been the industry strong point:

A further risk, exarcebated by a repeat GFC style event, is a fund freezing or reducing withdrawals as this implies a realisation of losses, which will affect other (i.e younger) fund member’s returns. One solution bandied about is to effectively turn larger funds into Ponzi schemes:

A fund with an ageing membership or with an uncomfortable level of exposure to illiquid assets could merge with a fund with a youthful membership or one with high levels of liquid assets.

Perhaps Ponzi is a stretch, as the more longer term solution, recommended after this comment, is to realign fund investment and product strategies with a return to annuity style products (this has been the strategy adopted by Challenger, pushed by the former chair of the Cooper review), which should never have gone away in the first place in the last 30 years and have potential outside super as well.

But should you rely on an industry to self regulate and promulgate such risk mitigation strategies, when their collective record of management and prudence when times are tough is less than exemplar? Perhaps the members are “doing it for themselves” as a recent Australian Investor’s Assocation surveyshowed that the average investment portfolio (including non-super) now had a 26% cash level, up from 21% in July.

Frozen and defaulted investments

The introduction of a deposit guarantee by the Federal Government during the GFC to prevent a run on illiquid mortgage funds (who would have needed to sell their assets at firesale prices to redeem funds) led to a widespread “freeze” with some investors still struggling to see their money returned, 3 years on. Not only struggling retirees – some of whom had concentrated a majority of their super into the once high yielding mortgage funds – but the sector itself is still battling, with ASIC running a “hardship” program pushing the funds to slowly return the frozen accounts.

The collapse of Trio Capital – not out of the blue or unusual particularly for a property based fund – was a wakeup call for the non-APRA regulated super funds who were denied compensation.

Who are they? Self-Managed Super or DIY Funds (SMSF). Currently, only APRA regulated funds (industry and retail super) can be compensated for bad investments, whereas the DIY crowd are on their own – literally – when it comes to these investment mistakes. Considering the rising popularity of SMSF (now more than a third of the whole super sector) this has a significant ramification, outside of the usual caveats about diversification and due diligence.

There have been some calls that the SMSF “community” should be regulated at a higher standard, including the trustees themselves. Given Australian’s penchant for requiring every aspect of life to have a “Ticket to Operate” attached, this has morphed into a possible requirement for trustees of SMSF to have, at least, finance Diploma level education and possibly more frequent auditing and a restriction of their investment universe.

This would “bring them into line” with the onerous requirements attached to the industry and retail super funds – you know, the ones that charge percentage based fees (and thus are constantly looking for ways to grow funds, and I don’t mean by performance) and provide around a 3% annualised return (before inflation) on your super.

So there is a minor risk that SMSF trustees in the future could find themselves “unqualified” and this could potentially mean a temporary or permanent loss of control through a compulsory allocation to the Federal Government’s new plan to tackle the fund management industry’s tentacular grip on super – MySuper, which leads me to the final identified risk.

Whose Super?

Puttings aside the tin foil hats for a moment – but not completely out of reach – the intent behind MySuper is a good one. First an explanation – what is MySuper (from the government fact sheet):

MySuper is a new low-cost and simple superannuation product that replaces existing default funds.

…funds will still be able to offer different products, and will not have to offer a MySuper product.

However, only a MySuper product will be eligible to operate as a default product. Which means a fund’s default product must meet the MySuper standards to continue to accept contributions from employees who have not exercised choice and nominated a fund.

- – no entry fees, with exit fees limited to cost recovery

- – a ban on hidden fees and commission in relation to retail products distributions and advice by financial advisers

- – removal of commissions in relation to Group insurance

- – a single investment strategy set by the trustee

Note that currently, MySuper is not compulsory, but by default (sic) it will be, as the vast majority of Australian’s don’t bother to change or select an investment option for their super. The savings for members (and the loss of income to the industry) is expected to be $550 million a year, growing to well over $1 billion. Whilst I agree with the rationale behind the new scheme, it has longer term implications and risks.

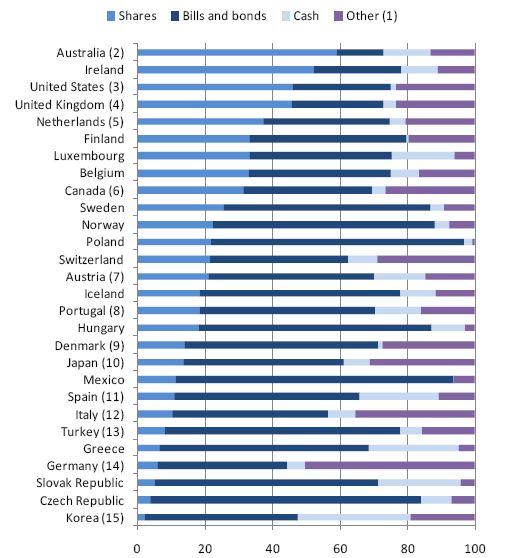

First, it still does not address the serious asset allocation problem of the standard default fund for the individual investor (i.e too much in shares, not enough in fixed interest). This is compounded by the structural concentration of retirement savings, as shown by the most recent OECD study, which shows Australian pension fund (i.e super) investments the most heavily concentrated in the world:

It is my contention that this concentration has lead to the serious underperformance of Australian super funds and will enable future governments to regulate MySuper at the investment level. That is, there is a great possibility that governments, working in the best interest of savers, will enforce a stricter asset allocation/investment strategy protocol on the MySuper accounts.

This could, in an extreme scenario, albeit done again with best intentions, lead governments to compulsorily acquire MySuper accounts and have them run viz. like State and Federal public pension schemes (e.g QSuper, Military Super etc).

This scenario is valid, particularly in a second GFC style event where a large amount of Baby Boomer retirement savings is wiped out (again) alongside the sparse and shallow savings of following generations.

Combined with the liquidity mismatch problem, another decade of sub-inflation returns by the entire industry, and the high probability that 2 generations of mortgage laden Gen Y and Gen X member cannot increase their contritbutions, could result, like in so many instances around the developed world, in a pension crisis. And from a crisis come the seeds of large and widespread solutions, including complete confiscation of private super accounts.

This could be construed as alarmist, I agree, and goes against the mainstream and longheld view that regardless of party, economic and fiscal management at the Federal level has been and will continue to be sound. Not having a recession for over 20 years will reinforce this notion, as does the concept of very low government debt, especially in comparison with the “badly run” developed nations now facing rolling debt and public spending crises.

I am not suggesting complete confiscation, but rather “voluntary” incremental steps. For example, in Hungary, the goverment recently “offered” the private retirement savers the option of either remitting these savings to the State or lose the right to the old age pension, and still have the obligation to contribute to it.

Poland recently came up with a variation on this scheme, whereby one third of future contributions (the equivalent of Australian Super Guarantee contributions paid by the employer) would be transferred into the State public pension scheme. However a more relevant example for Australians is the Ireland case.

Suffering from onerous repayment requirements from European banks in the midst of a property bubble crisis, the Irish government effectively had to give up its equivalent of the Future Fund (actually more so – the National Pensions Reserve Fund is supposed to fund ALL pensions, not just public service) to fund its bailout package.

Another “confiscation” risk is the ever increasing preservation and pension access age. This has increased in recent years, for superannuation, from 55 to 60 (for anyone born after 1 July 1964) and 67 for the old age pension (for anyone born after 1 Jan 1957). Both measures could increase further, as European nations facing austerity measures have recently used this tactic to cut public spending costs. In addition, this could involve an increase in tax rate in super, or elimination of contribution thresholds (thus increasing tax revenue).

Given that Australian private savings amount to some $1 trillion or almost 100% of GDP, the incremental measures above, tied to MySuper and other measures, are not out of the realms of possibility.

Risk Mitigiation

Obviously, diversifying assets amongst several different fund types, or outright exclusion of investing in illiquid funds (even if the yield seems tempting) goes a long way to avoiding risk of a frozen or defaulting fund. However, this does reduce your universe of investment products and in Australia particularly, there is only a small selection of super-suitable investments, due to our continued and unplaced devotion to equities.

The best way to mitigate against transactional liquidity is to control your own fund. This, for mind, is the greatest attribute of the Self Managed Super Fund (SMSF). Although the flipside of total control is total responsibility, and an almost part time requirement in terms of management and administration, there is no greater (apart from having off shore accounts) method of controling your precious retirement savings.

As for the final “tin-foil” hat risk, there’s not much (legal) chance of avoiding these risks (even if you emigrate to another country, your super remains in Australia until preservation age).

I contend the following:

1. If you are not approaching retirement age (i.e are Gen X or Gen Y), regardless of the generous (although they seem to be less generous each passing year) tax advantages of superannuation, I would not add any amount remaining of your disposable income to super. Let your employer contribute (as they are required to) and realign your asset allocation, but that’s it.

The risks are too high in putting all your savings into this basket, just as they are too high in putting the majority of your income into servicing a single dwelling. Accumulate wealth outside super where you can control it, direct it and use it.

2. A SMSF is the best way for you to get not only the best return OF your super, but managed correctly – and by not following the financial industry failed paradigms – also the best return ON your super.

For those interested in securing their retirement, regardless of age, their is no better solution – or would rather have the government or the fund management industry look after that for you?