As mentioned by Delusional Economics yesterday, the bastion of the Aussie punter, David Koch, has issued a warning that Australian home values are on the slide.

The question now is how far will prices fall and over what time period? SQM Research’s Louis Christopher recently issued a newsletter predicting falls of 5-10%, whereas many bank economists still expect prices to plateau.

For the sake of comparison, I thought I’d take readers through the housing corrections/crashes recently experienced by other developed countries, namely: New Zealand, the United Kingdom, the United States and Ireland.

Scenario 1: New Zealand slow melt

New Zealand’s housing correction has, to date, been relatively mild owing to its close linkages to China via Australia [Australia is New Zealand’s largest export market]. In nominal terms, New Zealand home prices fell by 9% peak-to-trough between September 2007 and December 2008. Prices have since recovered somewhat to be down 5% since their peak. However, in real (inflation-adjusted) terms, prices are down by 15% from their peak.

New Zealand home prices have shown little prospect of recovery as the economy slowly deleverages following a decade of credit-fuelled consumption. In the absence of another external shock, prices are likely to continue stagnating, declining in real terms as incomes catch-up.

Scenario 2: United Kingdom mini crash

The UK housing market experienced a mini crash over the period September 2007 until June 2009, whereby home prices fell by 21% in nominal terms peak-to-trough. Prices have since recovered slightly to be down 18% since the peak. In real terms, however, UK home prices have fallen 28% (see below chart).

Like New Zealand, the UK housing market is showing little signs of recovery, with the economy in a deleveraging funk compounded by the government imposing austerity measures on households. In the absence of another external shock, prices are likely to continue stagnating, declining in real terms as incomes catch-up.

Scenario 3: United States crash

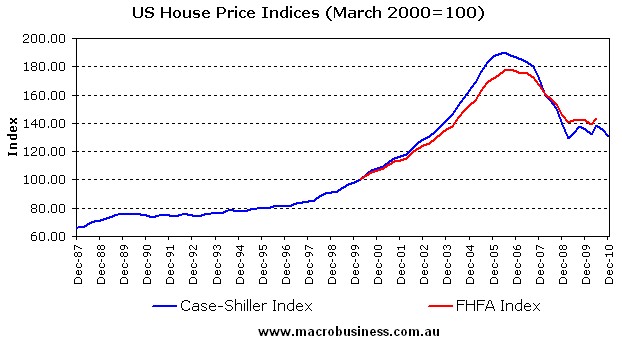

The US housing crash is interesting because there are two main indices commonly used to measure national home prices: the narrower 20-city Case-Shiller house price index and the broader 50-state FHFA national index. As explained previously, nominal home prices have been more volatile in the narrower Case-Shiller index because it comprises more housing markets where land/housing supply has been restricted (click to view comparison chart).

{kind=link}

I have chosen to use the Case-Shiller index in this case study since it more accurately corresponds with Australia’s restrictive urban planning system. According to the Case-Shiller index, US home prices have fallen 31% in nominal terms since their peak in June 2006. In real terms, however, home values are down a whopping 36% (see below chart).

The US housing market, too, is struggling to recover as it is marred by negative rates of household formation, a large stock of unsold homes, restrictive credit conditions, and household sector deleveraging (see here for details). As such, home prices are still falling and are likely to remain subdued for an extended period of time.

Scenario 4: Ireland crash

Like the US, Ireland has experienced a nasty housing crash, with nominal prices falling 37% peak-to-trough between September 2006 and December 2009. Home prices have since recovered somewhat to be down 28% in nominal terms and 29% in real terms (see below chart).

The Irish economy is cactus. Official unemployment is 15%, Irish citizens are in debt to the tune of 170,000 euros per head due to the government bailout of Ireland’s banks, the economy is surviving on hand-outs from the EU and emigration is at levels not seen for decades.

Combined with the Irish Government taking an axe to spending and increasing taxes, thereby further exacerbating the economic malaise, as well as the large stock of unsold homes, the Irish housing market will remain in poor shape for years to come.

What’s next for Australia?

If commodity prices can remain near record highs and international capital markets remain willing and able to fund our banks, then a New Zealand-style slow melt is probably on the cards for the Australian housing market.

If, however, the Chinese economy slows sharply, causing commodity prices to fall back to their long-run average, then a UK-style mini crash is likely.

A full-scale housing crash would probably require a hard landing in China and another GFC, causing: (i) a complete collapse of Australia’s terms-of-trade; (ii) a severe worsening of the Budget bottom-line; (iii) credit rationing and severe bank stress; and (iv) increased unemployment and a deep recession.

Which scenario (if any) do you think is most likely for Australia?

Cheers Leith