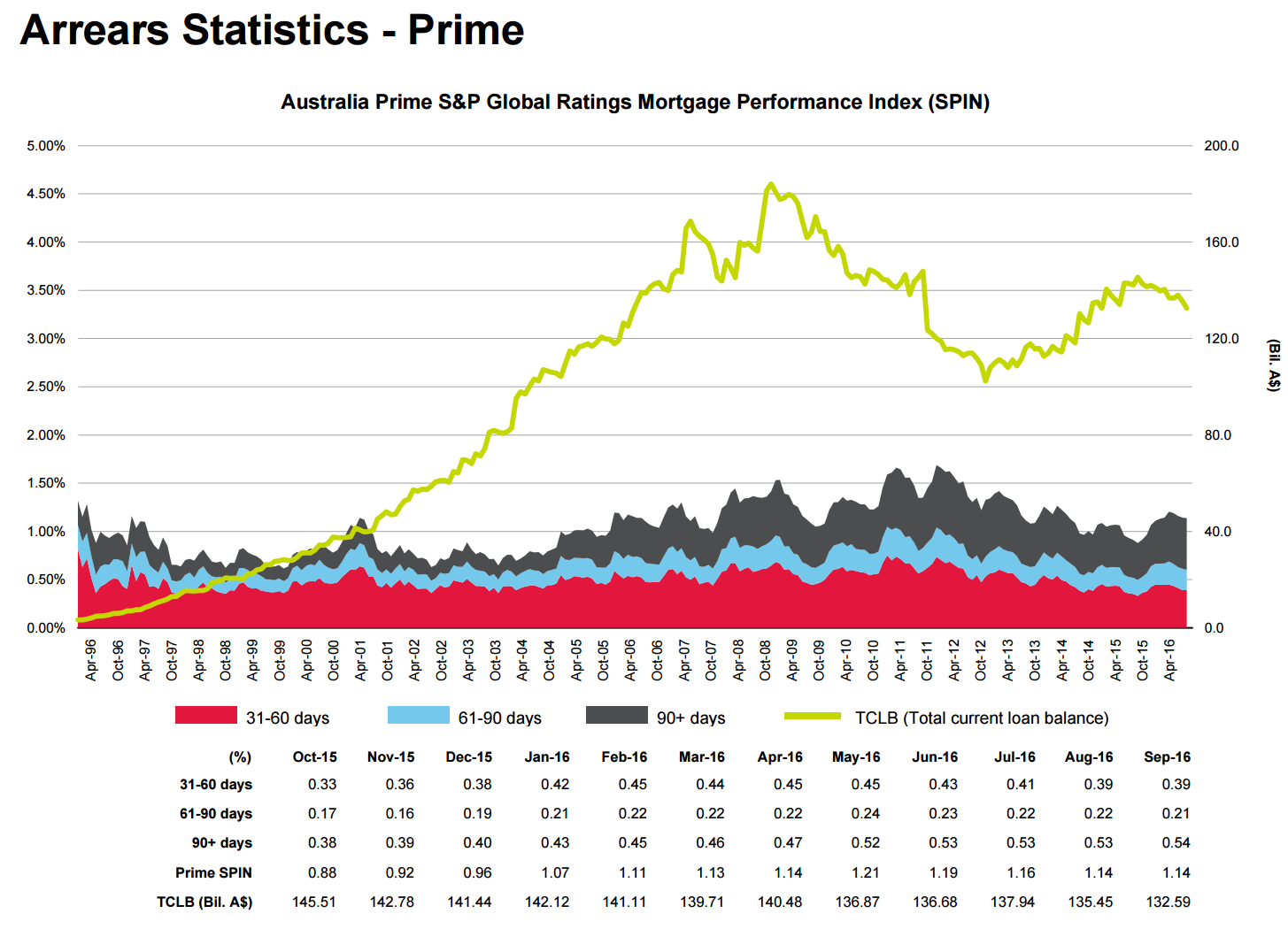

A total of 1.14% of Australian mortgages underlying prime residential mortgage-backed securities (RMBS) were more than 30 days in arrears in September, as measured by Standard & Poor’s Performance Index (SPIN). The figure, unchanged from August, was a divergence from the cyclical trend, in which arrears typically decline between April and November before starting to rise again in December.

Arrears, including capital market issuance, were 25% higher in September than at the same time last year. Excluding capital market issuance, arrears were up 18% year on year. The figures remain below their respective peaks and the average for the past 10 years.

Our data are based on RMBS transactions that include noncapital market issuance, totaling around A$132.5 billion. The SPIN for RMBS transactions that exclude noncapital market issuance, totaling around A$64.8 billion, declined to 1.10% in September from 1.11% a month earlier.

Arrears on full-documentation loans were also unchanged from August, remaining at 1.10% in September. Arrears on low-documentation loans decreased to 4.45% from 4.87% a month earlier. Low-documentation loans make up around 1.2% of the loans underlying prime RMBS transactions, and their performance does not have much effect on the SPIN.

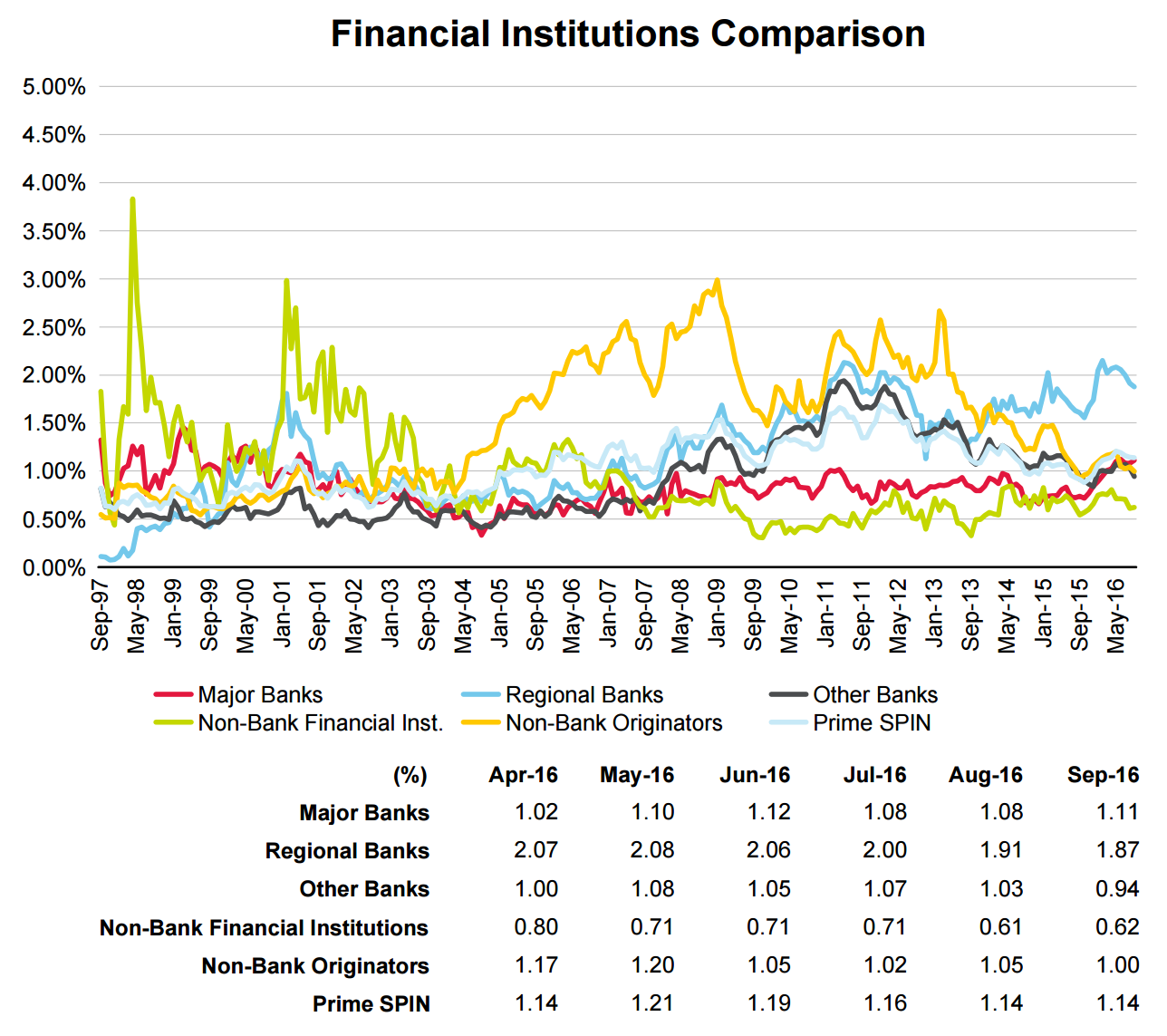

Arrears fell month on month for most originator categories except major banks, which recorded an increase to 1.11% in September from 1.08% in August, and nonbank financial institutions, which recorded a rise to 0.62% from 0.61% a month earlier. Nonbank financial institutions continue to have the lowest arrears among originators, followed by other banks, at 0.94%, and nonbank originators, at 1.00%. The major banks’ loan balances make up more than 53% of total RMBS loan outstandings, and their arrears performance has a large influence on the performance of the SPIN.

A few points:

September is a seasonally very good month for arrears so flat is bad;

by Q1 next year we’re going to see arrears climbing towards GFC levels;

major bank arrears are already worse than during the GFC, and

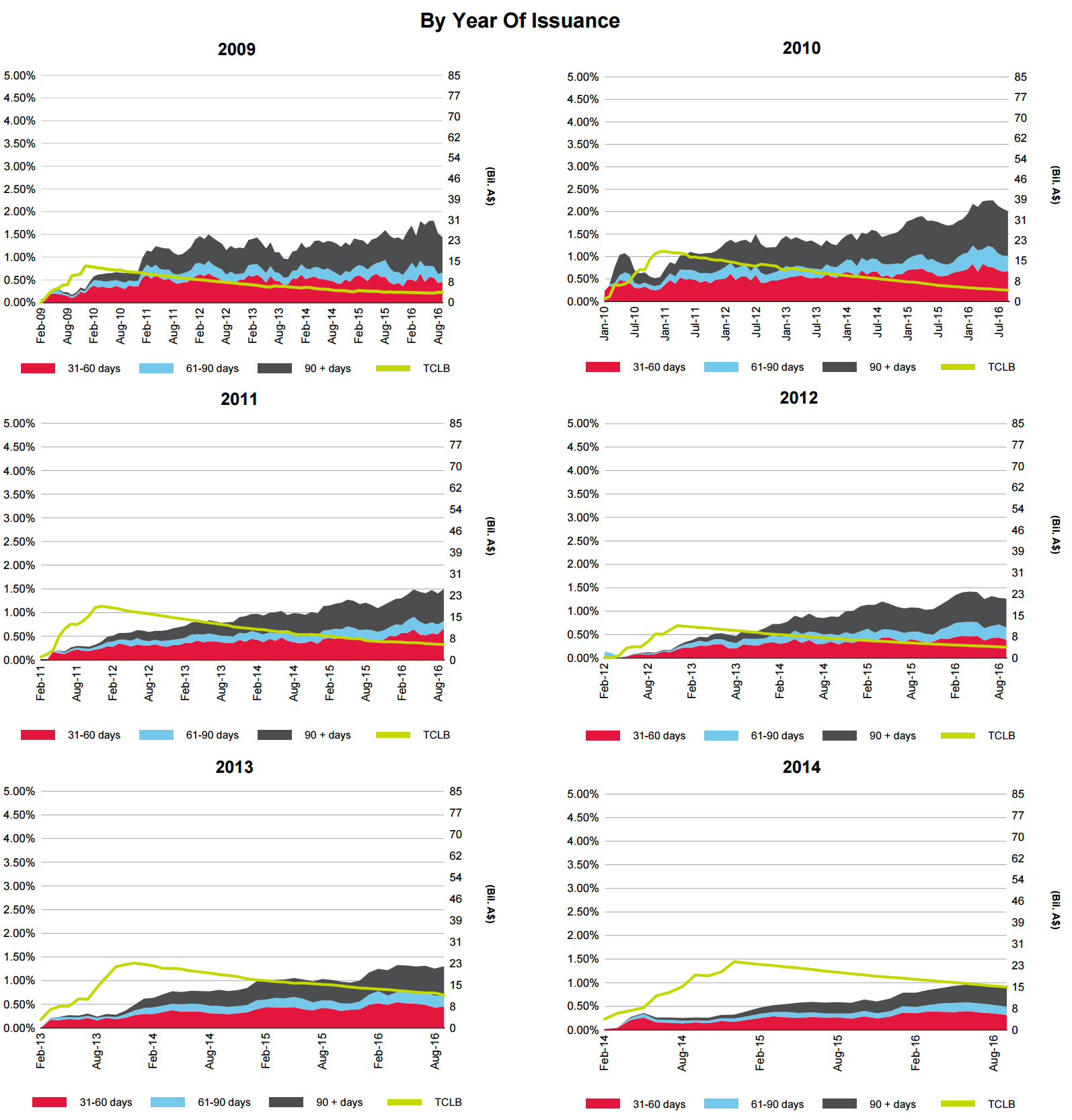

there is nothing especially noteworthy in the vintages:

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.