Tomorrow is the open date for Woolworth’s latest round of corporate bonds, called Notes II (Notes I having been redeemed in September of this year). It’s not often we see corporate bonds being offered to the retail investing masses (Australian’s tend to have a love for equities over bonds) so I thought I’d give a quick summary of the prospectus for Notes II, as well as the potential impact for equities investors.

Woolworths Notes II Summary

- Issue price $100

- Issue date 24 Nov, 2011

- Interest payments will be equal to the 90-day bank bill rate plus a margin

- Margin to be determined by book build, but will be in the order or 3.25% to 3.5%

- Maturity of 25 years (Nov 24, 2036)

- Woolworths can redeem the notes from 25 Nov 2016 ( the “step-up date”) and onwards,

- If notes are not redeemed by the step-up date, the margin increases by 1%

- Payments quarterly, in arrears, on 24 Feb, May, Aug and Nov of each year

- First payment scheduled for 24 February 2012

- WOW may defer payment at its discretion, but all deferred payments must be made within 5 years. It cannot pay dividends, distributions or make capital returns on equal-ranking obligations whilst notes payments are deferred

- The notes will rank ahead of ordinary shares and preference shares

- Minimum $5,000 initial purchase, with increases in $1000 lots

- The notes will trade on the ASX under the code WOWHC

For a bit of historical perspective, below is a graph of the 90-day bank bill swap rate.

The bill rate currently sits at 4.72%, which means the yield on the Woolworths Note II if held today would be between 8.9% and 8.24%.

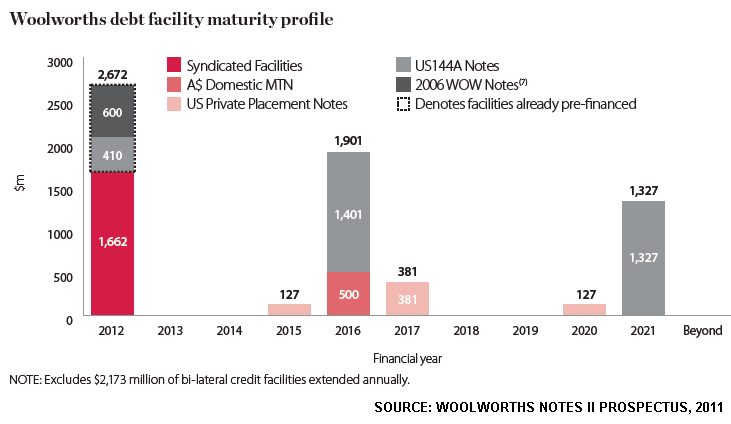

The prospectus states the aim of the Debt raising is for “general corporate purposes” and forms part of the company’s ongoing “general capital management strategy”. Woolworths previous Notes issue matured in 2011 whilst the company also has some large debt facilities maturing in 2012 (see graph below from the prospectus).

Impact on WOW Equties

For equity investors, the increase in leverage is a little concerning given that Woolworths also embarked on a share buy-back last year. From a purely mathematical point of view, using debt whilst also buying back share is a positive investment if your return on equity is higher than your interest costs – which is the case for WOW, which has an ROE of around 30%. However, increased debt means increased risk on your balance sheet.

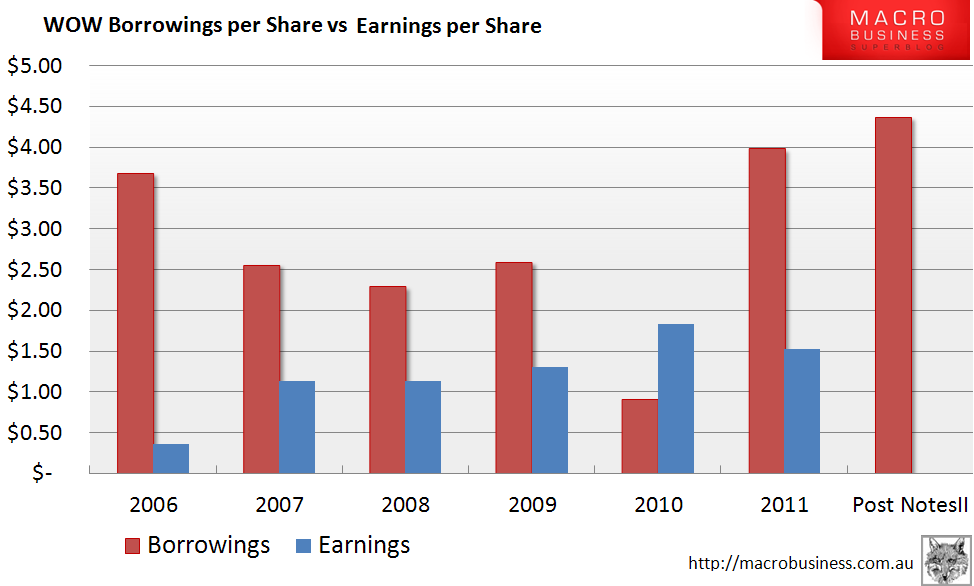

Woolworth’s total debt will increase from $4.85b to $5.33b after the issue of Notes II – a 10% increase. The graph below shows WOW’s total borrowings vs earnings per share over the last several years.

Despite the increase in leverage compared to earnings, some 80% of WOW’s earnings come from Australian food and liquor, which are typically non-discretionary, stable sources of profit. So Woolworth’s should easily shoulder the increased debt load.

None the less, we will be watching the leverage levels of WOW into the future and hoping to see the increasing debt trend arrested as profit increases.

Disclosure: The author is a Director of a private investment company (Empire Investing Pty Ltd), which has currently has an interest in the businesses mentioned in this article. The author also has a personal interest in the business mentioned in this article. The article is not to be taken as investment advice and the views expressed are opinions only. Readers should seek advice from someone who claims to be qualified before considering allocating capital in any investment.