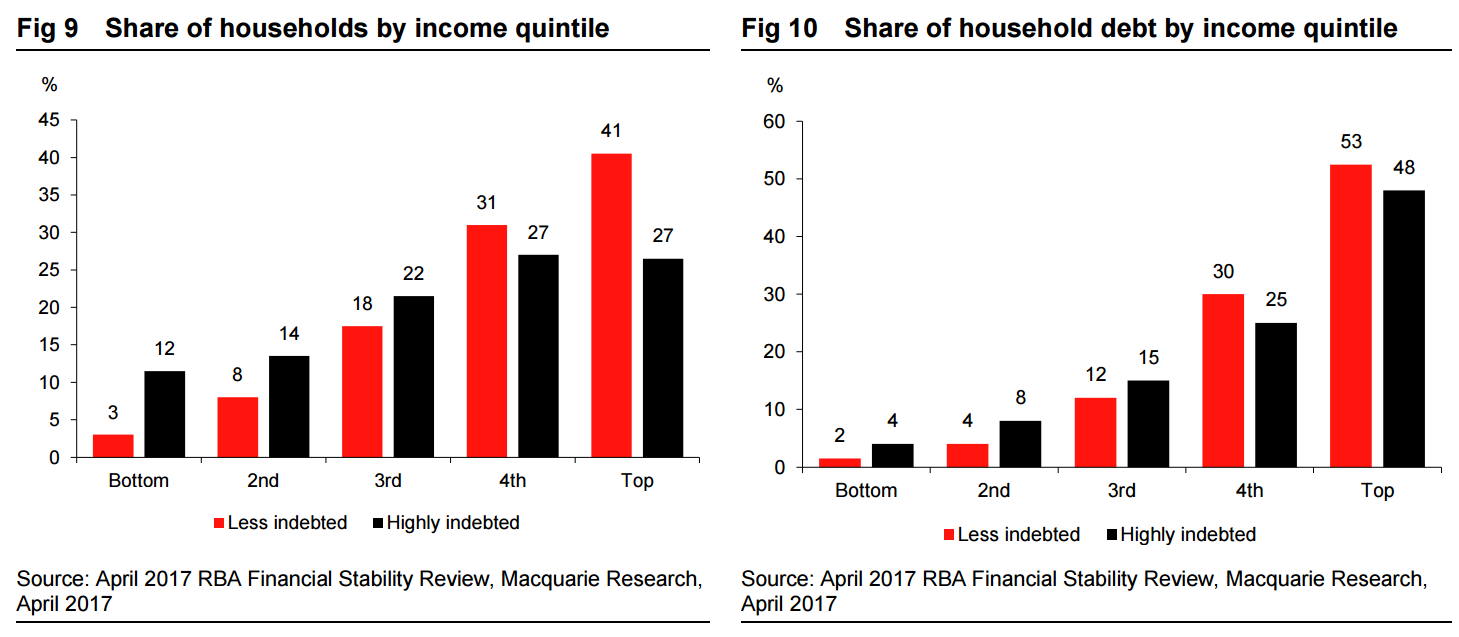

In this regards, the most indebted 10% of households are at most risk from rate increases. Our analysis below dissects this group by income quintile (i.e., highest 10% of households based on debt-to-income measure split into income quintiles). While a large share of debt (i.e., ~50%) resides within the highest income quintile, when analysed by the number of impacted households, the debt burden appears more evenly split between the top 3 income quintiles and falls to 12-14% of households in the lowest income quintiles.

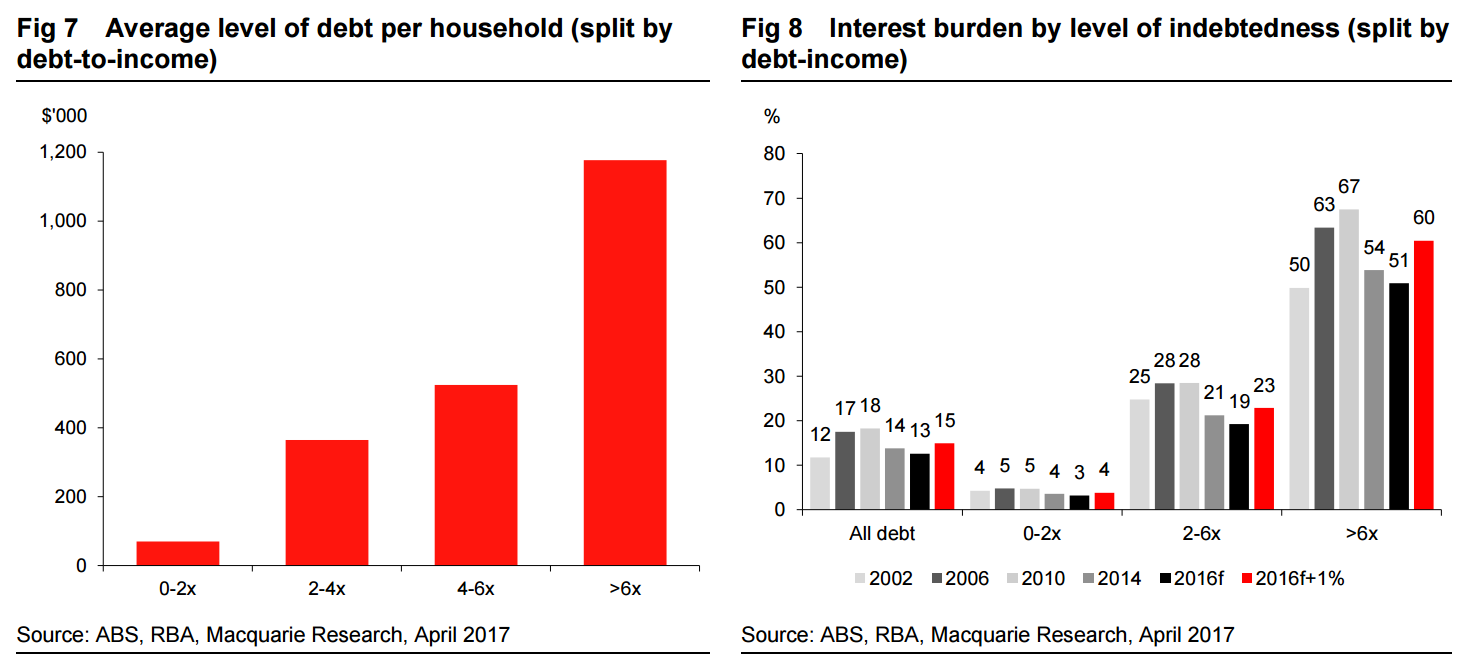

As the figures below highlights, the interest burden for those households is material. We estimate the interest servicing cost alone accounts for 40-60% of total household disposable income. While we suspect a large share of those households would have interest-only loans, should they start to repay principal the level of repayments increases to 75-120% of disposable income. As a result, recent changes around interest-only loans may have a significant impact on these households and force some of them to reduce their level of debt. As the figure below highlights, we estimate household repayments would increase by ~60% when repayment schedule changes from interest-only to principal and interest.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.