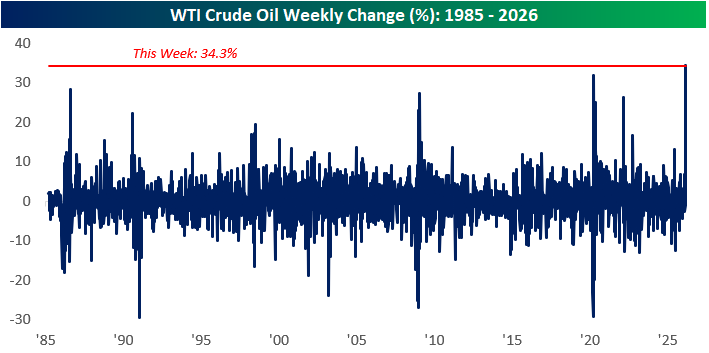

Since the latest round of conflict in the Middle East kicked off on the 28th of February, the cost of a barrel of oil (WTI) has risen by $23.98 compared with the final close of markets prior to the war, representing a rise in oil prices of 35.6%.

Taking a longer view, the current level is the highest oil price since October 2023 and still significantly below where prices were during the height of the impact of the war in Ukraine on commodity markets.

According to an analysis from the Bespoke Investment Group, last week’s oil market action saw the single largest increase in oil prices in relative terms since at least 1985.

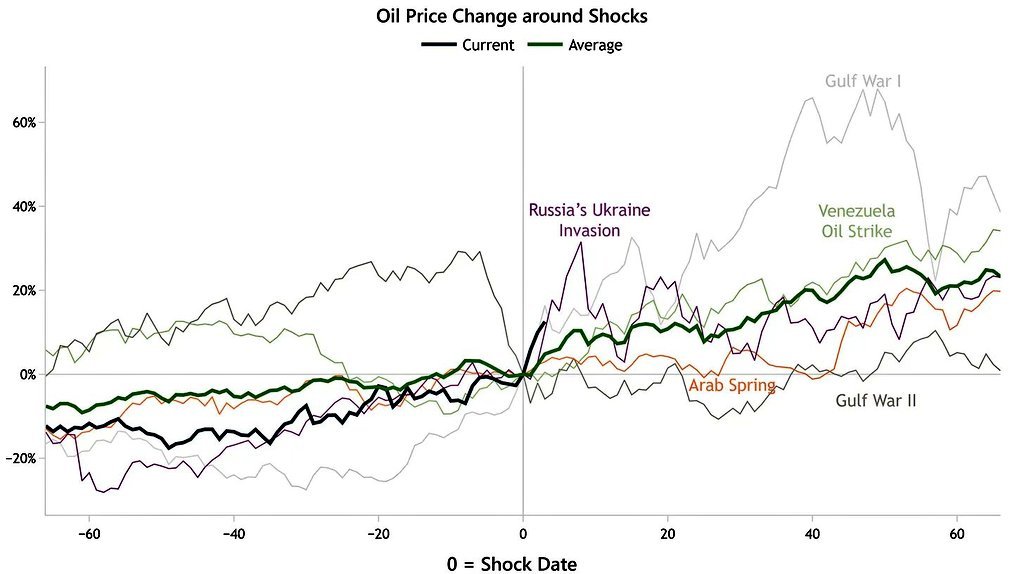

But an analysis from The Merchant’s News’ Jack Prandelli suggests that oil markets can initially underprice major shocks driven by supply shocks within energy markets.

Perhaps the best example of this in his analysis was that of the first Gulf War.

The full impact in terms of oil prices wasn’t felt for ~50 days from the start of the initial shock to markets.

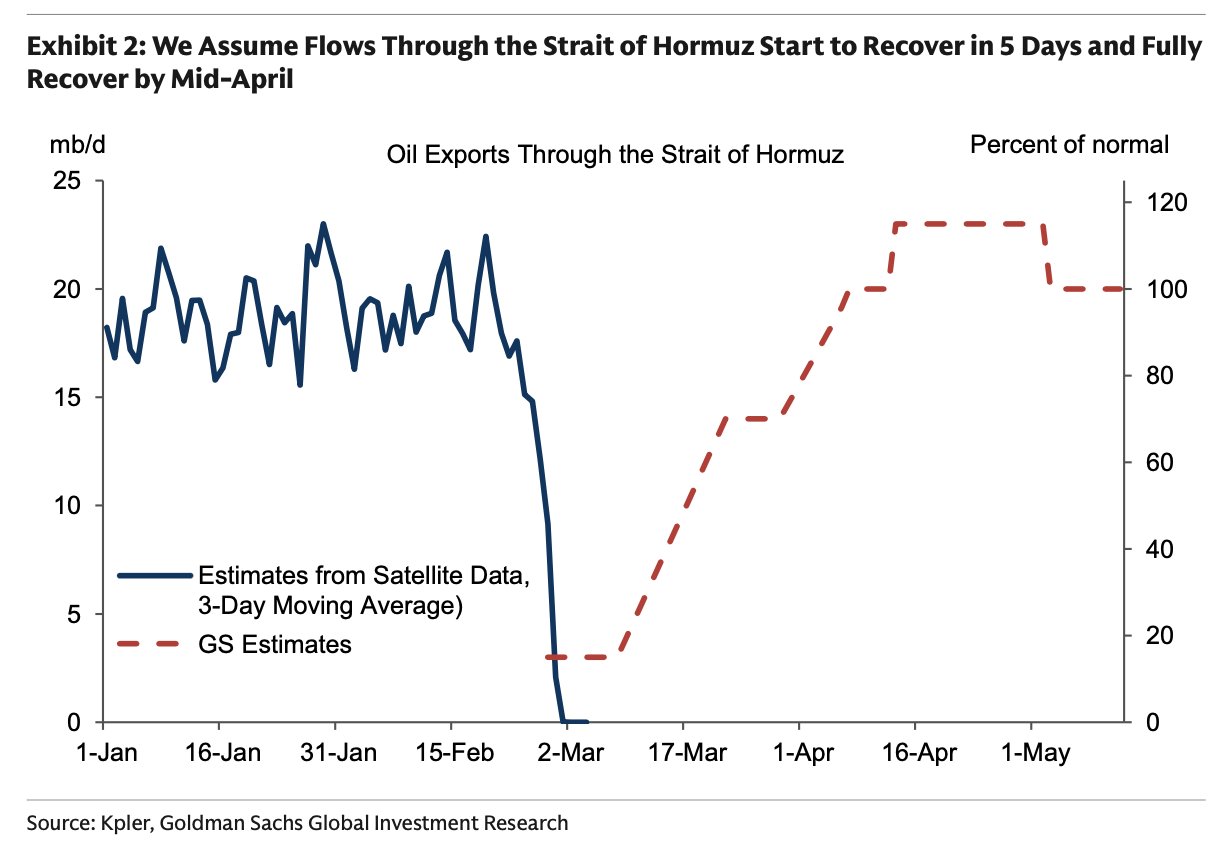

The problem is that the impact of the effective closure of the Strait of Hormuz on the flow of oil is far greater than that stemming from the first Gulf War.

Even assuming the full utilisation of pipeline infrastructure to circumvent the Strait of Hormuz, over 12 million barrels a day of oil and other hydrocarbons will be trapped in the Persian Gulf.

According to Canadian energy analyst Eric Nuttall: “We are experiencing the largest loss of oil supply in history (3X bigger than the 1973 Arab oil embargo)”.

This was followed by commentary from the Qatari Energy Minister and QatarEnergy CEO (the world’s largest LNG producer), Saad al-Kaabi that oil could reach over $150 per barrel in “two to three weeks” and that a prolonged conflict could “bring down the economies of the world”.

The minister also warned that even once the conflict has drawn to a close, it could take “weeks to months” for Qatar to return to a normal cycle of energy export deliveries.

Unfortunately, like a daytime TV infomercial, there is more to it and the news is not good.

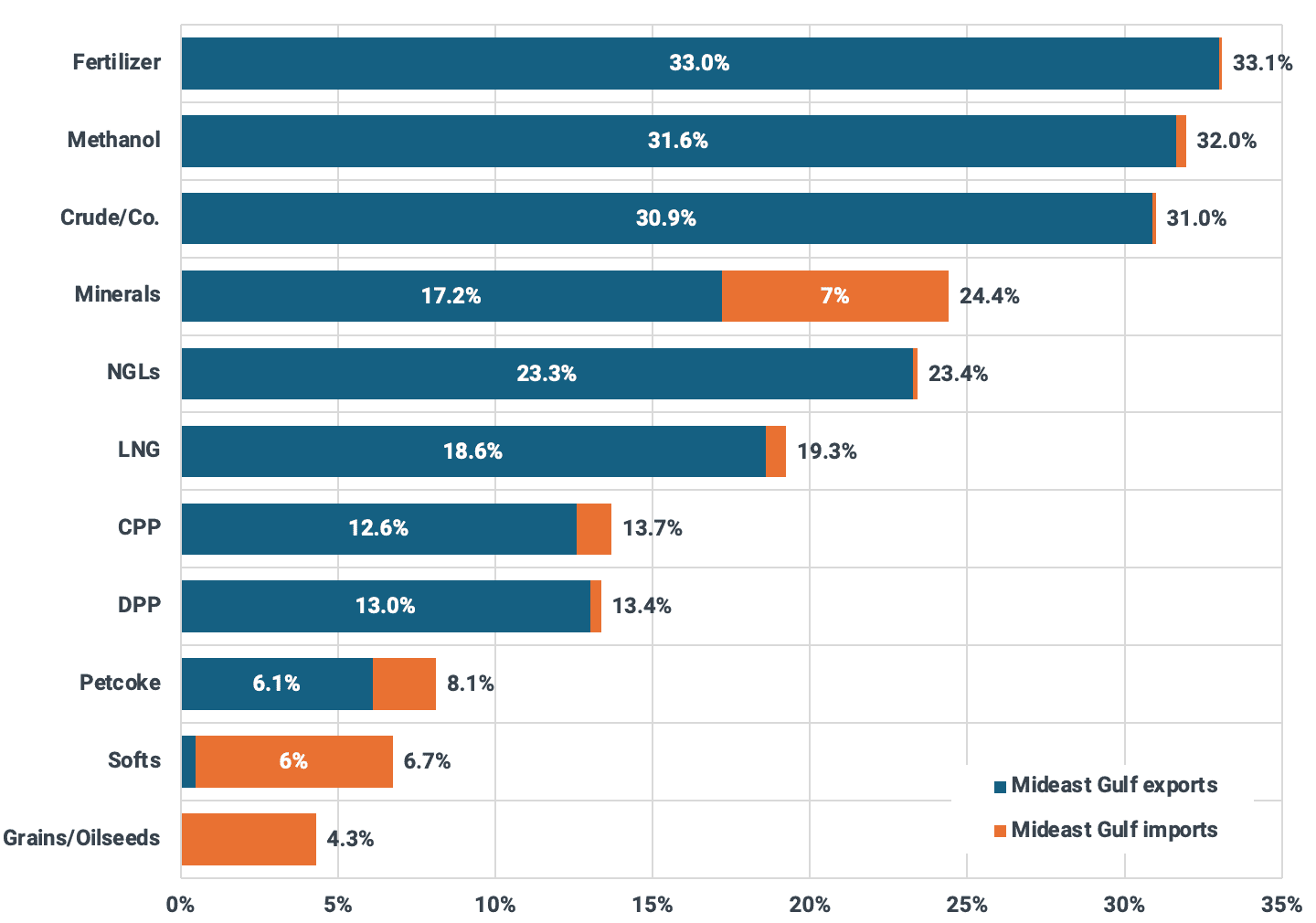

According to an analysis by Kpler, one-third of the world’s fertiliser exports pass through the Strait of Hormuz.

17.2% of the world’s broader exports of minerals pass through it.

Along with 18.6% of the world’s LNG exports.

The Takeaway

Despite the relative calm in broader markets, as silly as that may sound, the reality of a protracted closure of the Strait of Hormuz to most traffic is far more challenging than is currently being priced in.

In a matter of weeks, global aggregate fuel, fertiliser, and gas shortages will all become a reality.

While there is hope that conflict and interruption to vital trade flows will be resumed soon, the reality may unfortunately be quite different, as both sides appear far from an accord that could bring the conflict to a close.

I recently discussed this at length with Martin North of Digital Finance Analytics, where we went through the charts and numbers relating to the conflict and the flow of vital commodities.