Australia should look to Canada to solve the rental crisis

Australia’s current rental crisis has been fundamentally driven by excessive immigration-driven population growth in a supply-constrained market.

This excessive demand has driven rental vacancy rates to a historical low and pushed rental prices higher, squeezing affordability.

Anyone doubting the relationship between net overseas migration (NOM) and the rental market only needs to examine the following chart:

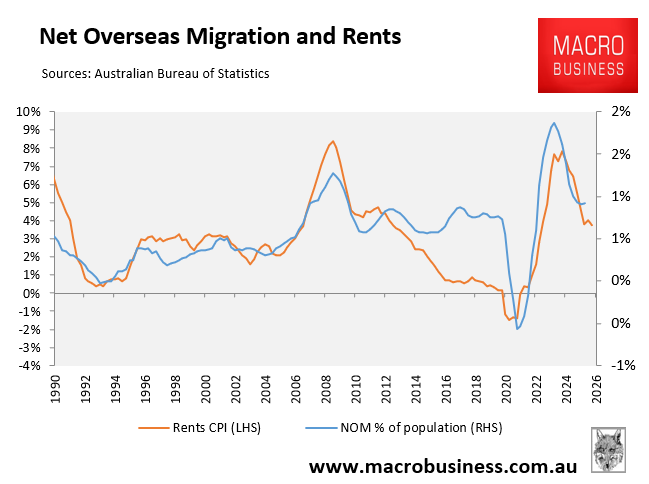

Higher NOM has typically corresponded to higher rental growth.

However, the rate of new dwelling construction also matters. As illustrated above, rental growth cratered between 2015 and 2020 due to a large increase in the supply of high-rise apartments.

Annual Australian dwelling completions averaged 207,400 in the five years to 2020, well above the 163,300 annual average over the five years prior (i.e. 2011 to 2015) and the 176,200 annual average in the five years afterwards (i.e., 2021 to 2025).

This five-year boom in the supply of mostly small one- and two-bedroom apartments from 2015 to 2020 successfully put downward pressure on rents, even amid continued strong population growth.

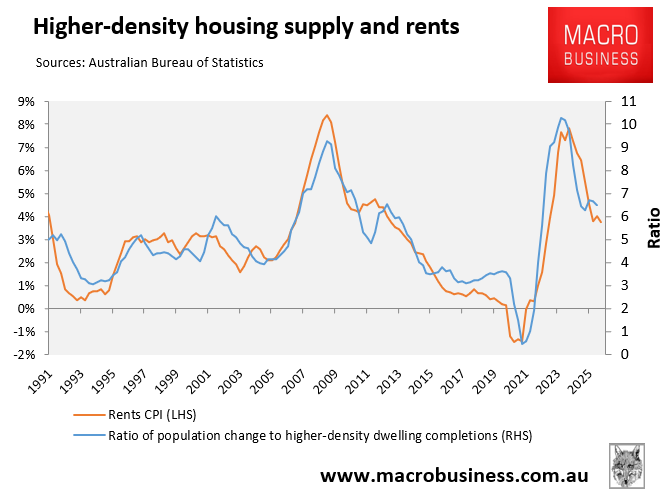

As illustrated below, there is a particularly strong relationship between increases in the supply of higher-density housing relative to population growth and rent growth.

This likely reflects the fact that apartments make up a disproportionate share of the rental market: just over 60% of apartments are renter-occupied, compared with around 20% of detached houses.

The interplay between population growth (demand) and apartment supply is, therefore, the fundamental determinant of rent growth. When immigration rises, it puts upward pressure on rents, other things equal, whereas increased apartment construction has the opposite effect.

Unfortunately, the record post-pandemic surge in net overseas migration has been met with a sharp reduction in new dwelling construction, particularly apartments, resulting in escalating rental growth.

There are several reasons for the slowing of construction in the post-pandemic period, including:

- Structurally higher interest rates.

- A circa 40% rise in construction costs.

- A circa 33% rise in residential lot values.

- Labour shortages and high insolvency rates in the construction industry.

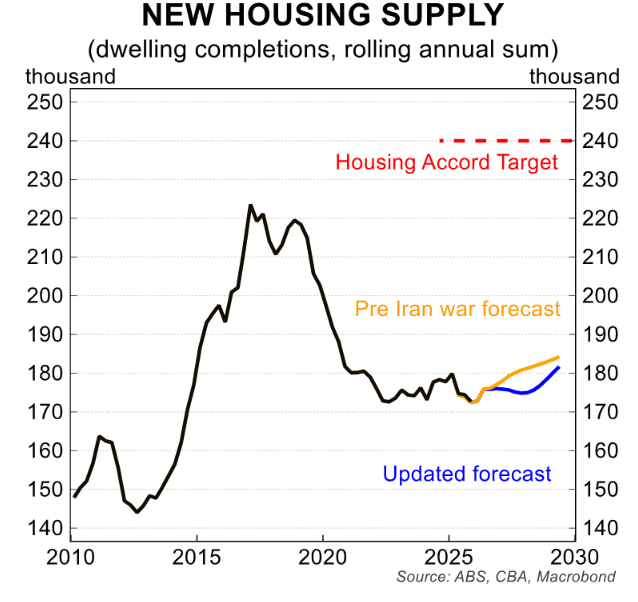

The outlook for dwelling construction remains poor, given that interest rates are widely expected to increase to a 15-year high by the end of 2026. Residential builders and developers have also warned that input costs are likely to rise further amid the global energy shock from the war in the Middle East.

Indeed, CBA recently downgraded its construction forecasts due to the global energy shock.

In CBA’s baseline scenario, only 885,000 homes will be completed over the five-year National Housing Accord period to 2028-29, which is 315,000 (26%) fewer than the 1.2 million construction target.

Therefore, with new dwelling supply remaining constrained amid high costs and interest rates and labour shortages, the only way to realistically ease shortages and the rental crisis is to cut demand via immigration.

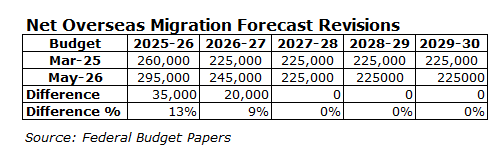

However, the latest federal budget upgraded NOM by 55,000 over the next two years, which will add significantly to housing demand.

As a result, Australia’s rental crisis, which is already the worst in living memory, is destined to worsen with demand via population growth continuing to run well ahead of supply.

Canada provides the solution:

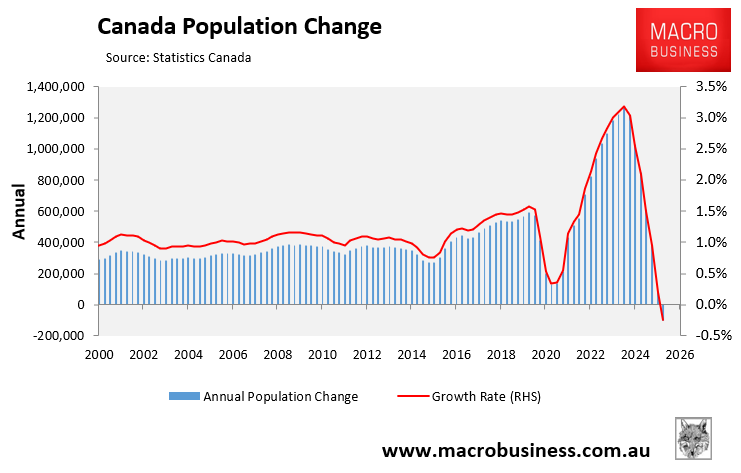

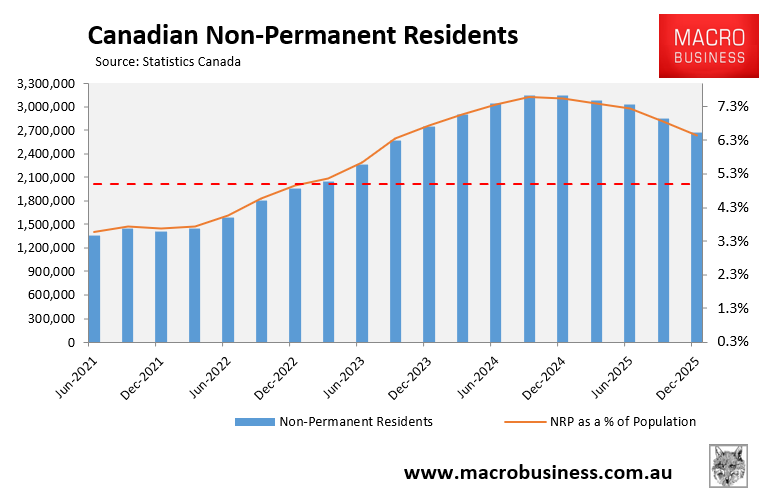

Canada’s population grew by just over 3 million people (7.9%) between the September quarter of 2021 and the September quarter of 2024.

A surge in non-permanent residents (NPRs), also known as temporary migrants, drove Canada’s record population growth. NPRs rose by nearly 1.8 million between the September quarter of 2021 and the December quarter of 2024, from 1.36 million to a peak of 3.15 million. As a result, the share of NPRs rose from 4.1% of Canada’s population in the September quarter of 2021 to a peak of 7.6% of the population in the December quarter of 2024.

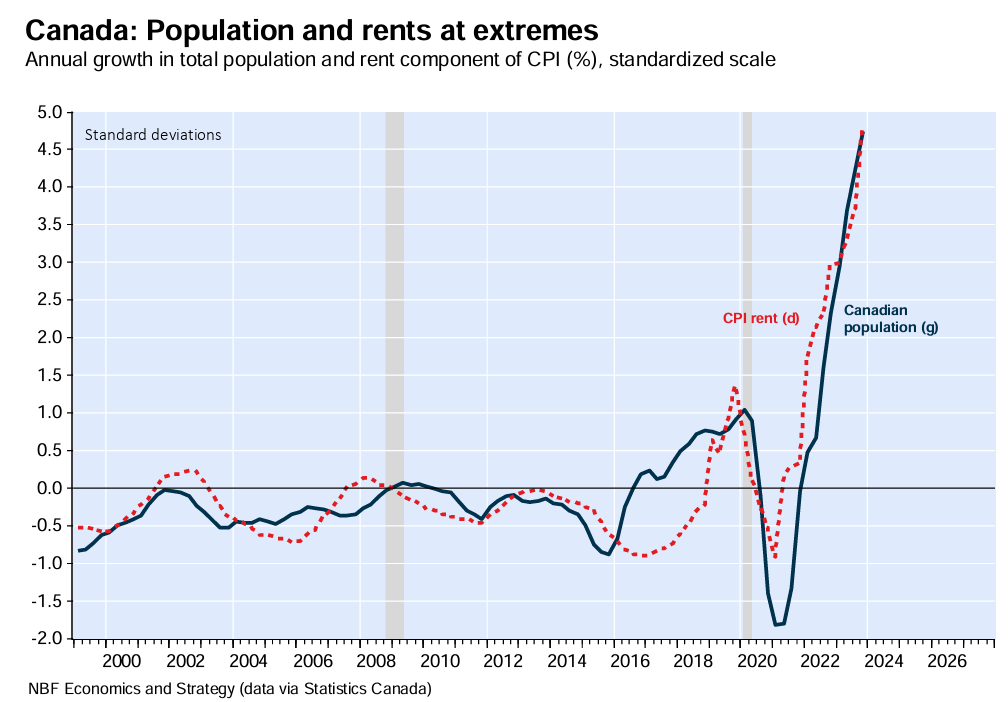

Canadian tenants suffered, with rental vacancy rates falling to record lows and rental growth surging.

In early 2024, Canada’s rental and population growth were extreme

Amid growing pressure on housing and infrastructure and political backlash over high immigration levels, the centre-left Canadian Liberal government announced sweeping immigration cuts in October 2024 to “pause” population growth.

The measures include reducing annual permanent-resident targets, restricting international-student and temporary-worker admissions, and tightening asylum and border rules.

Canada’s permanent residence targets have been cut from 500,000 to 365,000 by 2027.

Canada has set specific targets for NPRs, including international students (the most substantial reductions) and temporary foreign workers.

By the end of 2027, NPRs are forecast to make up about 5% of the Canadian population, down from 7.6% at their peak.

Canada’s immigration reforms have proven extremely effective.

The Canadian population declined by 100,000 (0.25%) in the 2025 calendar year, the first reduction since records dating back to the Second World War began. The stock of NPRs fell by about 462,000 in 2025, and their share of the population declined to 6.5%.

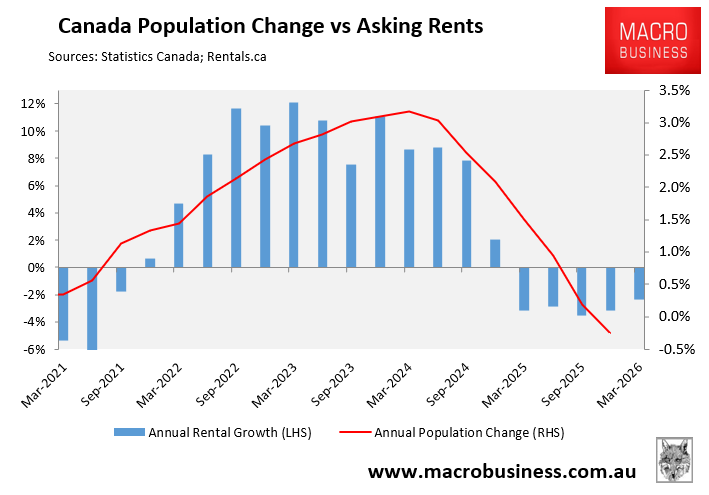

The impact on the rental market was immediate, with asking rents falling.

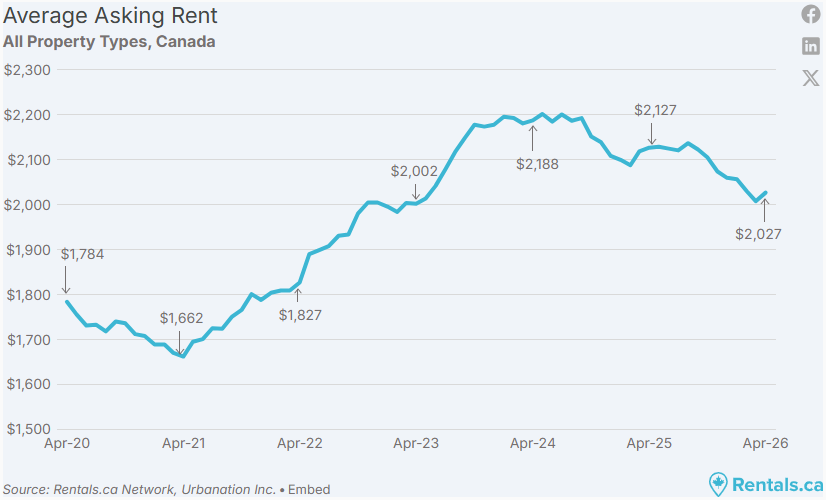

Indeed, the latest data from Rentals.ca show that average asking rent in Canada has fallen for 19 consecutive months in year-over-year terms:

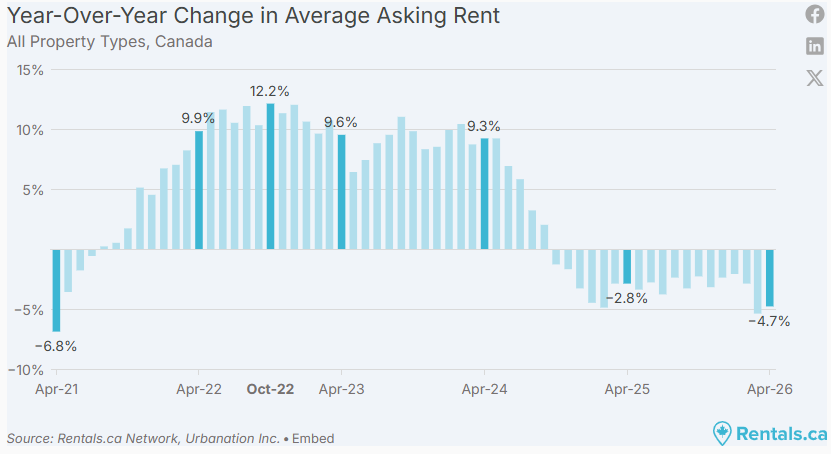

Rentals.ca reports that asking rents in April 2026 were 7.4% lower than in April 2024, although they were still 21.9% higher than the low of $1,662 in April 2021 during the COVID-19 border closure:

The takeaway:

The data above show that Canada’s sharp immigration cuts are rapidly solving the nation’s rental crisis, saving tenants thousands of dollars each year in rent.

Australia’s federal government should emulate Canada and ease its rental crisis by sharply cutting immigration.

Doing so would rebalance demand with supply, lifting the rental vacancy rate and placing downward pressure on rents.