J.P. Morgan has a useful note this morning on the impact of the proposed bank levy:

Who Wins and Loses? The introduction of the FCS was intended to ‘level the playing field’ to allow all ADIs to have insured deposits to remove ‘depositor bias’ toward larger financial institutions. However, ironically, the insurance fee relative to assets and earnings is 3 times higher for smaller institutions because they tend to 1) hold more retail deposits, 2) have a higher proportion of revenue from NII (due to less diversification), and 3) a lower ROA (due to less scale and efficiency) – (refer Table 4 and Table 5). In addition, whilst the scheme may be intended to support institutions such as CUBS who may be at more risk of failing as opposed to the major banks, ~75% of the funding for the scheme would actually be facilitated by major bank deposit holders (refer Table 6).

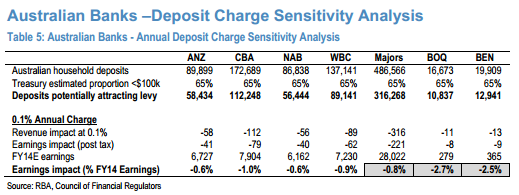

Earnings Impact (in Isolation): Assuming a 10bp annual fee, and the charge being applied to balances <A$100,000 for household deposits (corresponding to 65% of the value of deposits by Treasury), major banks may see a ~-1% FY14E earnings impact (refer Table 5). However, regional banks BEN and BOQ may be more adversely impacted, with an FY14E earnings impact of ~-3%.

Other Potential Consequences – It would be unlikely for the smaller institutions to absorb this impost and may look towards a ‘pass through’ to the ultimate beneficiary – the depositors. As a reminder, banks directly passed through Financial Institutions Duty on deposits and Bank Account Debit tax on withdrawals until their removal in 2001). Accordingly, major banks will then be in the position to 1) also pass on the impost to customers (whether it be straightthrough like FID and BAD above, or through deposit fees, deposit pricing, or recaptured through asset pricing to reflect the higher cost of funds), or 2) absorb the charge and therefore price deposits at relatively more attractive levels than their smaller peers to gain market share.

Valuation considerations – With banks fully valued (refer Table 1), they can ill afford any perceptions of earnings risk. However, we note that the regional banks (UW BEN and UW BOQ) are currently trading expensive relative to our valuations and have greater earnings risk from this issue.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.