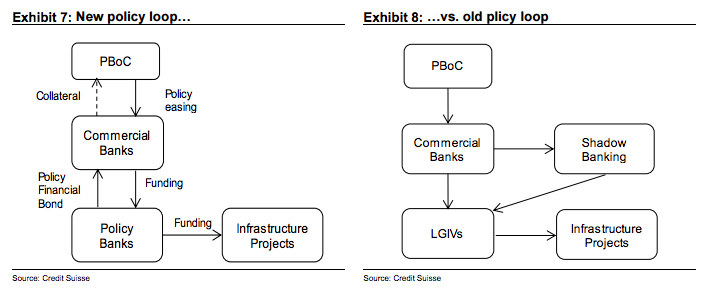

From Credit Suisse via FTAlphaville comes China’s new stimulus structure:

It looks to us that a new policy loop has been developed. The PBoC creates liquidity to commercial banks, through cutting the reserve ratio/interest rates and selective easing. Banks buy policy banks’ special bonds. Policy banks lend out to infrastructure projects that Beijing intends to promote.To some extent, the policy banks are doing what the local investment vehicles (LGIV) were under the Wen Jiabao administration. In the RMB4tn stimulus launched in 2009, the central bank eased monetary policies and banks lent to the local government investment vehicles, which are linked to the local governments, but have a separate balance sheet. The local government investment vehicles were largely responsible for the infrastructure investment during 2009–2012, lifting economic growth in the short run but also creating a local government debt legacy that threatens financial stability even now.

Compared to the LGIVs, the policy bank led stimulus has the following characteristics. 1) A more refrained investment style – it is estimated at RMB2–3tn in sum and concentrated in specific areas such as shanty town renovation, environmental protection projects; 2) mainly in equity investment instead of lending; 3) “no excess capacity and no crowding out effect”; 4) standardized lending, in the form of quasi sovereign bonds. The government does not guarantee the bonds, but the PBoC seems willing to take these bond as collateral in the future, if it wants to ease further

The move is clearly aimed at boosting growth, as the politburo has vowed to pay substantial attention to downward growth pressure and systematic risk.The specific policy financial bond scheme is another targeted easing measure to provide funding support to infrastructure projects and the agricultural sector, which should provide help for specific sectors in the real economy. The government has identified 22 areas of infrastructure and public goods, e.g., subsidized housing, gas, hydro, for which this project could provide funding to support. This project is significant, in our view, because it provides equity for new infrastructure investment. Banks usually require an equity base equivalent to 30% or more of the infrastructure investment before being willing to commit to any lending, but new infrastructure projects have trouble securing the equity base, as shadow banking (the primary fund source in the past) shrinks. Policy banks’ funds injection in equity form helps to address this hurdle.

To us, it seems evident that the leadership in Beijing is more willing to help boost growth prospects now, in contrast to talking about the “new norm” in growth this time a year ago. That said, the measures seem restrained. RMB2–3tn funding for the policy bank is material, but not excessive against the benchmark of the current RMB11.6tn in their balance sheet and RMB 340bn for monthly lending. This is not a repeat of the 2009 stimulus, but targeted easing to specific areas that potentially could help growth. Beijing does not seem interested in another outsized stimulus program that might deliver more harm to the economy than benefits in the long run. Still, with new infrastructure set, Beijing could scale up the stimulus, if it is deemed necessary in the future.

However, the overall impact for the economy would depend on the multiplier effect from the private sector. Unlike the last round in 2009, the private sector has demonstrated little interest in investment this time, despite Beijing’s efforts. Until Beijing can find a way to re-engage private investment, we suspect that the economy may not benefit as much, other than in areas directly boosted by government spending and lending.

It looks to me like more of the same. Targeted stimulus for glide slope management to lower and less commodity intensive growth. Good news for a moderately paced transition but no panacea for anything else.

As for the stock market, some estimates are flowing through on the extent of government spending, from Goldman also via FTAlphaville:

Advertisement

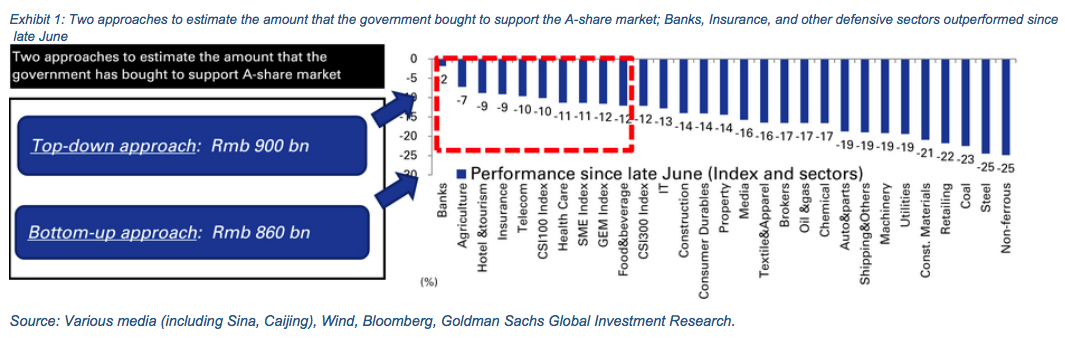

[China] has potentially spent Rmb860-900bn [some $144bn] to support the stock market in June-July 2015… equivalent to 1.6%/2.2% of total market cap/free float market cap:

…potential aggregate size of market-support funds is probably around Rmb2tn (including the money already spent), by our estimates, and we believe authorities including the PBOC are also likely to inject further liquidity if needed. This implies sufficient market-support funds to continue to provide a downside cushion to the equity market as the later stages of retail deleveraging unfold.”

HSBC sees similar:

The initial rally in the stock market was driven by cRMB1trn of debt-financed balance sheet expansion by domestic brokers, 80% of which has come from the issuance of broker bonds and commercial paper since 2013. Recent government efforts to stabilise the falling stock market through stock purchases came at the cost of another RMB1trn-plus of borrowing. Broker and OTC margin financing, and stock pledged lending could collectively add up to another RMB5trn of stock market related lending. All together, the amount of debt created as a result of the stock market boom has dwarfed the benefit in terms of additional equity financing, which has amounted to just cRMB400bn.

The amount of money borrowed by government-backed entities to calm the stock market in July alone has already surpassed the RMB434bn y-o-y increase in capital raised from equity issuance in 1H15.

Advertisement

Related and sadly, we are about to lose control of one of my favourite China indicators, from MNI via Zero Hedge:

The PBoC, MNI continues, will include loans made to CSF, China’s plunge protection vehicle, in the figures, meaning Beijing will pretend that the state-directed effort to artificially shore up the country’s stock market represents real, organic demand for credit.

As for the real situation, one loan officer at a Big Four bank told MNI that “our bank’s loans in July in the Beijing area were even weaker than in June. We can’t find the demand.”

But that’s ok because in the absence of government intervention, Chinese stocks “can’t find” a bid, which is why, as Bloomberg reported earlier today, CSF “seeks access to as much as CNY5 trillion to support the stock market if needed.”

China is increasingly running full tilt to stand still.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.