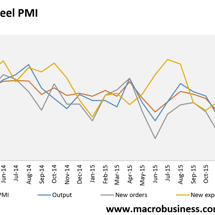

Another reason for the iron ore rally

From UBS: Tangshan’s International Horticultural Exhibition opens 29 April Tangshan, in Hebei province in China, opens its International Horticultural Exhibition from 29th April to 16th October – about 5½ months in total.