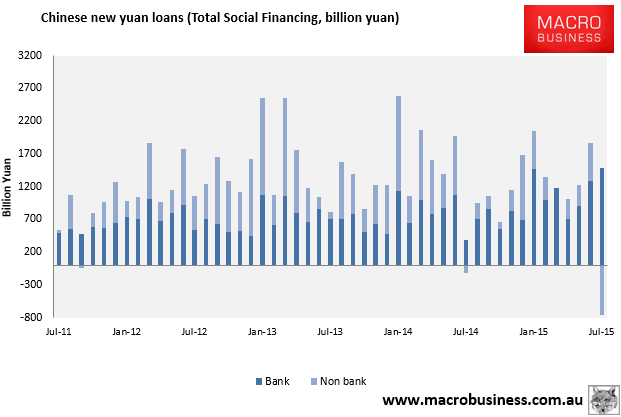

China has released absolutely crazy July credit data sending Australian equity markets equally bonkers. The headline numbers for new yuan loans in total social financing came in at a modest 718 billion yuan but bank lending went mad up 1.48 trillion and shadow bank lending crashed by 762 billion yuan:

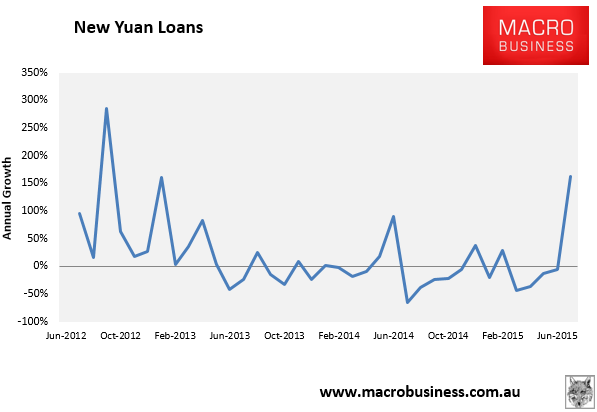

The net impact was still a big year on year surge because last July was a complete wipe out:

Advertisement

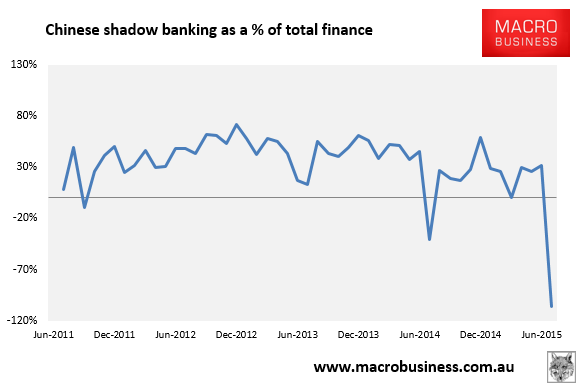

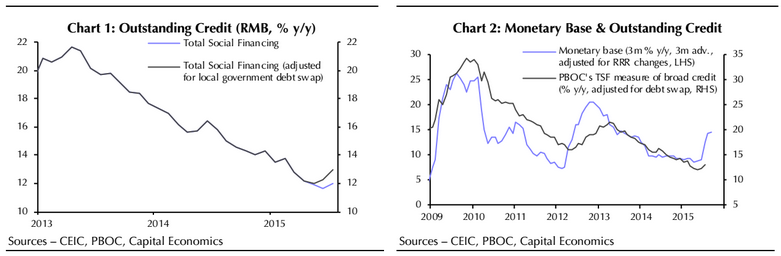

But look at shadow banking:

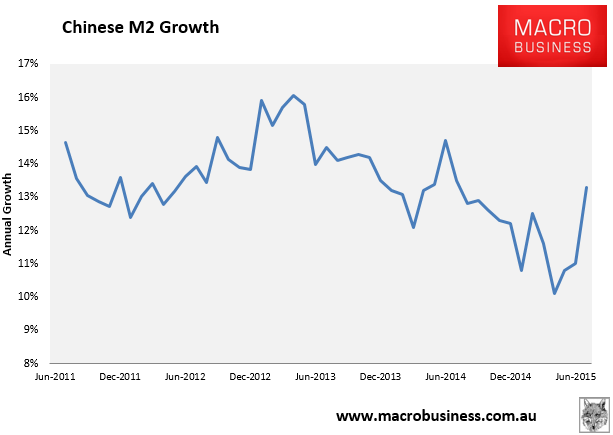

M2 growth took off to 13.3%:

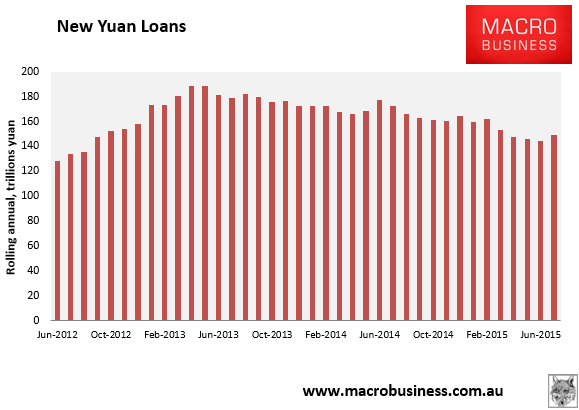

And the rolling annual enjoyed a bump:

Advertisement

But, as I noted recently, the PBOC is including in these figures the billions of yuan loaned to the “national team” in its efforts to stabilise the stock market. Media speculation has pointed at a figure somewhere between 500 billion and one trillion yuan for that, so that would render the entire bounce moot in terms of the real economy and could even hint at a rather large draw down.

However the shadow collapse is explained by the following:

Remember that, in recent month, local government financing vehicle debt which used to be captured in TSF in the form of bank loans and corporate bonds has started to be refinanced by municipal bond issuance which is not captured in the TSF measure.

So, once we adjust for the shadow bank shift and the “national team” lending we get a new yuan lending figure that shows a modest rebound, probably best illustrated in the rolling annual chart.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.