President Donald J. Trump oversees Operation Epic Fury at Mar-a-Lago, Palm Beach, FL, Feb. 28, 2026. (White House photo by Daniel Torok)

We have become spectators in the demolition of an era.

We are now, more than ever, bit players in what is unfolding, so we are detached. We can’t take our eyes off the spectacle, as we cannot be sure the demolition of certainty will not arrive at our doorstep. Should it do so, we know we are largely helpless.

The global macro, as it has been served to us for about 80 years, is being roasted on the spit marked by nothing more than the occasional plaintive bleat with no more substance than that of a stray wildebeest being consumed by a pride of lions.

That global macro was for at least 30 years after the end of the Second World War about ensuring economic certainty for the developed world, if only to make sure it didn’t become communist.

People across all levels of the western world had relative certainty of employment, motivated by products easily accessible with what they earned as they rebuilt the world.

With this certainty they could focus on themselves and their families, largely freed from the prospect of either their state or any other state capriciously intruding on their lives.

Where states did intrude, it was for discernible good – health, education, and reduced discrimination first and foremost.

Institutions developed globally to ensure stability and economic growth – world banks, a General Agreement on Tariffs and Trade, the OECD, UNESCO and numerous others – ensured an architecture to the age and an edifice to the seeming certainty.

As economic substance returned, credibility sufficient to ward off the prospect of communism returned to the elites of the developed world after the two world wars and global depression they had delivered the previous century.

The rules they espoused represented the basis for planning. This was most notable in finance and credit, where the probability of repayment vastly increased in stable societies with governments promoting growth, diverse economies, and a range of occupations that included principle-based education in mathematics, reasoning, and expression, as well as teaching, law, medicine, and administration.

Credit became easier as the repayments became more certain, employment became more sure, and the prospect of war was lessened.

The only risk was the prospect of labour price increases or commodity input increases, meaning the currency being repaid devalued through inflation.

After about thirty years, the removal of the US dollar tie to gold and the sudden advent of OPEC pricing the oil all economies needed meant that inflation became the issue, particularly after capital discovered the scope to move production to lower-cost locations and the gulf which opened between labour productivity and share of the economic dividend and the return to capital from the early 1970s.

In the 1980s capital began the slow process of removing administrative processes dedicated to ensuring system integrity, to focus on efficiency and better return to capital.

In the UK and US, where it began, it was promoted in the name of individual choice, but the effective choice was the uptake of large, and historically unheard of, levels of debt and the consumer society by the population at large, largely to offset the decline in spending power from their share of the economic dividend.

The biggest beneficiaries were global banks, as distinctions between investment and savings banks, implemented after the collapses of the Great Depression in the US and Europe, were removed.

The dawning realisation that money was created as debt, and the revenue streams of the burgeoning credit society, became the basis of a complex array of traded financial instruments in the search for ever better yield. Married to government and quasi-government debt issues, pension and investment schemes proliferated, as entire sections of society became financialised, from British pubs and Australian water rights to US and Australian pensions and superannuation.

But the geopolitical underpinning of the financialised world was changing.

The Soviet Union ended in 1991, setting Russia on the crash capitalism path to dictatorship, as communist China welded party dictatorship to capitalism and financial market mercantilism to lift millions out of poverty.

The developed world took on a state and consumer debt explosion and the widespread financialisation of education and housing markets as manufacturing was outsourced and ‘services’ became the mantra.

The advent of the internet in the 1990s and the multiplier effects of the computer age meant that more of life became online, which in turn meant that more of all work could potentially be done online.

At the same time the manufacturing which had enabled the neoliberal age was leaving the developed world except where retained for reasons of national security or political clamour.

After precursors with a number of asset managers in the 1990s and the Russian and East Asian banking crises of the late 1990s, the 2008 cardiac arrest of the global financial system was met by flooding the system with money, accessible primarily by the affluent and large capital agglomerations. These increasingly took the money and funded rentier positions or bid up asset prices.

But the social concerns about the implications of the 2008 crisis were only slowly addressed by developed-world polities, amidst mounting concerns about immigration, housing prices, private debt and the long-term employment outlook.

In the US this brought Donald Trump to power in 2016 as a reaction to the political inaction about widespread concerns on all these in the US and, to a large degree, a mounting sense that the polities of the developed world were more about serving the interests of large corporates and the very affluent than they were about the concerns of ordinary voters.

Trump floundered as Covid arrived, bringing further unknowns to the certainty that had seemed to underpin the age, while mounting concern about global warming and the effects of anthropogenic activity merged with suspicion that developed-world working people were being held more accountable than those in emerging economies.

Trump nearly overthrew democracy in the US when voted out, but his replacement by the moribund Biden administration provided little re-engagement of working people, in particular, with the political process. Across the developed world – in North America, Europe, Japan and Australia – belief in the integrity and focus of the political process had deteriorated similarly.

In 2024, an attempt to ensure a further term for a plausibly senile Biden brought the return of Trump. Emboldened by the first-term experience, within days of returning to power, he unveiled tariffs as a means to support employment, flying in the face of decades of ‘free trade’ espoused by most of the developed world.

The NATO alliance, which has been at the centre of strategic certainty over that same period, has been undermined by his determination to remove US presence in the Russia-Ukraine war.

After the Biden administration had used the global financial system to attempt to force Russia’s hand to back down in Ukraine, emerging nations are increasingly hedging their position about the centrality of both the US dollar and of the global institutions which reconcile trade issues and investment flows. A rising China offers an alternative not seen since the demise of the Soviet Union.

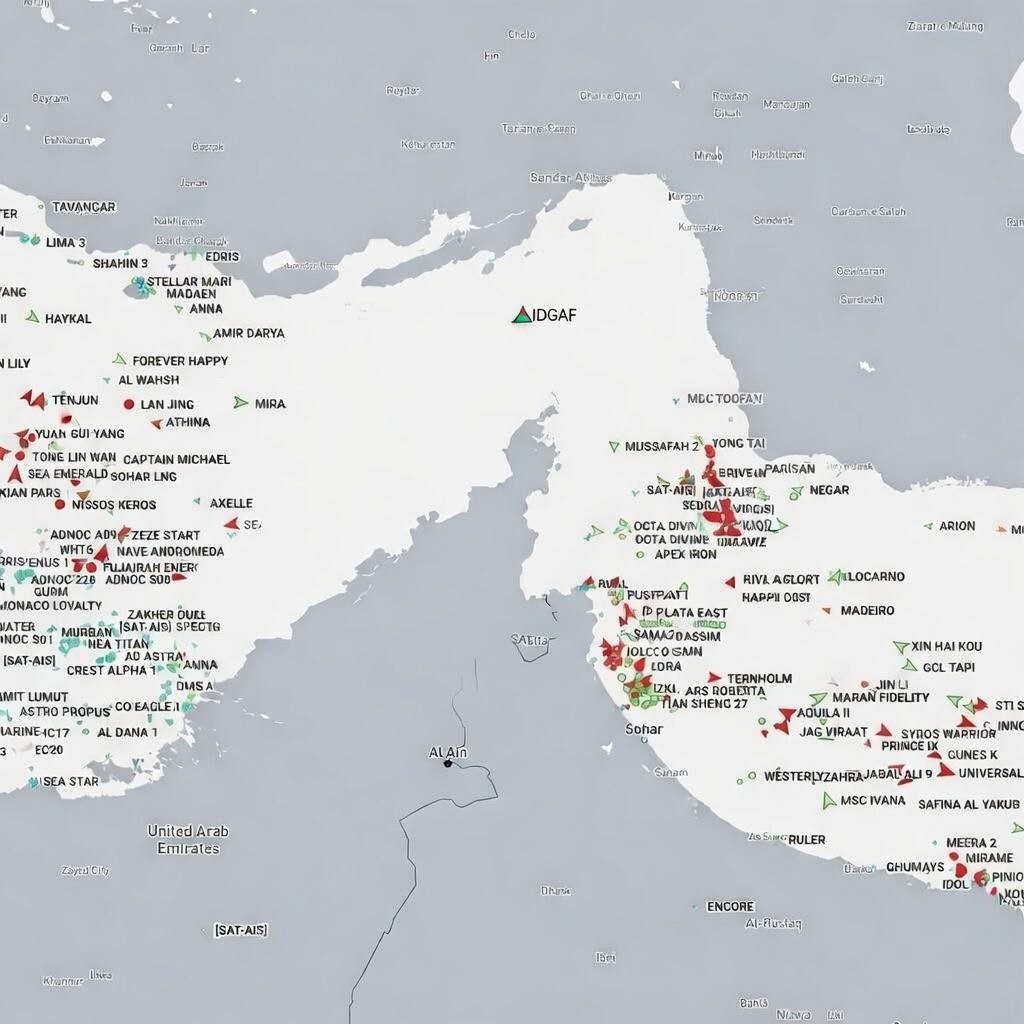

But the fire to end the rules-based international order, if well prepared by others, has been lit by President Trump’s unilateral attack on Iran, in alliance with Israel, in late February 2026.

Despite being viewed as a pariah on the global stage, Iran is home to 90 million people, possesses significant oil and gas production capacity, and holds a strategic position over the Persian Gulf’s energy supply.

Almost no matter what happens from here, the world will see a spike in energy prices, which will ignite further inflation concerns, and the political stability that had been eroded for a generation has been exposed as a fraud by the nation most central to upholding it in the 80 years since WW2.

The tariffs being thrown about on the whim of a president, who has militarily kidnapped a president in Venezuela, asserted a US right to Greenland, now struck at Iran, and is already talking about a deal to address Cuba, mean that all nations now need to seek their own industrial and manufacturing certainty and, likely, the fostering of military capability.

All investment from here will be inherently a greater risk than it was in the past. That means higher interest rates. This will be a major issue in nations which have pushed debt to address political failure to reconcile the division of proceeds of economic growth and logically lead to questions about who, why, and how the beneficiaries have benefited.

The outcome could be a rough journey. But the neoliberal era is over, and the rules-based international order it asserted is now solely for the history books.

The Straits of Hormuz, choke point of a good chunk of the world’s energy