Throughout Friday, the azure blue sky above Brisbane was marred by the criss-cross pattern of contrails, as investors panicked and took the first flights to safety they could find. Gold was a popular holiday spot, whilst Equityville and Commodity City were deserted come close of business.

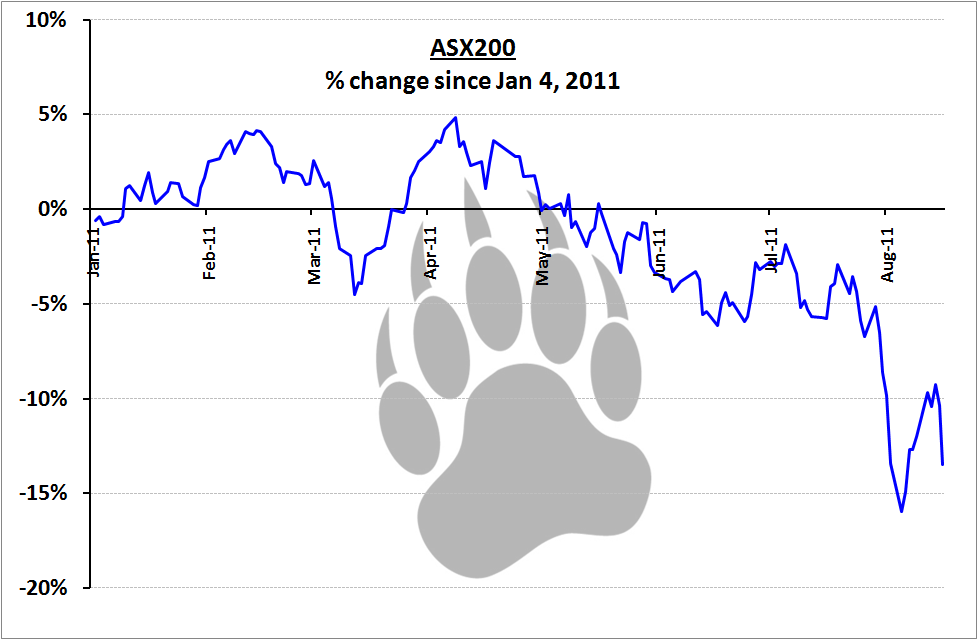

And really, who can blame them? This graph shows the % change in the ASX200 since the start of the year.

Not inspiring stuff for any buy and hold investor (although a welcome sight for traders and cashed-up value investors). Given the US and EU are in a competition for political ineptitude, most people (your blogger included) believe things will only get worse before they get better on the sovereign debt front .

At times like this, those still brave enough to invest in equities often start looking for stocks with high dividend yields. These should become more numerous as stock prices continue to drop, however there’s a couple of traps in this strategy:

- The price drops that create the high dividend yields often happen for a reason (I bet ABC Learning had a decent dividend yield towards to end).

- Yeilds are typically quoted “backwards” looking – i.e. they based on the last full year dividends, at best on the next lot of forecasted dividends. Companies will (and often should) cut dividends when times get tough and earnings drop, so that high dividend yield may disappear come the next reporting season.

- A high yield doesn’t mean continued good returns – if the company’s return on equity (ROE) is below your required return as an investor, then in the long run it will provide a below-par return on your invested capital.

The following are three examples of dividend-yield traps (yield as of 19/8/11, including all dividends paid but not including franking credits)

Lemarne Corporation (LMC), yield 35%: LMC owns a single electronics manufacturing business in Malaysia. Although now debt-free, its ROE has dropped from above 30% to 12% over the last 5 years and it no longer franks any dividends. Having a single operation in Malaysia also exposes it to the MYR/AUD forex movements – not exactly an electrifying investment.

Vision Group (VGH), dividend yield 55%: VGH one of the largest providers of private ophthalmic services in Australia. It is also heavily indebted, recently closed practices in Rockhampton, Hervey Bay and Bundaberg and posted a loss last year equivalent to 40% of equity. A dividend yield stock for the short-sighted.

Infigen Energy (IFN), dividend yield 44%: IFN develops, maintains and manages wind energy assets in America, Europe and the Asia Pacific. Another heavily indebted company that has posted losses for three of the past 5 years, with positive years producing paltry ROEs of 1.7% and 2.7%. Also at risk of Don Quixote puns.

Avoiding the Traps

The best way to avoid the traps is to apply a few fundamental investing filters. I’d look for companies with:

- A consistent (or increasing) ROE that’s above my required return (15%)

- Manageable debt

- No recent, major setbacks (and subsequent price drops)

- Not in a sector facing serious challenges (e.g. retail)

- Not dependent upon commodity prices

Using these criteria, I’ve chosen 5 high-yield (+7%) stocks that the dividend huggers might want to get cosy with.

Telstra – 9.0% yield, ROE 30%, net debt at 3 x NPAT

Telstra – the former government-owned come quasi-private monopoly telco – has been a perennial “Mum and Dad” stock and dividend-hugger staple for a decade. The Prince and I have railed against it as a dividend trap previously (see here and here), however the NBN has been a game changer. The current agreement will shower TLS with billions of dollars of cash for the next 30 years in exchange for their network assets. If they choose to distribute this cash stream to shareholders, then TLS will become a service-only telco with a nice annuity stream attached to it. The dividend-huggers delight.

Infomedia Ltd (IFN) – 11.7% yield, ROE 27%, no debt

IFM provides electronic parts catalogue and data management systems for the automobile industry. Infomedia has headquarters in Sydney and support centres in Australia, Europe, Japan, China, Latin America and North America.

I know very little about IFM (a contender for this week’s Equities Spotight maybe), however their raw numbers look good and they sell their systems to some 160 countries worldwide. They are exposed to forex movements due to their overseas operations; however this small-cap may be a decent dividend yielding stock.

Melbourne IT Ltd (MLB) – yield 9.1%, ROE 18%, net debt covered by 1.5 NPAT

MLB is an online solutions provider, focusing on professional consulting and corporate domain name management services to business. Despite exposure to forex movements, MLB services division still seems to be signing new business. Debt was reduced over the year, although intangibles were still very high (not unexpected for an internet-based business). Once again. A business with solid fundamental numbers.

Equity Trustees Limited (EQT) – yield 9.1%, ROE 15%, no debt

EQT is a financial services company that provides private client, trustee, estate administration and funds management services. First half FY11 revenues and NPAT were up and the latest guidance was for more improvement in the latter half. ROE has been solid for several years and the company has no debt.

Supply Network limited (SNL) – yield 12.1%, ROE 14%, net debt less than 1 x NPAT

SNL is the listed holding company of a group of related entities dealing in the importation, distribution and sale of after-market parts to the commercial vehicle industry. Their operations are spread throughout Australian and NZ. Revenues in both NZ and Australia increased last year – an impressive feat given the troubles both economies have been facing. ROE has been decent and debt levels are quite low.

Those that didn’t make the cut

To be honest, finding decent high-yield stocks was quite a challenge. Most of them had low ROE, high debt or were high yielding only because of a large price drop. There were also some well-known stocks that I discarded because of their sectors – Myers and David Jones in the retail sector and Mortgage Choice and Devine in property. For similar reasons, I didn’t include any of the big 4 banks because their traditional revenue well – ever-growing mortgage numbers – has run dry. Tabcorp and Tatts almost made the cut, but uncertainty surrounding recent demergers, government licensing and high debt saw them axed.

Is dividend hugging the best strategy?

Personally, I am not a fan of chasing dividends. For a value investor, dividends only tell part of the story. Capital growth (i.e. reinvestment of profits) is important as it can compound the size of future dividends. The split between reinvestment and dividend distributions is also important from a capital management perspective – high ROE companies with growth opportunities would be better retaining profits than distributing them and vice versa. And of course, as I always bang on about, ROE is the best indicator of a company’s performance.

Don’t get me wrong – dividends are important, but they will be accounted for in any decent intrinsic value calculation. If I can find a high-dividend stock with a consistent 20% ROE that distributes all its earnings, I’ll be first in line at the share registry. However, chasing a stock for its dividend yeild – without considering all the other financial elements of the company – can be fraught with danger. Choose the right stock and you’ll have a good annuity-like investment. Choose the wrong one, and you’ll end up with a sub-par investment.

Hugger beware.