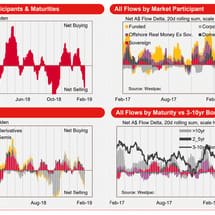

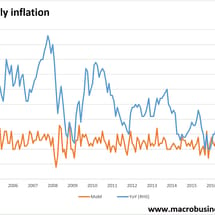

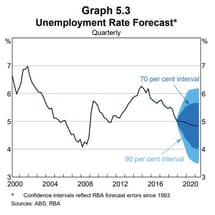

UBS folds: RBA to cut interest rates as unemployment spikes

George Tharenou at UBS has finally joined MB: Recent data clearly shows that the pace of growth is slowing, with weakness in retail, car sales, resi & non-resi approvals, business surveys, home loans & credit.