A staggering 57% of mortgage holders could not handle a $100 increase in their loan repayments, according to new research by Finder.com.au.

This additional $100 is equivalent to an interest rate rise of just 0.45% based on the national average mortgage of $360,600. This means the average standard variable rate of 4.83% would only have to rise to 5.28% to put more than half of mortgage holders in stress.

With increasing interest rates, some borrowers have little breathing room, said Bessie Hassan, money expert at Finder.com.au.

“The typical mortgage holder will begin to struggle once interest rates reach around 5.28% – that’s a pretty small window before borrowing costs start to hurt,” she said.

“The reality is borrowers have over-extended themselves if it only takes a $100 leap in repayments for more than half of homeowners to reach their tipping point.”

Hassan expressed concern about mortgage holders and their exposure to mortgage stress, especially with rising rates forcing borrowers to use a greater percentage of income on their loans.

Looking at higher rate rises, the research found 18% of borrowers could handle a monthly repayment increase of $250 while just 14% could manage $1,000 or more.

There is a $209 monthly difference between the cheapest fixed interest rate (3.59%) and the most expensive (4.59%), Hassan said, meaning borrowers could be “throwing away thousands of dollars” per year.

With the research also showing that 39% of all mortgages are interest-only, this highlights why the Reserve Bank of Australia (RBA) and the Australian Prudential Regulation Authority (APRA) have shown some concern, she added.

Comparing genders, 63% of women and 50% of men would struggle to repay their mortgages with an increase of less than $100 per month.

Across the states, South Australian borrowers were the worst placed with 70% saying they could not handle an increase of less than $100 per month. This figure was lower in New South Wales, Tasmania and Western Australia at 59% and further dropped to 51% in Victoria.

As the RBA said recently:

While the financial position of households has been fairly resilient, vulnerabilities persist for some highly indebted households, especially those located in the resource-rich states.

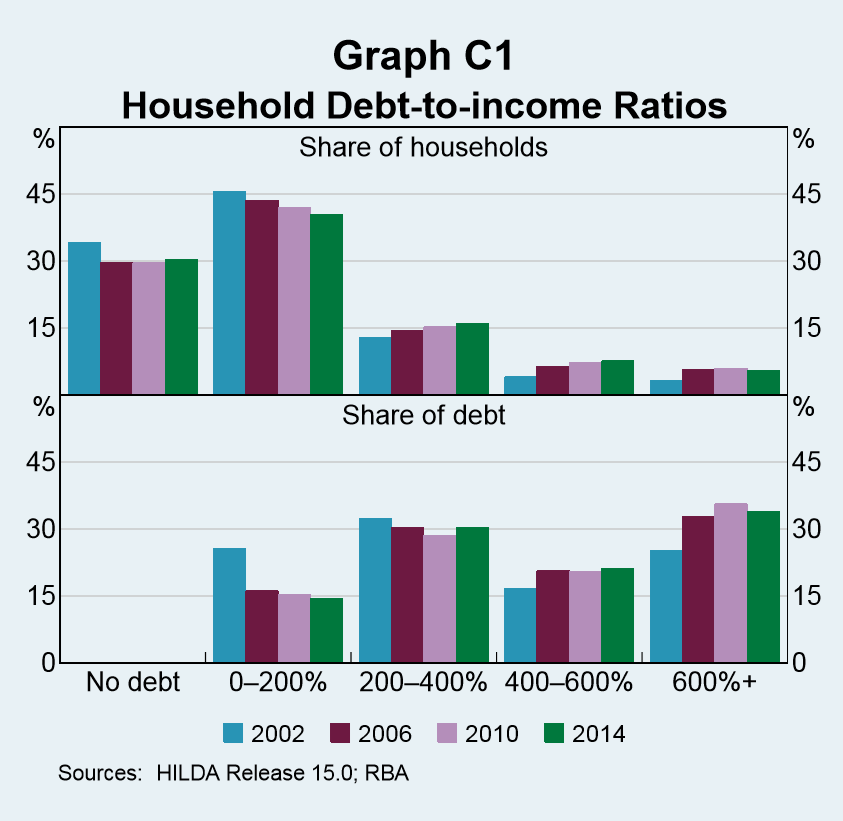

Household indebtedness (as measured by the ratio of debt to disposable income) has increased further, primarily due to rising levels of housing debt, although weak income growth is also contributing. Rising indebtedness can make households more vulnerable to potential income declines and higher interest rates. This is of most concern for households that have very high levels of debt.

Low interest rates are helping to offset the cost of servicing larger amounts of debt and hence total mortgage servicing costs remain around their recent lows (Graph 2.5). In this regard, lenders have tightened mortgage serviceability assessments in recent years to include larger interest rate buffers, which should provide some protection against the potential effects of higher interest rates.

Prepayments on mortgages increase the resilience of household balance sheets. Aggregate mortgage buffers – balances in offset accounts and redraw facilities – are high, at around 17 per cent of outstanding loan balances or around 2½ years of scheduled repayments at current interest rates. However, these aggregate figures mask significant variation across borrowers, with available data suggesting that around one-third of borrowers have either no accrued buffer or a buffer of less than one month’s repayments. Those with minimal buffers tend to have newer mortgages, or to be lower-income or lower-wealth households.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.