The S&P/ASX200 has slid 12% in four weeks with similar falls across major developed markets as the Western crisis has gathered pace in the past month. Apart from the usual and vapid insistence to buy any and all stocks now because they are “cheap”, some commentators have said that ”buy and hold” is dead and we are now entering a trader’s market.

Well, if buy and hold means grabbing any ASX200 share, holding and hoping for a substantial capital gain, then yes, “buy and hold (and hope)” is dead. It was always dead. No matter how long you hold onto Qantas, Bluescope or Telstra you’ll get sub-par returns with their current business models, incompetent capital allocation and poor management . This will be even more evident in a future without the debt-fuelled asset price growth we’ve seen over the last 20 years.

As for the traders, every secondary asset market has always been a traders market – the good ones should be able to make money whether it’s raining bulls or bears. The pigs will still get slaughtered.

Nonetheless, the future of share investing will not be the same as the past. As we’ve covered at length here at MacroBusiness, Western risk markets have seen asset price growth fuelled by highly-leveraged, high-income baby boomers. Both of those drivers are now evoparating due to the GFC and inexorable demographic changes.

So what lies ahead? What should the intrepid equity investor be wary of as we sail upon uncharted waters, keeping a wary eye out for Chinese dragons and debt krakens?

Earnings multiples (P/E Ratios) will drop

Price Earnings (P/E) ratios are not a valuation technique in of themselves, but a gauge of what the market is usually willing to pay for the earnings of a company (invert the ratio and you have the earnings yield to compare to a savings interest rate or bond yield)

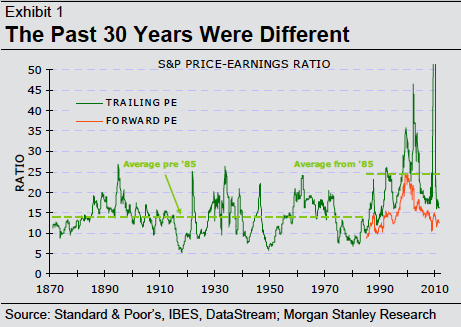

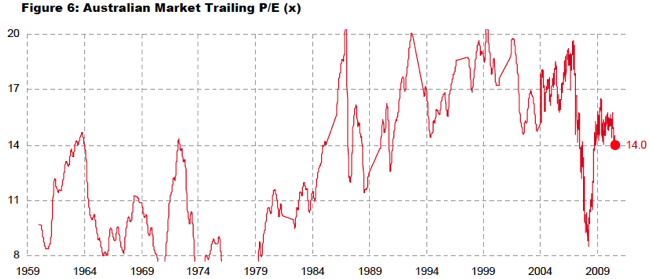

The last 20 years have seen the US market average a PE ratio of 25, whilst the Australian market over the same time period averaged 17-18x.

- From Wilson HTM

What causes these PE ratios to drop? Why are investor’s less willing to pay for the same amount of earnings as before? The answer is a mixture of sentiment, unclear inflation expectations and of course, a removal of exuberance – i.e. money creation.

The chart below shows the change in margin (funds borrowed to purchase stock) at the NYSE and the corresponding S&P500 Index. This is the true “cash on the sidelines” and when this meta-money disappears when investors lose confidence, or sell their holdings to fund retirement, volume drops, transactions become more volatile and the market corrects. The same dynamic is underway in property markets around the world.

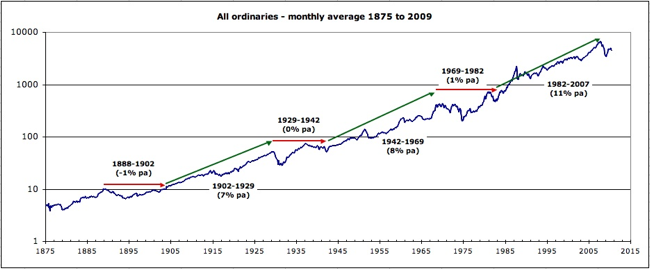

This is a reflection of the poor sentiment of investors by ranging, or trading sideways, sometimes for over a decade, as this chart of the All Ordinaries since 1875 (h/t Data Diary) shows:

- From Data Diary

Even during those sideways markets, share prices still went up and down, great companies were started and flourished, poor companies went to the wall, or became zombies and investors still made and lost money along the way.

However, the average P/E ratio drops, usually to 10-11 times in Australia and the long run average of 14 times in the US.

What is key is that the price people are prepared to pay (or not pay) still reflects the underlying value of the stock, and in sideways markets, this means a reduced P/E ratio. The last 30 years, as Gerard Minack has stated, was different.

Earnings growth potential will stagnate or fall

As alluded to above, earnings growth will no longer be fuelled by household debt. Only when disposable income and/or labour productivity increases will there be scope for more consumer spending at the macro level. At the company-level, the above-average performers with high-demand products will be able to grow earnings substantially – especially those exporting to growing markets (Cochlear as a prime example) or underpinned by non-discretionary government and household spending.

This “new normal” of reduced earnings growth will also be reflected in lower PE ratios as markets begin to accept (probably through a series of lower highs as market’s rally between earnings seasons) that the previous period was an aberration. Other factors that cloud this outlook are increased regulatory burdens and overshoot by government, reduced innovation and “entrepreneurial spirits” as management and lending institutions become more conservative, increased tax burdens and the likelihood of producer and consumer price inflation of commodity-based goods.

At Empire Investing we contend that the combination of lower earnings potential and structurally different sentiment, Australian and other debt-satured developed equity markets will be returning to an era of PEs between 10 and 15, with the majority of Australian industrial stocks averaging a PE ratio of 10 or less.

Non-discretionary is the new black

In the post-leverage era, those companies relying on expanding credit for earnings will not fare well. Indirectly this will impact retailers, but more directly it will affect the issuers of debt themselves – the banks. As we have highlighted in our research earlier this year, you should expect a return to high single-digit ROEs as the banks become the utility-like financial intermediaries they are supposed to be. High dividend yields will entice the average investor and speculator, as will the average super fund, which may cause bank share prices to trade at a premium from time to time. But volatility through increased hedging/shorting by institutions and successive data releases and the over-exposure of the banks to the index can have a disastrous effect on the capital value of any bank-laden portfolio.

If western consumers retreat further into their shells, China will be in trouble. An export-lead development model won’t work when no one buys your products. This will directly impact commodity prices and Australia’s much-vaunted mining boom. The likes of Rio, BHP, Fortesque and all the other miners are enjoying record high prices for their minerals and basing expansion plans on continued elevated prices. China falling over will kill share prices and halt or delay projects. In a double whammy, those projects now online that are nearing completion will add supply as prices come off their peaks. Our miners may be our saving grace at the moment, but commodity prices are fickle at best and unbelievably volatile at worst. Be prepared fro extreme volatility in resources shares.

Following on from these concerns, and moving away from the staid “Houses and Holes” investment strategy, we contend that the only companies worthy of producing stable, robust earnings and supported by fundamentals are those that cater to the non-discretionary household and government budgets.

This is not just a defensive “play”, but reality. The makers of fashionable “wants” and discretionary retail items will struggle to win over the cautious consumer. Further, industrial companies tied to property (including commercial) and construction will feel the pinch as economies retract to a normal (or below normal) growth phase. The ever-expanding internet can provide better opportunities but the track record of Australian corporate management in taking advantage in this area is dismal.

Meanwhile, the ageing baby boomer will allocate his/her shrinking retirement “pie” into ever-increasing healthcare costs, which will benefit those companies with strong management and customer focus. For the aged consumer, non-discretionary will include expensive health care products (e.g Blackmores) and services as demographics moves to include two entire generations extant, over the age of 65. The choice between a caravan and a cataract operation will reverberate through the economy as this massive block of citizens get older and poorer.

Although most energy companies deliver mediocre Return on Equity (ROE), most enjoy monopolistic franchises, an ability to raise prices at whim, and usually high dividend/distribution yields. Purchasing these companies at a discount to their equity per share value can provide the investor with an enhanced return. Renewable energy companies, once mature and developed and with carbon prices factored in can also be considered non-discretionary and robust in nature and may grow with demand.

Volatility will be the norm, not stability

A return to the old paradigm, that markets are actually risky and a balanced portfolio actually means less than half weighted in shares, does not necessarily mean a realisation by the majority that price volatility equals risk. This lack of observation will of course create more volatility.

Participants must get used to annual price volatility exceeding 20% (and occasionally 50% each way). During sideways markets, this will be the norm, not a stable bull market that inexorably rises 10% annually and usually comprise 1-3 dips, and maybe a single correction (up to 10%) a year.

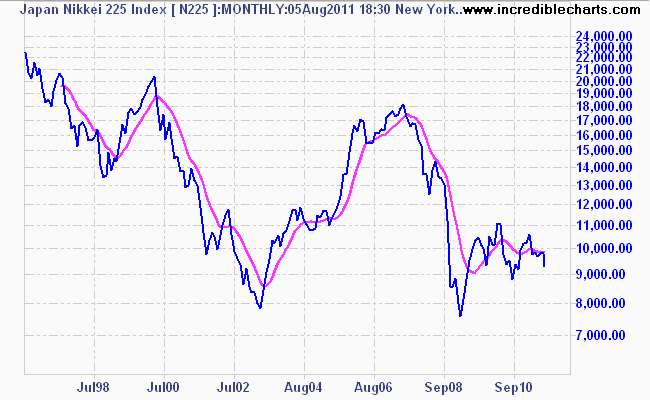

An interesting empirical observation of this type of volatility is the post-bubble Nikkei 225, the Japanese stock market. Whilst it has other factors that explain why it is still some 60% plus below its 1989 nominal high, it provides an idea of the volatility within a “sideways” market.

- Monthly chart of Nikkei 225 plus 260 day moving average

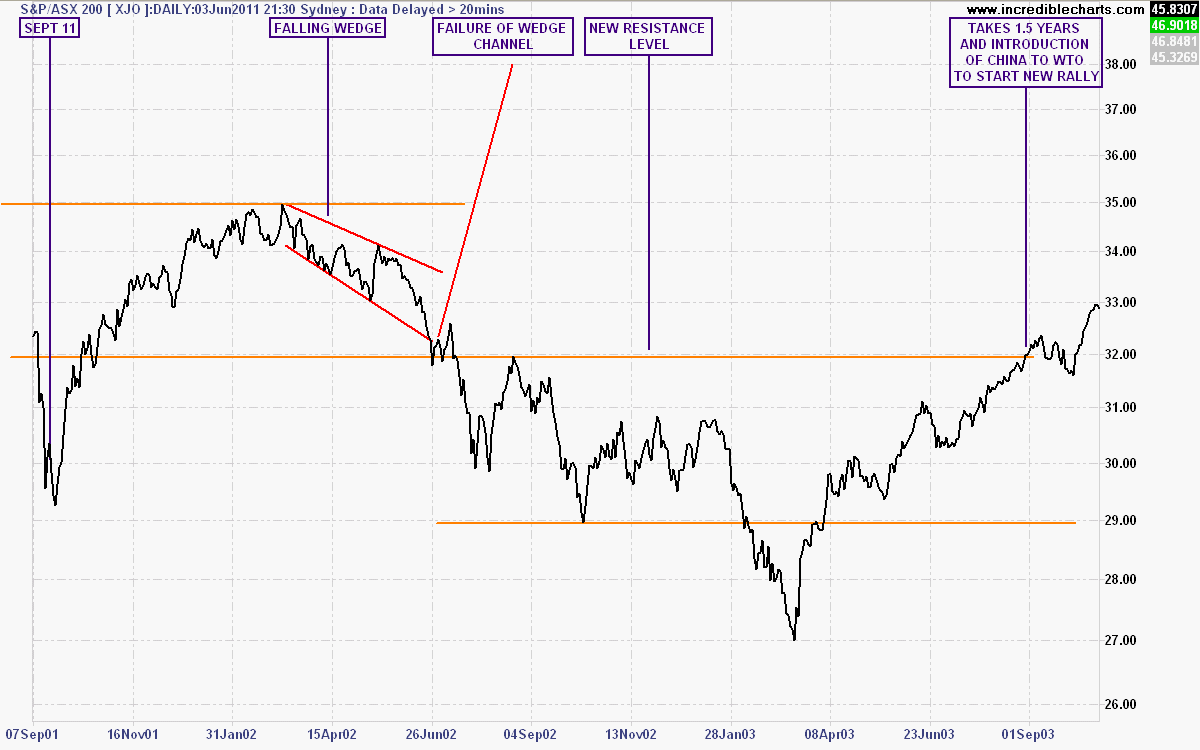

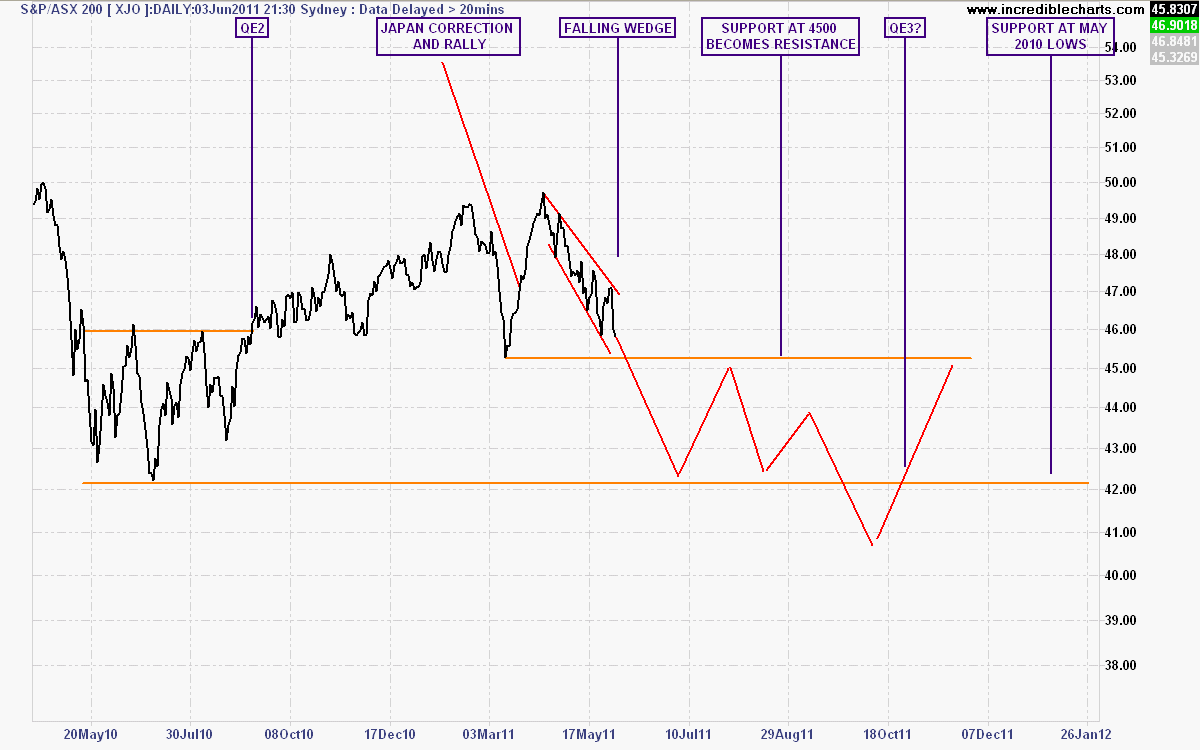

Another example is The Prince’s study of the 2001-2003 bear market, in “Tale of Two Charts”.

- ASX200 2001-2003 Bear Market

- The Prince’s study of the ASX200 from mid-May

This pattern, and a variation thereof – possibly including another round of stimulus from the US provoking a huge rally – is likely to be repeated going forward. What will not, however, is the medium term aberration that was the 2003-2007 rally, and the 1982 to 2007 secular bull market.

Given this premise – you need to choose your role – investor, trader or watcher. If you can’t stand this price volatility, stand aside. If you intend to invest, be prepared to sell on rallies (if no other investments exist that provide a good return) and buy on crashes – or hold for the long term with protection built in. Traders, continue the course and provide liquidity for all of us (except the HFT).

Long-term now means long-term

Since we’ve been involved in finance and the markets, most participants we’ve encountered consider two to five years as a long-term investing timeframe. It ain’t. In a future stagnating and sideways market, long term for the investor must mean beyond a five year holding period to iron out the inevitable volatility that will occur.

The investor should be prepared to see minimal or nil real (adjusted for inflation) market price growth during this period (although intra-year volatility is likely to be very high), even if the equity base and earnings appreciate in real terms.

Markets could take 2-5 years to return to pre-crash highs, or up to a decade, or within 12 months. No one really knows and unless you are prepared to ride out this volatility, stand aside, or consider a new way to allocate assets based on risk (more to follow from The Prince’s series on asset allocation and superannuation).

Fundamentals still matter, but sentiment will drive markets

It is worth remembering that contrary to considered opinion, markets lead and directly change the underlying fundamentals by way of sentiment. When $4.5 trillion in stock equity is wiped out over a week or so, investors change their spending and investing behaviour. This is reflected back in the markets as reduced earnings and a reluctance to buy risk. The real loss of faith in markets hasn’t changed the reality that secondary asset markets are still a place for capital speculation based on human behaviour.