At last MB and Professor Warwick McKibbin agree, from a nice piece by Adam Creighton:

Guy Carson, chief investment officer at asset manager Quick Brown Fox in Sydney, warns that the bigger economic risk isn’t price falls but the volume of transactions. “The economic fallout from the stalling residential sector and falling house prices is greater than most local economists have suggested, not because of the so-called ‘wealth effect’ but because of the fall in construction work.”

Almost one in 10 workers is employed in building and construction, a 20 per cent increase in six years. Almost three-quarters are home builders. “The end of the largest residential construction boom that Australia has ever seen will lead to a rise in unemployment,” Carson says. “We believe the fallout from the housing market is likely to be bigger than any previous cycle.”

…Warwick McKibbin, economist and former Reserve Bank board member, says the RBA bears some of the blame for swollen debt levels and excessive dependence on dwelling investment. “They should have started lifting rates when Philip Lowe became governor in 2016. That was the right time,” he tells Inquirer, suggesting the official rate could be around 2.5 per cent now, rather than 1.5 per cent. The Reserve Bank repeatedly has suggested the next move in official rates will be up. But few expect that to happen for at least a year.

….McKibbin and Carson say the Reserve Bank should have acted sooner. “The Federal Reserve replaced the dotcom bubble with a housing bubble while the RBA has replaced the mining boom with a housing bubble,” Carson says. The Reserve Bank cut interests rates from 4.75 per cent in October 2011 to 1.5 per cent in August 2016, leading to a fall in average mortgage rates above 6 per cent to below 4 per cent across the same period.

“The problem now is they can’t raise them because house prices are falling and there’s a federal election approaching,” McKibbin says, recalling the blowback from the Howard government when the RBA board lifted rates in the lead-up to the 2007 federal election.

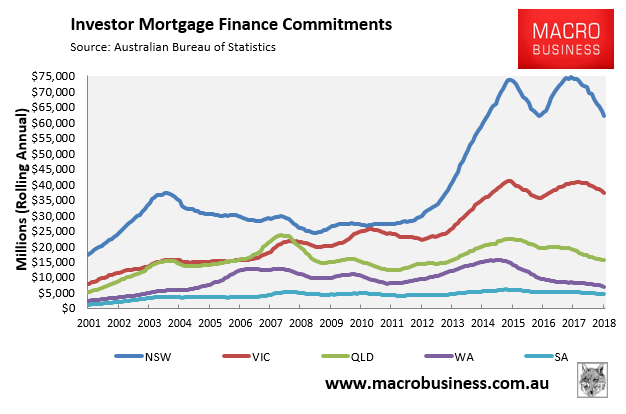

The RBA is directly responsible. But Lowe’s ascension to governor in 2016 was already far too late to tighten and would make no difference today. The interest-only bubble was blown by Glenn Stevens’ RBA from 2012-2016:

This was all the more perverse given Stevens had declared household debt too high in 2009/10 and very successfully deleveraged the sector for several years.

The RBA was unable to hike rates in the 2012-2016 period because the economy was very weak amid the mining bust and the Australian dollar was stubbornly high through the period. It’s mistake was to not consider macro prudential tools earlier with APRA and then to fight against that notion when MB lobbying finally got macro prudential on the drawing board. Those tools did snuff out the bubble in 2016 but MB proposed them from the first rate cut in late 2011.

Ironically, Professor Warwick McKibbin developed the same strange aversion to the words “macro prudential” over the 2012-2016 so he can wear some of the responsibility for the blow off and bust too.