Just in case you’re thinking of buying ANZ

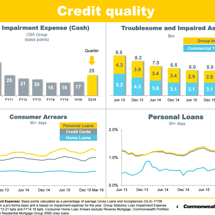

Try some Brian Johnson of CLSA who is all class: 1H16 cash earnings of A$2,782m bore the brunt of A$717m of non-operational specified items (capitalised software –A$441m, restructuring –A$101m, AMBank impairment –A$231m, Esanda gain +A$56m), but even excluding these items, pro forma cash earnings of A$3,499m (2H15 A$3,540m) missed consensus by ~2%.