At MB, one our key reasons for being is to expose ‘the spruik’ wherever we find it. Many of the bloggers at the site have very successfully done so for the perma-bullish housing brigade that used to dominate the national media.

No doubt readers have noticed the insistent call to “buy” shares over the past week coming from commentators in all quarters of the national media. I could have chosen any number of articles to expose this poor investment thinking, but one article using the motto of “buy when others are fearful” nicely highlighted three common mainstream misconceptions of equity markets and their role in your portfolio.

The first is a lack of understanding of how secondary asset markets work. The second is why asset allocation matters as much as simplistic stock picking. The third is the common lack of consideration of downside risk, either through opportunity cost or the consideration that stock markets can continue to fall and stay down, sometimes for a decade or more.

The article asked:

What’s driving the sell-off?

Standard caveat: Who knows? Markets do crazy things. More than 60 per cent of total volume is done by high-frequency computer trading using brainless algorithms. The past two weeks have understandably shaken confidence. Fearful of GFC2, investors have been fleeing the market. Broker TDAmeritrade said it processed more than 900,000 trades last Monday, with four out of five days last week hitting record levels of trading activity. Many were buying. But if the market is any guide, plenty were panicking.

Well actually half were buying, half were selling – that’s how markets complete a transaction. But the buyers wanted lower prices to take on the higher risk. But to get to the key word: confidence.

Just like the property bulls tend to confuse investment with speculation, equity and other risk markets are not places to efficiently allocate capital: they are for speculation on asset prices, driven by sentiment and confidence.

And this works both ways – for prices to rise, investors must be confident that future market prices are likely to be higher. When does this shift happen? No one knows – and for Japanese investors they are still waiting for this confidence to return, 20 years later, whilst American and European investors have waited for 10 years.

Back to the article, we then find an example of our second violated investment principle, that asset allocation matters:

Over in the US, the earnings yield on 10-year Treasuries is the equivalent of 50 times earnings. By contrast, Apple, possibly the fastest growing mega-cap company ever, trades at 11 times earnings. Which investment would you prefer?

I’d prefer the one where I get a return of my money, not just on my money. What if Apple trades at 9 times earnings (the average during a US bear market), and those earnings are 20% less because of tapped out consumers or higher taxes?

The article goes on to state:

Many Australian banks are still offering one-year term deposits at well over 6 per cent. If it’s the safety of cash you’re after, and with markets betting Australian interest rates are heading sharply lower, 6 per cent is a mighty fine deal.

You cannot compare different asset classes and value one as “better” than the other based solely on an earnings multiple (or lack of earnings). This is a misconception shared with physical gold, which has no yield, and thus is considered “worthless” by conventional asset allocation theory. In the same vein, negative real yield US T-notes (CPI in the USA is above 3%, so the yield is -1%) are also considered worthless or nearly so using this paradigm, which explains this from the article:

If you’re one of those willing to lend money to the US government for a decade at 2 per cent, we need to talk. Even a renowned dividend miser like BHP Billiton is yielding more than 2 per cent.

Again, this misunderstands the real role of money – exemplified by the run to gold experienced now, in almost every currency. This is not an investment or a willingness to get a return on your money (although many are speculating in the non-physical markets), it is to ensure, as best as possible, the return of your money and displays of a lack of confidence in risk markets.

And that brings us to our third ignored principle. What we really need to talk about is the downside – risk management, or the consideration that you may not get a return of your money, either through time decay, opportunity cost or outright physical loss.

The examples used in the article, Apple (AAPL), BHP, QBE and Woolworths are considered either blue chip and/or growth “stories”. Yet each face risks that will impact either their earnings and the multiple (and hence the real valuation, the price a buyer is willing to pay and a seller is willing to dispose at) applied to those earnings.

As I said during my piece (co-written with Q Continuum) on the Great Volalitility:

Price Earnings (P/E) ratios are not a valuation technique in of themselves, but a gauge of what the market is usually willing to pay for the earnings of a company (invert the ratio and you have the earnings yield to compare to a savings interest rate or bond yield)

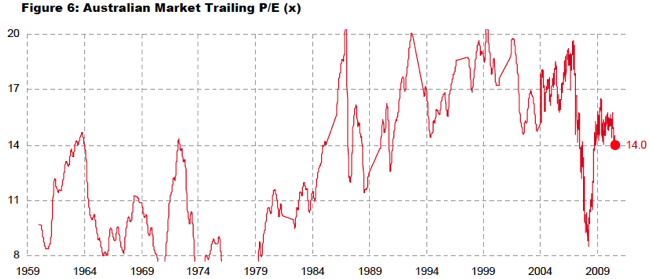

The last 20 years have seen the US market average a PE ratio of 25, whilst the Australian market over the same time period averaged 17-18x.

What causes these PE ratios to drop? Why are investor’s less willing to pay for the same amount of earnings as before? The answer is a mixture of sentiment, unclear inflation expectations and of course, a removal of exuberance – i.e. money creation.

From Wilson HTM

During the last sideways market (1969 to 1982), P/E ratios ranged between 8 and 14 – not the recent aberration of 17-18 times. Where is consumer sentiment (i.e the actual force that determines if businesses can create the “e” in earnings) heading? Where is the money creation – margin lending is disleveraging, the house ATM is turned off, governments are loath to stimulate and central banks “printing” is sitting in excess reserves that won’t be lent out.

Investors who don’t understand market dynamics need to understand history first, and not ideology. Markets “move” sideways as often as they go up or down. Sometimes these secular trends last a decade or more. The brave who hold on during these periods – even if they purchase the bluest of chips and receive a nominal dividend, run the second risk of this yield eaten up by inflation or a reduced payout ratio. Which is why the real focus needs to be on the underlying business robustness, as Q Continuum explains here not on a notional consideration of “cheapness”.

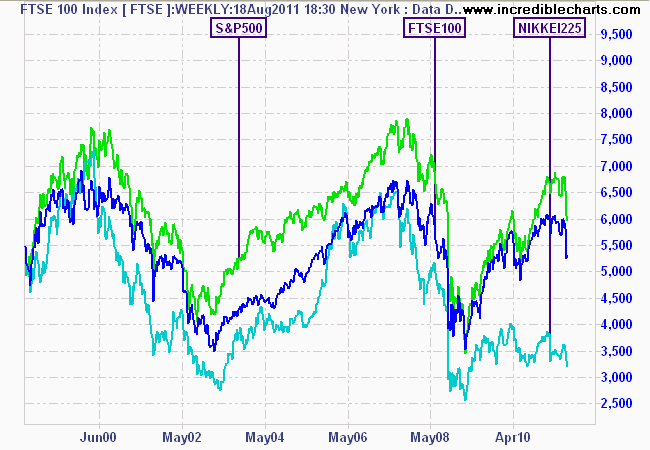

All major western equity markets in the last decade have not appreciated – the current “panic” is just another reversion along a decade long bear market. To repeat, the US, Japanese, UK, German and Italian stock indices have not yet recovered their 2000 highs. A similar fate is likely to have befallen Aussie equity markets if it weren’t for the rise of China (particularly there inclusion in the WTO)

The time to buy is not when others are fearful of missing out on a bounce, which is effectively what the falling knife brigade are hoping for, but when they are despondent that nothing will make them go back up again.