Categories

Global Macro

JPM wizard says gold and recession

Some of you will no doubt be familiar with JPM Gandalf A.K.A Marko Kolanovic, from Bloomberg: That’s what happened yesterday.

David Llewellyn-Smith

10 years ago

5

Mining GFC explodes as central banks lose control

David Llewellyn-Smith

10 years ago

50

William White on quantitative failure (now working)

David Llewellyn-Smith

10 years ago

18

Mining GFC smoulders

The Mining GFC smouldered overnight as the our Janet barely moved the needle.

David Llewellyn-Smith

10 years ago

10

Treasury head hoses ABS jobs numberwang

Treasury head John Fraser in the Senate this morning on global growth: “There is no clear path ahead…The volatility has been significant.

David Llewellyn-Smith

10 years ago

11

Mining GFC rages higher

The Mining GFC raged higher last night as the tension between falling commodities and the end of Fed tightening gave way to simple worries about global growth and commodity demand.

David Llewellyn-Smith

10 years ago

26

Japan leads on the path to quantitative failure

Japanese stocks are taking another flogging today with the Nikkei down -4.4%. More to the point they are now down -8-9% since the BOJ announced its new negative interest rate policy (NIRP) as a part of its ongoing attempt to inflate markets.

David Llewellyn-Smith

10 years ago

13

Mining GFC crisis deepens

The Mining GFC crisis deepened last night as rumoured US shale bankruptcies swept the market and stocks were pummeled -2.5% then rebounded some: Those low 1800s support levels on the S&P500 do not look strong.

David Llewellyn-Smith

10 years ago

15

BIS warns on Mining GFC

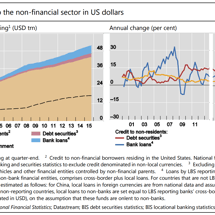

The only credible institution in world banking, and the only one that warned of the GFC, today warned on the Mining GFC: The growth of debt in the emerging economies has been dramatic, as shown in Graph 1.

David Llewellyn-Smith

10 years ago

4

Mining GFC roars back to life

After one day off it’s baaaack.

David Llewellyn-Smith

10 years ago

15

Wolf: Central banks better prepare for recession

From the FT’s always excellent Martin Wolf on what central banks need to think through for the next recession (which may not be far away): One would be to do nothing.

David Llewellyn-Smith

10 years ago

33

Is the Mining GFC at an end?

From our old friend Clifford Bennett: One could be forgiven for thinking thus.

David Llewellyn-Smith

10 years ago

18

Mining GFC crashes into quantitative failure

David Llewellyn-Smith

10 years ago

10

Are we on the verge of “quantitative failure”?

This post comes via Zero Hedge and is, for me, the key question for just how bad the Mining GFC is going to get.

David Llewellyn-Smith

10 years ago

30

Mining GFC erupts again

David Llewellyn-Smith

10 years ago

13

Mining GFC resumes

The Mining GFC sputtered into life last night.

David Llewellyn-Smith

10 years ago

WHO declares ZIKA emergency

From the World Health Organisation comes news the Americas hardly need.

David Llewellyn-Smith

10 years ago

15

Stocks rocket as Mining GFC gets worse

David Llewellyn-Smith

10 years ago

14

Mining GFC eases on oil surge

The Mining GFC took a well-earned break overnight as oil rumourtage doused some flames.

David Llewellyn-Smith

10 years ago

1

Mining GFC soverign defaults loom

From the FT: Officials from the International Monetary Fund and the World Bank are heading to Azerbaijan to discuss a possible $4bn emergency loan package in what risks becoming the first of a series of bailouts stemming from the tumbling oil price.

David Llewellyn-Smith

10 years ago

10

Fed balks at Mining GFC

From the FOMC comes a little acknowledgement that things are not going too well: Information received since the Federal Open Market Committee met in December suggests that labor market conditions improved further even as economic growth slowed late last year.

David Llewellyn-Smith

10 years ago

20

Mining GFC rages as Shanghai crashes

Finally someone else has worked out what’s at stake in the Mining GFC.

David Llewellyn-Smith

10 years ago

9

Summing up Davos 2016

By Alpha Beta Strategy and Economics DAVOS 2016 The mood in Davos this year was mixed.

Leith van Onselen

10 years ago

38

Mining GFC takes a break

Brent oil rocketed 10% on Friday night and the Pavlovian share market went with it: Alas the odds still favour this being another bear market rally, not a bottom.

David Llewellyn-Smith

10 years ago

Zombie ships herald the Mining GFC

I don’t regularly follow the Baltic Dry Index as a direct indicator of economic or market forecasts, but you cannot deny the current price action, as it reaches a record low.

Chris Becker

10 years ago

30

Newer Articles

Older Articles

Page

58

of

95

Newer Articles

Older Articles

Advertisement