From Goldman has nicely summarised the recent bank reporting season in terms of net interest margins:

Margin drivers – Lending and deposit spreads to hurt bank margins Competition in the domestic lending space remains intense for both housing and business lending, though we note that investor mortgage lending is currently much less competitive than a year ago given bank repricing and various tightening in lending standards post macroprudential regulation. Specifically,

ANZ’s 1H16 NIM (ex-markets) +1bp hoh, with asset spreads contributing 2bps to NIM as mortgage repricing helped to offset weaker business trends, while deposit pricing was also a positive contributor (+1bps). Divisionally we note Australia was +1bps, Institutional was -5bps (though up 10bps on an ex-markets basis) and NZ was -7bps.

WBC’s 1H16 NIM (ex-markets) +2bp hoh, largely reflecting improved spreads on customer deposits. We note that despite experiencing a fuller period impact from recent mortgage repricing, the asset spread contribution was neutral, with competition across all lending segments offsetting the 5bp gain from mortgage repricing.

NAB’s 1H16 NIM (ex-markets) +2bp hoh, NAB has retained much more of the recent mortgage repricing and benefited by +5bps from asset spreads (peers neutral) and also added 4bps from deposit pricing, partially offset by funding and liquidity headwinds.

CBA’s 1H16 NIM (ex-markets) flat hoh, the biggest headwind to NIM this half was the continued low rate drag on free funds.

Margin performance was divergent for the regionals as BOQ surprised positively with 1H16 NIM +1bp hoh, but BEN’s NIM was down 2bps despite favourable liability mix (with TDs declining and good at call product growth).

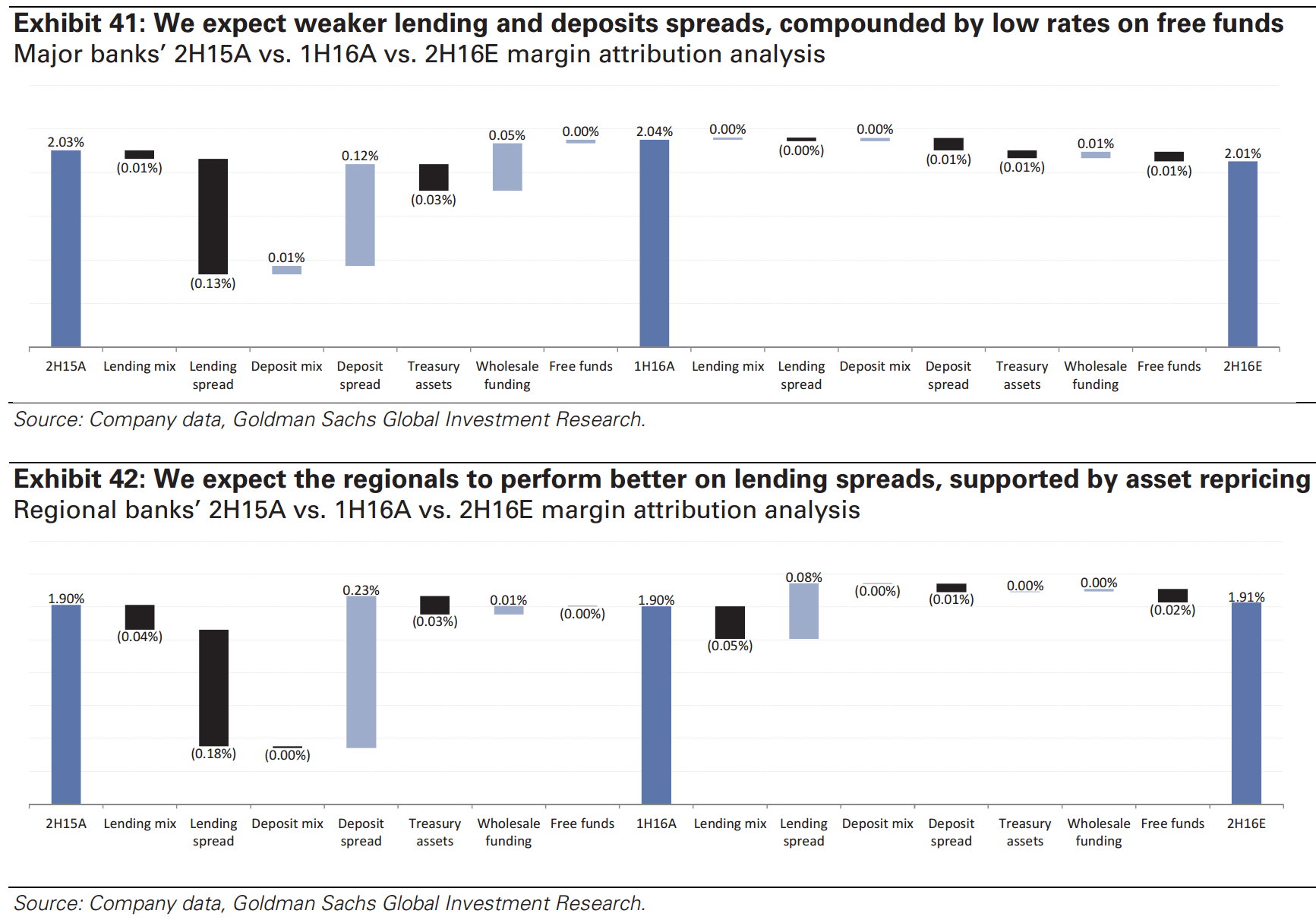

Into 2H16E, we expect the majors to experience weaker margins (c.-3bp hoh) driven by negative contribution from both asset and liability spreads and the impact of further expected rate cuts on free funds. Conversely, we expect the regionals to see NIM +1bp hoh, supported by better lending spreads on mortgage and business repricing, offset by weaker deposit spreads as they move to reprice term deposits upwards in response to wholesale funding pressures (Exhibit 42).

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.