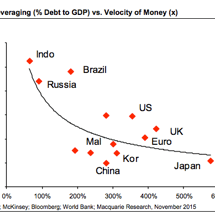

BRICS collapse on Goldman

From Bloomberg: The bank’s asset-management unit folded its money-losing BRIC fund, which invests in Brazil, Russia, India and China, and merged it last month with a broader emerging-market fund…Fourteen years after former Goldman Sachs economist Jim O’Neill coined the acronym that ushered in an unprecedented investment boom, the biggest emerging markets are now sputtering.