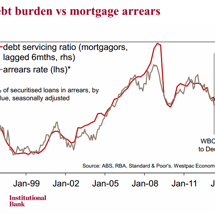

Where are bank regulators taking us?

Deputy Governor of the RBA, Guy Debelle, gave a good speech last night that sensibly provided support for Australia to adopt the structures of global financial re-regulation: The BIS Committee on Global Financial Stability, on which I sit, has published some work on that recently, but there is more to be done.