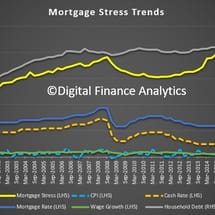

One quarter of households in “mortgage stress”

From Martin North: Digital Finance Analytics has released new mortgage stress and default modelling for Australian mortgage borrowers, to end April 2017. Across the nation, more than 767,000 households are now in mortgage stress (last month 669,000) with 32,000 of these in severe stress.