When all is said and done, the RBA can do 3 things this Tuesday

- It can lift rates

- It can leave rates alone

- It can drop them

The last is the easiest to dismiss.

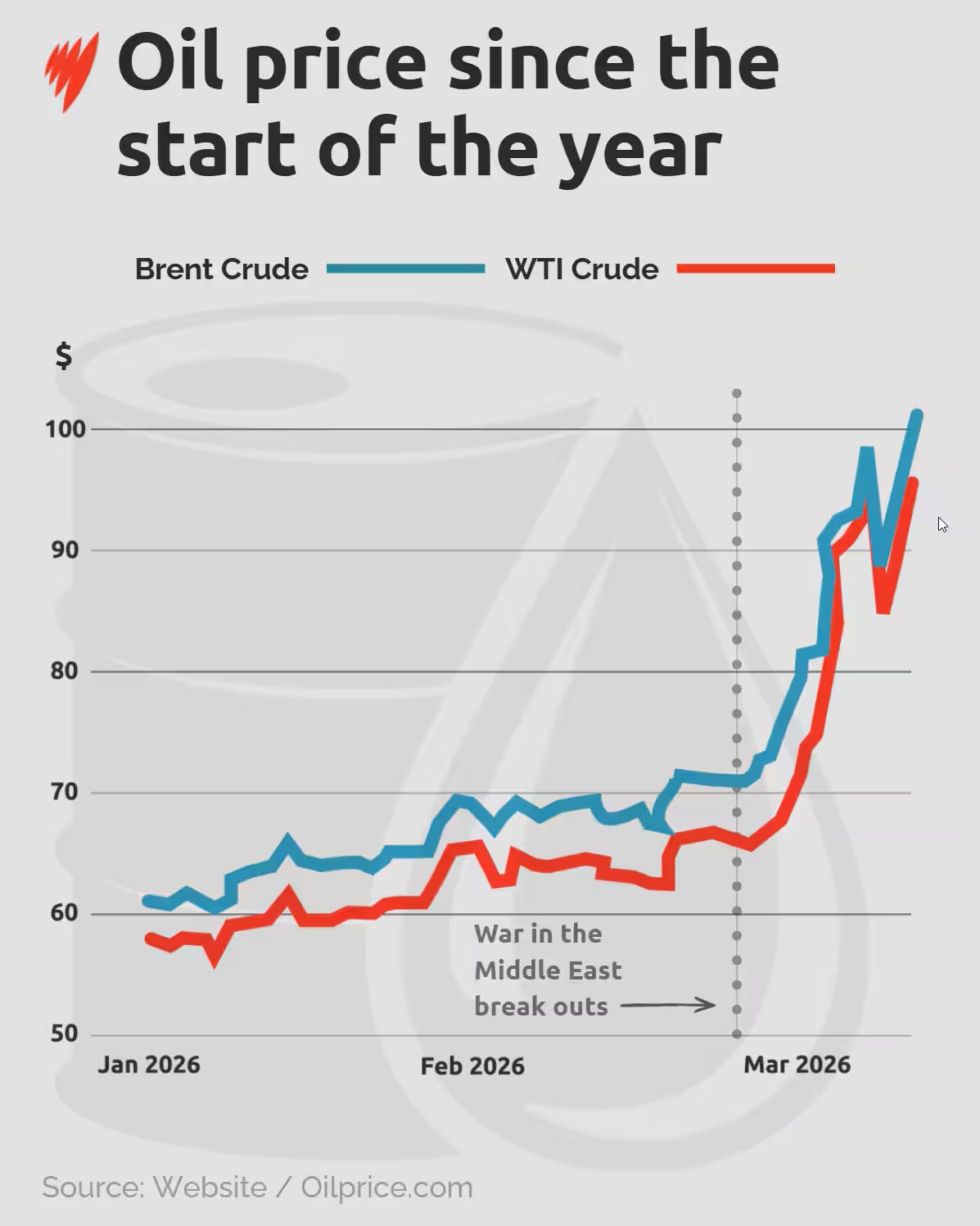

In February, the RBA told us, rightly, that inflation was running hotter than they liked and that a rate hike was needed to temper pressures. Since then, the price of petrol has increased by about 70 cents a litre across most of the country, with diesel rising by an even greater amount.

We can be as sure as night follows day that this increase is already reflected in the prices we will see for fruit and vegetables this week, meat shortly afterwards, and everything else in short order.

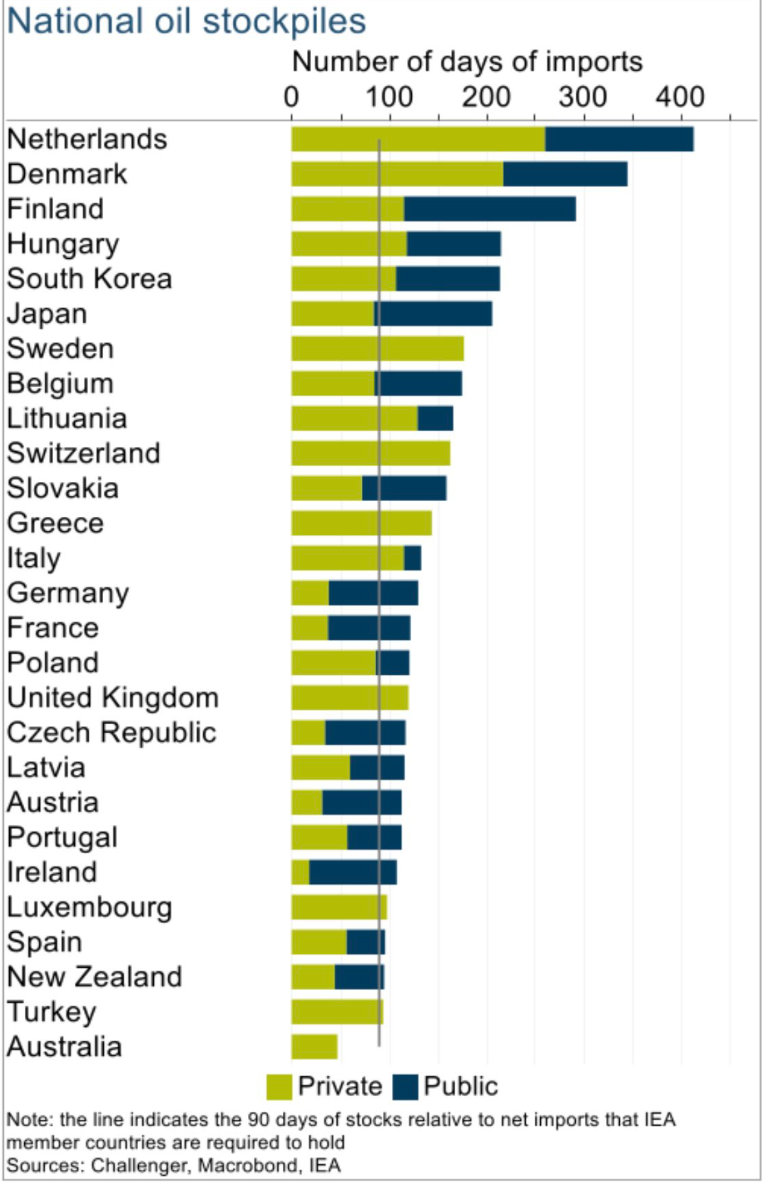

The price increases have occurred despite the government tweaking laws to ensure retailers aren’t price gouging. This gives rise to the possibility that it isn’t price gouging driving the rising prices, but the simple fact that in a nation with storage capacity for about 30-35 days’ worth of its fuel consumption – about the lowest in the developed world – people are concerned about being able to fill their tanks at any price in the foreseeable future.

Despite regular warnings coming from politicians and bureaucrats about ‘panic buying’ for a nation with as many mega four-wheel-drive utes on the road as Australia now has, and with the dearth of fuel reserves in storage as Australia now has, the urge to top up on fuel is common sense for most people.

The fact that our politicians and bureaucrats cannot acknowledge this exposes the gulf between them and the national interest as perceived by the electorate.

Returning to the options the RBA faces, the concept of leaving rates alone is next in the queue. This is almost certainly what the politicians are hoping for.

To arrive here, the RBA would need to consider its job done with the single rate rise it has kicked into play on the field now doused in rising fuel costs, with the outlook set alight.

The RBA knows, as do the politicians and the bureaucrats, that inflationary pressure is not anchored in the spending propensities of the individual consumer, but rather in the aggregate consumer in a population being force-fed heavy volumes of immigration.

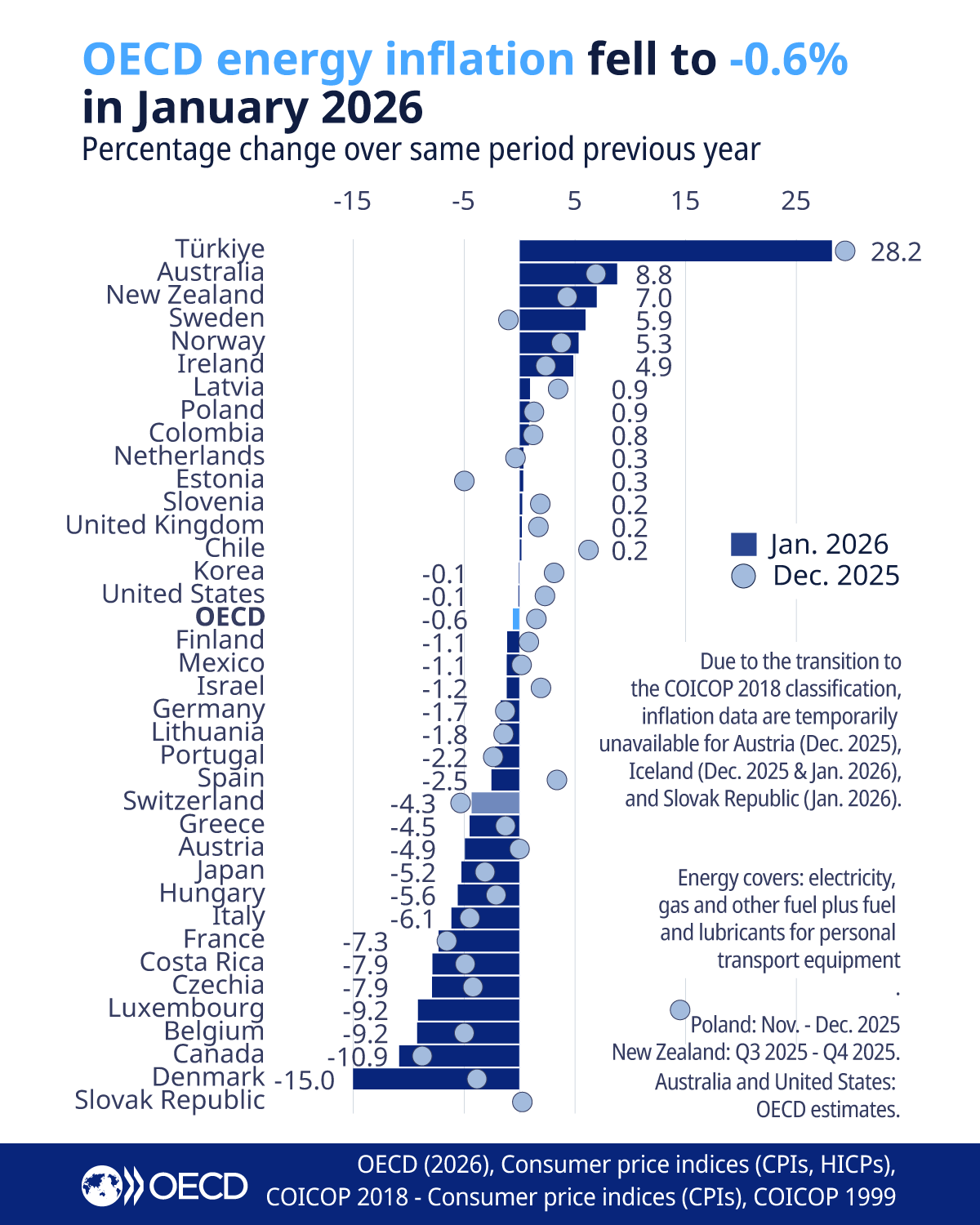

This pressure is in combination with what is known as non-tradable inflation. This is inflationary pressure largely baked in. The rents, the electricity bills and rates, the car registrations and educational outlays, the insurance premiums, and, of course, the commuting costs— the outlays people can’t easily get away from.

Everyone knows, and the RBA knew before its February hike, that such spending is what has driven Australian inflationary pressure and that the February rate hike will have had only a marginal impact on that type of inflation.

They may consider that a 30% jump in fuel costs will have a similar effect in curbing tradable inflationary pressure. People on the street are highly unlikely to be spending more on anything other than fuel and are likely to be cutting back on discretionary spending just to fit in the additional fuel costs.

The only other delusion that could enable an RBA hold is the psychedelic idea that, as soon as the Iranians buckle, the prices will drop back to where they were five weeks ago.

But for the here and now, prices are certainly going to follow the fuel price up, and an RBA hold would give rise to the possibility of losing grip on inflation and possibly another house price surge as ‘investors’ or the cashed up realise there is nothing else moving on a local investment street featuring consumers being hammered.

That brings us to the idea that there will be a rate hike come Tuesday. At that point, there must surely be a question about the appropriate size, given that the rising fuel outlay is going to be a very significant inflationary pressure, and the RBA will know that the rate hike in February is unlikely to make much of a dent in the largely non-discretionary inflation Australia had at that point.

From there comes the idea that a 30% jump in fuel costs may necessitate a 50-basis-point hike. That would likely bring howls of protest and an inclination on the part of the government to point the finger at the RBA for taking ownership of the decision.

Indeed, 50 basis points may even be enough to push large numbers of stressed mortgage payers to the breaking point. Ample evidence points to much of the electorate being in a stressed situation regarding rents or mortgages.

That leaves us all wondering if the whiff in the air is an economic implosion. This situation is exacerbated by a heavily indebted economy that relies heavily on lightly taxed commodity exports, with many individuals assuming that exchanging houses at ever-inflating prices is a viable economic model.

At that gloomy point come several other considerations which take us to the kernel of the malaise we are now in. For Australia, the economic problem is not so much demand management as the structure of our economy and the policies that have shaped it.

The first backdrop point is that, in 2008 and again in 2020, when crises threatened to overwhelm the global economy, central banks around the world responded by flooding it with cash. Funding windows, swap lines, investment concessions, and direct fiscal stimulus.

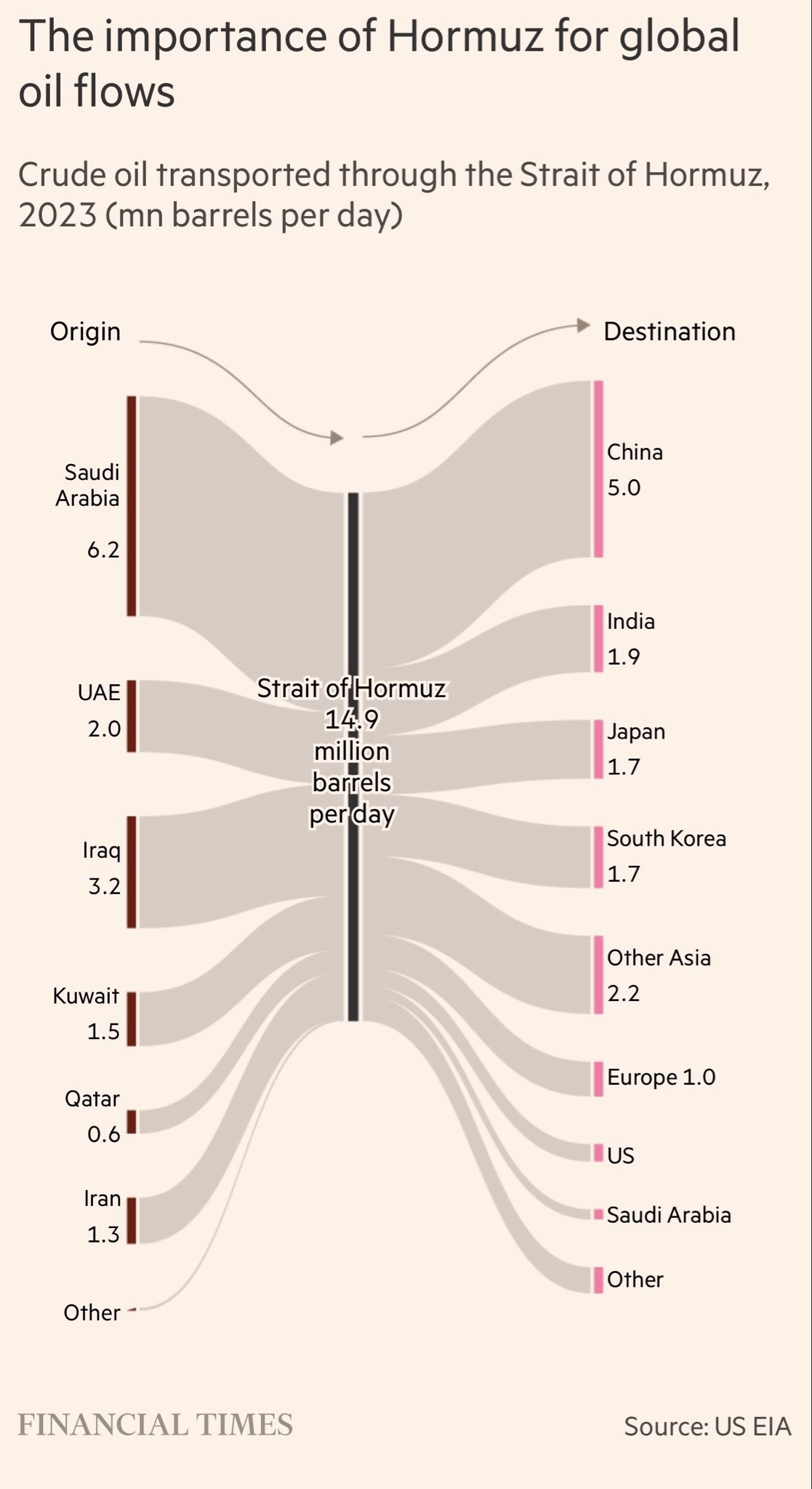

Two weeks into the war against Iran and the halt of crude flows out of the Strait of Hormuz, it is obvious that global markets are experiencing a similarly sized phenomenon.

We also know that last week, many nations with the capacity did so, contributing to an emergency release of global fuel reserves. At that point, the question becomes one of whether, in deliberations about coordinated action to support fuel availability, the question arose, ‘So if this doesn’t work, it will be coordinated fiscal stimulus again, yeah?’

A look around the developed world from there sees the US never too far away from a debt ceiling crisis, the EU remaining bound to considerable financial rectitude in an economy already wearing an energy shock from Russia and Ukraine, a China now facing demographic headwinds and with a financial system hole, a Japan which has taken a bond bath for a generation and an Australia where government outlays are at all-time highs.

That may fit with the ideas of US President Trump, who would no doubt like to open the spending sluices but would treat the future peoples of that developed world like the scumbags he has referred to the Iranian leadership as.

Australia couldn’t get it right even when crude prices were falling, and that is largely because we ceased producing and refining our own and became price takers for others.

We are all scumbags now.

But those of us awaiting an RBA decision this week would note that we are all scumbags now.

The RBA can essentially jack up rates and treat mortgage- and rent-stressed Australians as scumbags through its servicing requirements, or leave rates unchanged and treat future Australians as scumbags through inflation or likely higher costs of actually owning a house.

Maybe we can wait for the world to roll out fiscal stimulus and point to others as being in a worse predicament than ourselves.

Further scumbaggery comes from both sides of mainstream politics and the bureaucracy. These have deindustrialised Australia so much that we make very little of what we use; we traded that for commodity receipts, which we allow producers to amortise away or leave untouched, as a commodity-reliant economy should if it wants to convince its people it is a developed economy.

On a global level, we seem to have our fates in the hands of the administrations of the US and Israel. They may have a valid point when they assert that the Iranian leadership consists of dishonest individuals.

But OPEC clearly established 50 years ago that the developed world relies very heavily on energy flowing through the Strait of Hormuz. Those running the US and Israel proceeded on a course of attacking Iran and didn’t inform the rest of the developed world that their energy lifelines were about to be imperilled.

Likewise, they seemingly didn’t give enough thought to the idea that Iran, as it has made clear countless times, would endanger energy flows out through the Straits it rests above. The people of Asia, Europe, Japan, and Australia, who are reliant on those energy flows, could plausibly assume that those on a path to war, unconcerned about the consequences of their path, have a touch of the scumbag about them, too.

The Chinese decision to immediately cease exports of aviation fuel should highlight the flaws in our decision-making leading up to this point. Is anyone going to warn them that they may perceive ‘sovereign risk’ regarding investment there?

The one upside of this for Australians may be that, from here, we can tell the gas cartel where to get off and start crafting energy policy for Australians, rather than global capital tax avoidance, especially given that China is a buyer of our gas.

And once we start thinking this, we need to start contemplating bringing meaningful productive capacity back to this country, rather than being scumbags to the future Australians and the immigrants we bring here, anticipating that their lives will be better by immersing them in unproductive debt servitude.