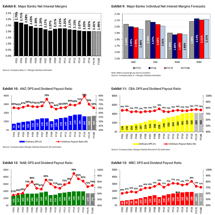

Banks hike fixed-rate mortgages on Trump effect

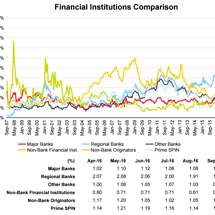

The AFR is reporting mortgage rate hikes: Firstmac, the nation’s biggest non-bank lender, and nine other smaller lenders are discreetly raising fixed-rate mortgages by up to 45 basis points in a move expected to be followed by others as the “Trump effect” begins to bite local borrowers, according to lenders and market analysts.