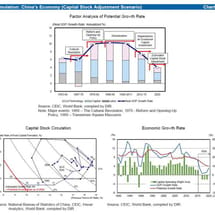

Measuring China’s Western property crash

From Andrew Collier of Orient Capital Research via BeyondBrics: Some of the excess construction in Sichuan’s rural areas can be laid at the feet of disgraced former Chongqing Party Secretary, Bo Xilai, who was removed from office under a cloud in 2012.