The ferrous jaws may have partially closed, but a new problem is fast emerging: the price of steel amid weak demand.

More profitable steel, or less loss-making steel, means more of it and lower prices, which leads to lower iron ore prices in a rinse-and-repeat cycle.

ANZ has a new report that is worth considering in this context.

It argues that Chinese steel exports will crater by 30% this year.

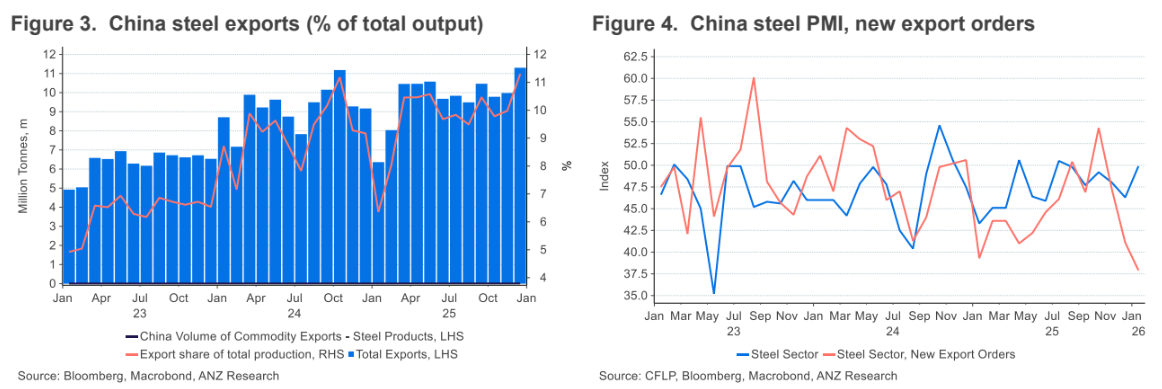

Chinese steel exports have partially offset weak domestic demand, but pressure is mounting on this avenue, the bank argues.

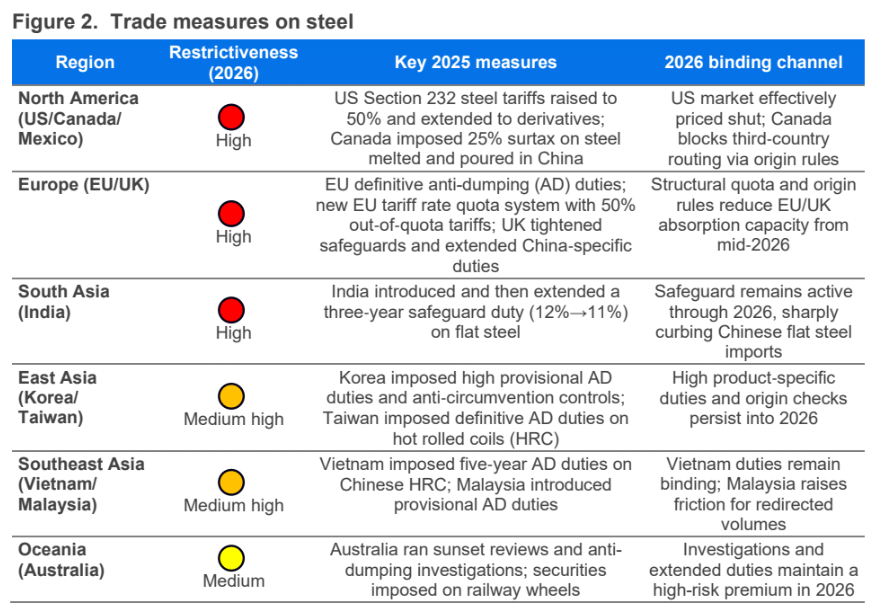

We know about the wave of tariffs slapped on Chinese steel worldwide, including in Australia, in the last few months, and we can expect more of the same in 2026.

Now, ANZ argues that the launch of Europe’s carbon border adjustment mechanism (CBAM) will jeopardise last year’s 5mt to Europe.

If China’s idled fleet of EAF mills is revived, it could easily fill any CBAM gap, so any currently pig-iron-based demand will evaporate.

Moreover, ANZ argues, part of the 2026 steel export surge was due to front-running tariffs that are now in place, so it expects that much of the 2026 demand for Chinese steel worldwide has already been satisfied.

A move away from using exports as a safety valve is also indicated by China’s introduction of export licensing for hundreds of steel products.

A 30% decline in Chinese steel exports would be equivalent to 35 million tons of steel output, nearly 4% of total output. It’s another 50mt of iron ore demand that has gone up in smoke as well.

That is more bearish than I am on steel exports, but it makes the crucial point that the steel export pressure-release valve is exhausted, so any expansion of the iron ore supply will face material demand contraction this year.

There is already evidence of weakness in exports in the Steel PMI, with new orders cratering to post-COVID lows in the new year.

ANZ reckons iron ore prices can remain above $100 in Q1 and fall to only $90 by year’s end, even in its very bearish exports scenario.

But adding the numbers results in lower prices. We already have an iron ore surplus of 70mt. New supply will be 30mt this year. Drop demand by 30mt in China, which is the marginal price setter, and you’re deep into a cost curve shakeout surplus.

That’s not $90; it’s $80 and below.

And there is one final warning to give. A group of very large, leveraged traders, such as Radiant World, has been supporting iron ore prices above $90. If the price falls below their lending thresholds, a margin call may be triggered and prices freefall.

Given the ongoing decline in the Chinese property market and the scarcity of stimmies, the outlook for steel demand in China appears bleak for 2026.

And even darker for iron ore. If ANZ’s forecast for steel exports is accurate, I anticipate that iron ore will fall below $80 in the near future.