World of Statistics tweeted the following, claiming that “India leads the world as the top remittance recipient country and is the only country in human history to ever exceed $100 billion in annual remittances”.

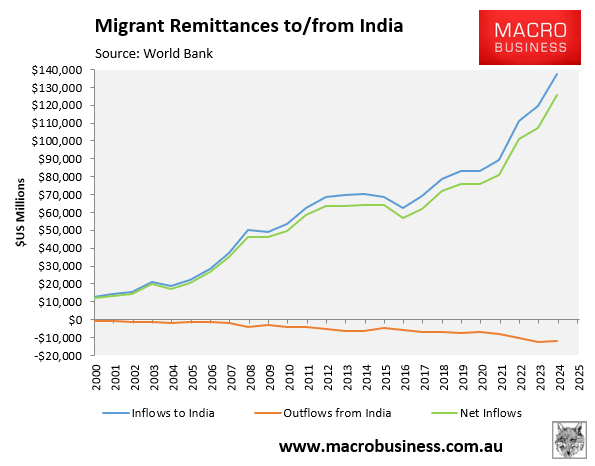

In fact, the latest data on migrant remittances from the World Bank shows that in 2024, India was a net recipient of US$125.6 billion in remittances from migrants living in other countries, up from US$57.1 billion in 2016:

This means that net migrant remittances were equivalent to around 3.2% of India’s GDP in 2024.

IND Money explains how migrant remittances have become an increasingly important component of India’s economy:

Money sent home by Indians working abroad quietly supports millions of households and also plays a meaningful role in the country’s economy. These transfers, known as remittances, are the income migrants send back to their families in India.

For families, remittances are everyday support. RBI’s survey notes that about 99% of the total value of inward remittances captured by authorised dealer banks was for family maintenance and savings.

In simple terms, this money helps pay for education, healthcare, housing, emergencies, and regular household expenses. In many homes, remittances are not extra income. They are part of the monthly financial base.

Remittances do more than support families. They also help India at the country level. India buys many things from abroad, such as crude oil and electronics, and often imports more than it exports. Money sent home by Indians working overseas helps cover part of that gap.

In 2023-24, remittances were large enough to cover 42.2% of India’s merchandise trade deficit, which is the gap between what India imports and what it exports. That is one reason these inflows matter so much for the wider economy.

They are also a steady source of foreign money for India. Unlike some foreign investment flows that can rise and fall quickly, remittances usually stay more stable because they come from Indians supporting their families back home. This makes them an important cushion for the economy.

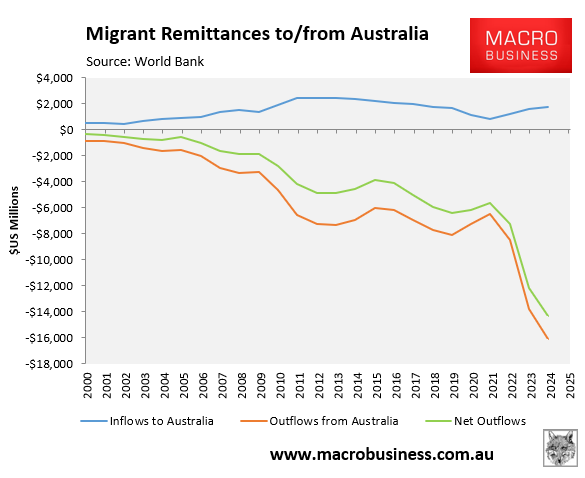

Indians migrating and living in Australia have also become a major financial drain on Australia’s economy:

According to the World Bank, $US14.3 billion of net remittances were sent from Australia in 2024, up from only $US784 million in 2004.

Net migrant remittance outflows from Australia have also more than doubled since 2019, when $US6.4 billion in remittances left Australia.

Based on the average AUD/USD exchange rate of 0.66 in 2024, this figure suggests that Australia lost around $A21.7 billion from net migrant remittance outflows in 2024 alone, roughly equal to around 0.84% of GDP. That is a large leakage by advanced‑economy standards.

Separate data from Money Transfer Australia, which drew on figures from the World Bank, ABS, KNOMAD, and DFAT, estimated that US$25 billion (A$37.9 billion) was sent abroad from Australia in 2024, with India (US$4.8 billion) the largest single recipient.

“The surge comes as Australia’s migrant population hits historic highs, fuelling unprecedented levels of money flowing back to families and communities across India”, noted Indian Link.

“These funds help families cover essentials such as education, healthcare, and housing, while also boosting local economies across India”.

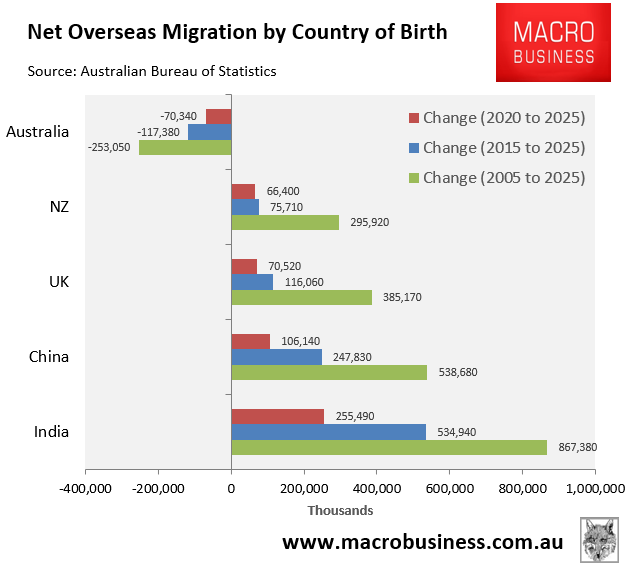

The large volumes of remittances sent home by the Indian diaspora make sense, given that they are now Australia’s largest migrant source after expanding by 867,000 via net overseas migration over the 20 years to 2024-25:

Indian Link projected that remittance outflows to India will continue to rise as the migrant population expands in Australia.

The heavy leakage of migrant remittances from Australia is another cost of immigration that policymakers choose to ignore.